Renovation Cost Segregation Strategy for Multifamily Investors

Jun 18, 2026Value-add multifamily investors often focus on rents, finishes, debt terms, and construction budgets. But the tax strategy can be just as important, especially when an investor buys an older property, places it in service, and then completes a major renovation. In the right facts, one cost segregation study may apply to the acquired property, while a second study may apply to capitalized renovation assets once those improvements are placed in service. The goal is not to “double dip.” The goal is to properly identify old assets, new assets, placed-in-service dates, and depreciable basis.

Let us walk you through your property. Schedule a call today.

Key Takeaways

- Understand how acquisition and renovation studies can work together

- Separate old property basis from new capital improvement costs

- Use depreciation timing to improve value-add cash flow

- Apply this strategy to older multifamily renovation projects

- Plan placed-in-service dates before the renovation begins

- See how basis allocation can change tax timing

- Use engineering support to keep the strategy defensible

What Is the Two-Study Renovation Strategy?

The two-study renovation strategy is a practical cost segregation approach for investors who buy an older residential rental property and then improve it. The first study analyzes the property as acquired. The second study analyzes the capitalized renovation costs after the renovated assets are placed in service.

For a multifamily property, the acquired building is generally 27.5-year residential rental property. But the property may also include assets that can be classified separately, such as 5-year property and 15-year land improvements. A cost segregation study uses tax and engineering analysis to identify those assets and assign cost to the correct depreciation classes.

This strategy is especially relevant for value-add investors because the acquisition and renovation are often separate economic events. The purchased property may include existing appliances, flooring, cabinets, window treatments, dedicated equipment connections, site lighting, sidewalks, paving, fencing, and other components. Later, the renovation may create new depreciable assets with their own costs and their own placed-in-service timing.

The IRS Cost Segregation Audit Technique Guide emphasizes that quality studies should classify assets into property classes, explain the rationale for § 1245 and § 1250 treatment, substantiate cost basis, and reconcile allocated costs to actual costs. That is the basic compliance logic behind this strategy. A defensible approach should feel less like a tax shortcut and more like a documented asset inventory tied to real costs.

For investors comparing this approach to a basic depreciation schedule, this is where cost segregation vs straight-line depreciation becomes more than a theory. In a renovation project, timing and asset classification can directly affect how much depreciation is available in the early years of ownership.

How the Acquisition Study and Renovation Study Work

The first cost segregation study starts with the acquired property. The purchase price is allocated between nondepreciable land and depreciable building basis. From there, the study identifies components within the depreciable basis that may qualify as 5-year property or 15-year land improvements instead of remaining entirely in 27.5-year residential rental property.

In a multifamily acquisition, 5-year property may include qualifying tangible personal property such as appliances, removable window treatments, certain specialty equipment, and eligible dedicated electrical connections that support qualifying assets. 15-year land improvements may include items such as parking areas, sidewalks, fencing, site lighting, and certain exterior improvements, depending on the facts. The remaining building structure, standard building systems, walls, roof, foundation, standard HVAC, plumbing, general electrical, and ordinary lighting generally remain 27.5-year residential rental property.

The second study focuses on capitalized renovation costs. This is not a repeat of the first study. It should analyze the new work, the invoices, contractor scopes, change orders, drawings, site observations, and placed-in-service dates for the improvements. The second study may identify new 5-year property, new 15-year land improvements, and new 27.5-year residential rental property.

This is where documentation matters. The IRS ATG says a quality study should use appropriate documentation, describe methodology, review construction records when available, and reconcile allocated costs to actual costs. That is why a value-add investor should preserve purchase documents, settlement statements, renovation invoices, contractor payment applications, photos, drawings, and unit-level scopes.

Timing is also important. A property or improvement generally has to be placed in service before depreciation begins. If the investor buys a 20-unit building and immediately rents 12 units while renovating the other 8, the placed-in-service analysis may be different than a full gut renovation where the building is not ready and available for rental use until later. This is why when to perform a cost segregation study should be part of the acquisition and renovation plan, not an afterthought.

Why This Matters for Value-Add Cash Flow

The benefit is timing. Cost segregation does not create fake costs. It changes how eligible depreciable basis is classified and recovered under the tax rules. For investors, that timing can improve after-tax cash flow during the same period when renovation budgets, lease-up risk, interest costs, and stabilization pressure are already high.

In a value-add multifamily deal, the first few years often carry the heaviest cash demands. Investors may be funding unit turns, exterior work, common area upgrades, leasing costs, and operating shortfalls. If a properly supported study moves part of the acquisition basis and part of the renovation basis into 5-year property and 15-year land improvements, the investor may be able to bring forward depreciation deductions that would otherwise be spread across 27.5-year residential rental property.

This can affect real decisions. It may influence how much capital is kept in reserve, how quickly renovation phases are completed, whether additional units are upgraded, or how the investor evaluates refinance timing. For sponsors, it can also affect investor reporting because depreciation allocations may flow through to partners based on the operating agreement and tax structure.

That said, the strategy has limits. The investor cannot simply call every renovated item 5-year property. Structural components, building systems that serve the building generally, permanent walls, roof work, windows, standard HVAC, standard plumbing, and ordinary electrical systems usually stay in 27.5-year residential rental property for residential rentals. A good study separates qualifying assets from nonqualifying assets with engineering support.

For investors who want a broader explanation of why the process matters, cost segregation benefits are strongest when the tax strategy is connected to the property’s actual business plan.

Where This Strategy Applies Best

This strategy fits older multifamily acquisitions where the investor buys an existing property and then executes a meaningful renovation plan. It may apply to small apartment buildings, garden-style multifamily communities, older townhome rental communities, mixed vintage apartment assets, and value-add syndication projects.

It can be especially useful when the property has existing 5-year property and 15-year land improvements at acquisition. Older properties often include appliances, removable items, site improvements, exterior lighting, parking areas, fencing, landscaping, signage, and other assets that should not be ignored in the original purchase allocation.

It can also be valuable when the renovation creates a second layer of capitalized assets. Examples include new appliances, qualifying removable finishes, new site improvements, clubhouse equipment, laundry room equipment, exterior amenity improvements, or dedicated systems that directly support qualifying assets. The engineering review should identify what was acquired, what was removed, what was newly installed, and what remains part of the building.

For multifamily syndications, the strategy may need additional coordination because depreciation affects partners differently. Sponsors should coordinate with their CPA, tax advisor, and cost segregation provider so the study output lines up with the partnership tax return, investor K-1 reporting, and capital account planning. This is especially important for multifamily syndication cost segregation, where one property-level decision may affect many investors.

This strategy is not limited to “gentrification” in the social sense of neighborhood change. From a tax planning standpoint, the better framing is value-add renovation. The property is purchased, improved, placed into productive rental use, and depreciated according to supported asset classifications.

How to Plan the Strategy Before You Renovate

The best time to plan this strategy is before closing or early in the renovation design phase. Waiting until tax season can still work in some cases, but the investor may lose access to details that make the study stronger. Photos disappear, walls get closed, invoices get combined, and contractors may not remember which costs relate to which assets.

Start by separating the acquisition from the renovation. The acquisition study should tie back to purchase price, land allocation, closing documents, and the condition of the property at acquisition. The renovation study should tie back to capitalized improvement costs, contractor invoices, direct and indirect costs, and the date each improvement was placed in service.

Next, track removals and replacements. If the investor removes old appliances, cabinets, flooring, site improvements, or other assets, the tax advisor may need to evaluate disposition treatment, remaining basis, and whether any partial disposition rules apply. The cost segregation study can help identify assets, but the tax return position should be coordinated with the CPA.

Then, organize renovation costs by scope. A single contractor invoice labeled “renovation work” is much harder to analyze than invoices broken down by flooring, appliances, electrical, plumbing, site work, common areas, unit interiors, and exterior improvements. The more specific the cost records, the better the engineering team can classify assets.

Finally, match the study to the tax year. If the acquired property is placed in service in one year and the renovation assets are placed in service in a later year, the studies should respect those dates. If the investor later corrects depreciation classifications for a property already placed in service, the tax advisor may need to consider whether a change in accounting method applies.

A strong renovation strategy depends on more than percentages. It depends on the same documentation discipline found in a quality cost segregation study, including methodology, cost support, asset descriptions, and reconciliation.

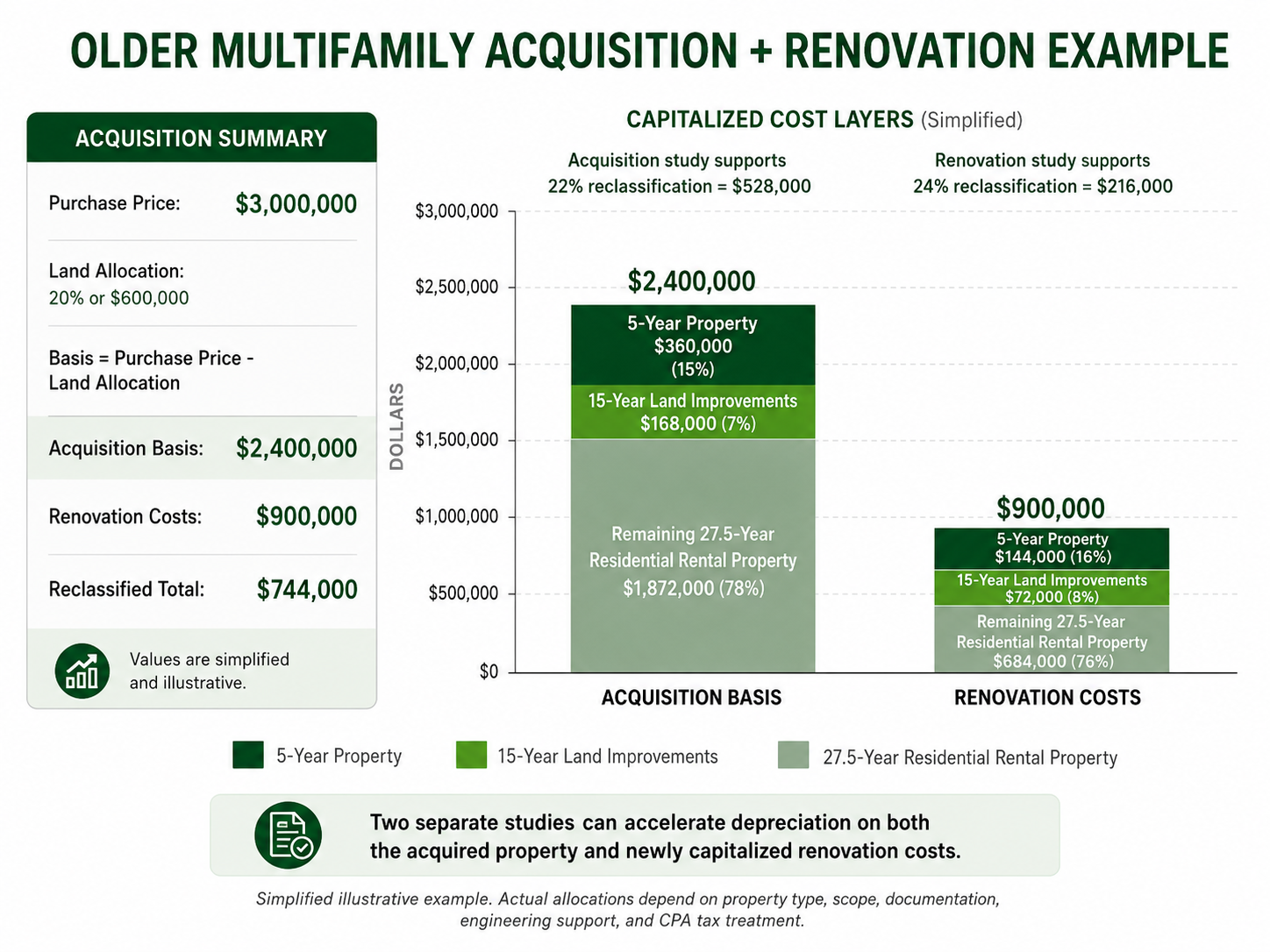

Financial Example: Older Multifamily Acquisition Plus Renovation

Assume an investor buys an older 24-unit multifamily property for $3,000,000. The land allocation is 20%, or $600,000. That leaves $2,400,000 of depreciable acquisition basis.

A cost segregation study reviews the acquired property and supports a 22% reclassification of depreciable acquisition basis into 5-year property and 15-year land improvements. That equals $528,000 reclassified from the $2,400,000 building basis. In a typical multifamily result, 5-year property is expected to be the dominant category over 15-year land improvements when the building has meaningful appliances, removable items, and qualifying personal property.

Now assume the investor completes a $900,000 capitalized renovation after acquisition. The renovation includes unit interiors, new appliances, common area updates, exterior site work, and building system upgrades. A second study reviews the renovation costs after the relevant assets are placed in service and supports a 24% reclassification, or $216,000, into 5-year property and 15-year land improvements.

The combined reclassified amount is $744,000, calculated as $528,000 from the acquisition study plus $216,000 from the renovation study. The balance remains in 27.5-year residential rental property, except for nondepreciable land. These numbers are simplified and illustrative, and the actual result depends on property type, scope, documentation, and engineering support.

The important point is that the second study is not duplicating the first study. The first study analyzes what was bought. The second study analyzes what was newly capitalized. Done correctly, this can help the investor capture depreciation timing on both the original property assets and the new renovation assets.

Investors should also consider bonus depreciation rules when eligible property is involved. Bonus depreciation depends on the tax year, property class, acquisition rules, placed-in-service timing, and elections. The study identifies assets and classes, while the CPA applies the final tax treatment on the return.

Use the Strategy, But Keep It Defensible

Yes, the broad concept can be a legal strategy when the facts support it. An investor may be able to perform a cost segregation study on the acquired property and another study on later capitalized renovations, provided each study uses the correct basis, the correct placed-in-service dates, and proper asset classification.

The key is to avoid overlap. Do not depreciate the same asset twice. Do not classify structural building components as 5-year property. Do not treat repairs, capital improvements, removals, and replacements as if they are all the same thing. And do not let the tax strategy outrun the documentation.

A value-add multifamily project is exactly the kind of situation where an engineering-based cost segregation approach can create clarity. The investor has old assets, new assets, construction records, placed-in-service events, and a business plan tied to improved cash flow. When those details are documented and aligned with established tax treatment, the strategy can be both practical and defensible.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.