Cost Segregation for Multifamily Syndications and Partners

May 26, 2026Multifamily rental properties are often purchased through syndications where multiple partners share ownership, depreciation, losses, and future upside. That makes cost segregation more than a property-level tax strategy. It becomes a partner-level planning tool that can affect K-1 reporting, cash flow projections, investor communication, and hold-period decisions. For sponsors, the key is using an engineering-based study that supports the depreciation strategy without relying on broad percentages or unsupported assumptions.

Key Takeaways

- Understand why syndications use cost segregation for multifamily rentals.

- See how engineers classify assets into depreciation categories.

- Learn why partner-level tax timing affects investor returns.

- Identify multifamily properties where studies can create value.

- Plan study timing around acquisition, reporting, and distributions.

- Review a sample multifamily syndication depreciation outcome.

- Use IRS-aligned methods to support defensible tax treatment.

Multifamily Syndication Cost Segregation Explained

Cost segregation is a tax and engineering analysis that separates a building purchase or construction cost into assets with different recovery periods. In a multifamily syndication, the property may be owned by an LLC or partnership, and depreciation typically flows through to partners based on the operating agreement and tax allocations.

The IRS Cost Segregation Audit Technique Guide explains that cost segregation studies are used to allocate building costs among land, land improvements, buildings, equipment, furniture, fixtures, and other property classes. For multifamily residential rental property, the building itself generally uses a 27.5-year recovery period. Certain tangible personal property may qualify as § 1245 property, commonly recovered over 5 years, while qualifying land improvements often fall into 15-year property.

That distinction matters because a multifamily syndication usually has many investors looking at after-tax returns, not just operating cash flow. A study that identifies appliances, removable finishes, site improvements, specialty electrical, flooring, cabinetry, and other qualifying assets may accelerate deductions in the early years of ownership.

This is also where accuracy matters. Syndicated deals often involve large acquisition prices, lender reporting, preferred returns, waterfalls, and investor tax expectations. A quality study should support the asset classifications through engineering review, documentation, and tax logic rather than relying on a blanket percentage.

How Engineers Classify Multifamily Assets in a Syndicated Deal

The process starts with the property basis, land allocation, placed-in-service date, construction records, purchase documents, settlement statements, appraisals, site information, and available drawings. From there, an engineering-based cost segregation study identifies property units and assigns costs to the correct depreciation categories.

For multifamily residential rental property, common categories include 27.5-year residential rental building components, 5-year tangible personal property, and 15-year land improvements. The IRS ATG residential rental property matrix identifies many asset types that can appear in apartment communities, including awnings, removable items, site components, and other property elements.

The technical line between short-life and long-life property is not based on whether an item feels useful to tenants. It is based on tax classification, permanence, function, attachment, and whether the asset is part of the building structure or a separate item of tangible personal property. This is why a quality cost segregation study is especially important for syndicated multifamily deals.

A syndication also has to think beyond the report itself. Once the study is complete, the CPA must apply the results to the partnership return, depreciation schedules, partner K-1s, and any special allocations required by the partnership agreement. The engineering study identifies the property-level depreciation opportunity, but the partnership tax reporting determines how that benefit reaches the investors.

Why Partner-Level Depreciation Timing Matters

Multifamily syndications often attract investors because of a mix of cash flow, appreciation, principal paydown, and potential tax benefits. Cost segregation can improve the timing of depreciation deductions, which may reduce taxable income allocated to partners in the early years of the deal.

That timing can be meaningful. A partner receiving quarterly distributions may still care deeply about what appears on the annual K-1. If accelerated depreciation helps reduce taxable income from the property, the investor may see a stronger after-tax result than the cash yield alone suggests.

This is why sponsors often discuss cost segregation benefits during acquisition planning. The strategy can help investors understand how depreciation interacts with projected returns, especially when the property has a strong basis allocation to depreciable improvements.

The benefit is not identical for every partner. Passive activity rules, at-risk rules, real estate professional status, outside basis, suspended losses, and each investor’s personal tax situation can affect whether depreciation losses are currently usable. A sponsor should avoid promising identical tax outcomes to every investor. The better approach is to provide a defensible study, clear reporting, and room for each investor’s tax advisor to evaluate the impact.

Cost Segregation Applications for Multifamily Syndications

Multifamily syndications can use cost segregation across several property types and deal structures. Garden-style apartments, mid-rise apartments, student housing, build-to-rent communities, senior housing that qualifies as residential rental property, and mixed-use properties with a residential component may all benefit from a study.

Acquisition deals are common candidates because the purchase price must be allocated between land and depreciable property. The study can then identify shorter-life assets within the depreciable basis. Value-add deals can also be strong candidates because renovations may create additional asset classification opportunities when costs are properly tracked.

New construction syndications can benefit as well, especially when detailed construction records are available. In those cases, invoices, contractor schedules, plans, change orders, and cost records can often support a more direct engineering analysis than an acquired property with limited historical cost detail.

Mixed-use properties require extra care. If the asset includes apartment units, retail space, restaurants, leasing offices, clubhouses, parking structures, or amenities, the property may include more than one tax classification framework. For example, a clubhouse may be treated differently from residential rental apartment buildings, and commercial areas may need separate analysis. This is where timing a cost segregation study early can help the sponsor coordinate the engineering review with tax reporting before investor K-1s are prepared.

Planning Cost Segregation Before K-1s and Investor Updates

The best time to plan a cost segregation study is before the partnership return is finalized. For a syndication, that usually means starting soon after acquisition, renovation completion, or placed-in-service timing is clear.

Waiting too long can create avoidable friction. The CPA may need depreciation schedules before filing the partnership return. Investors may be waiting on K-1s. The sponsor may be preparing annual updates or refinance projections. If the study starts late, the team can lose the opportunity to make clean first-year reporting decisions.

Sponsors should also coordinate the study with the operating agreement. The agreement may contain provisions about depreciation allocations, tax distributions, special allocations, capital accounts, and waterfall economics. Cost segregation does not rewrite the deal economics, but it can change the timing and amount of tax depreciation reported by the partnership.

Bonus depreciation planning adds another layer. When eligible short-life assets are identified, bonus depreciation and cost segregation may accelerate deductions further, depending on the placed-in-service year, asset eligibility, and elections made by the taxpayer. In a syndication, those elections can affect all partners, so they should be reviewed before filing rather than treated as an afterthought.

A practical sponsor checklist includes the settlement statement, purchase agreement, appraisal if available, closing date, placed-in-service date, property photos, rent roll, unit mix, site plan, renovation budget, capital improvement details, and construction documents. Better inputs usually lead to better classification support.

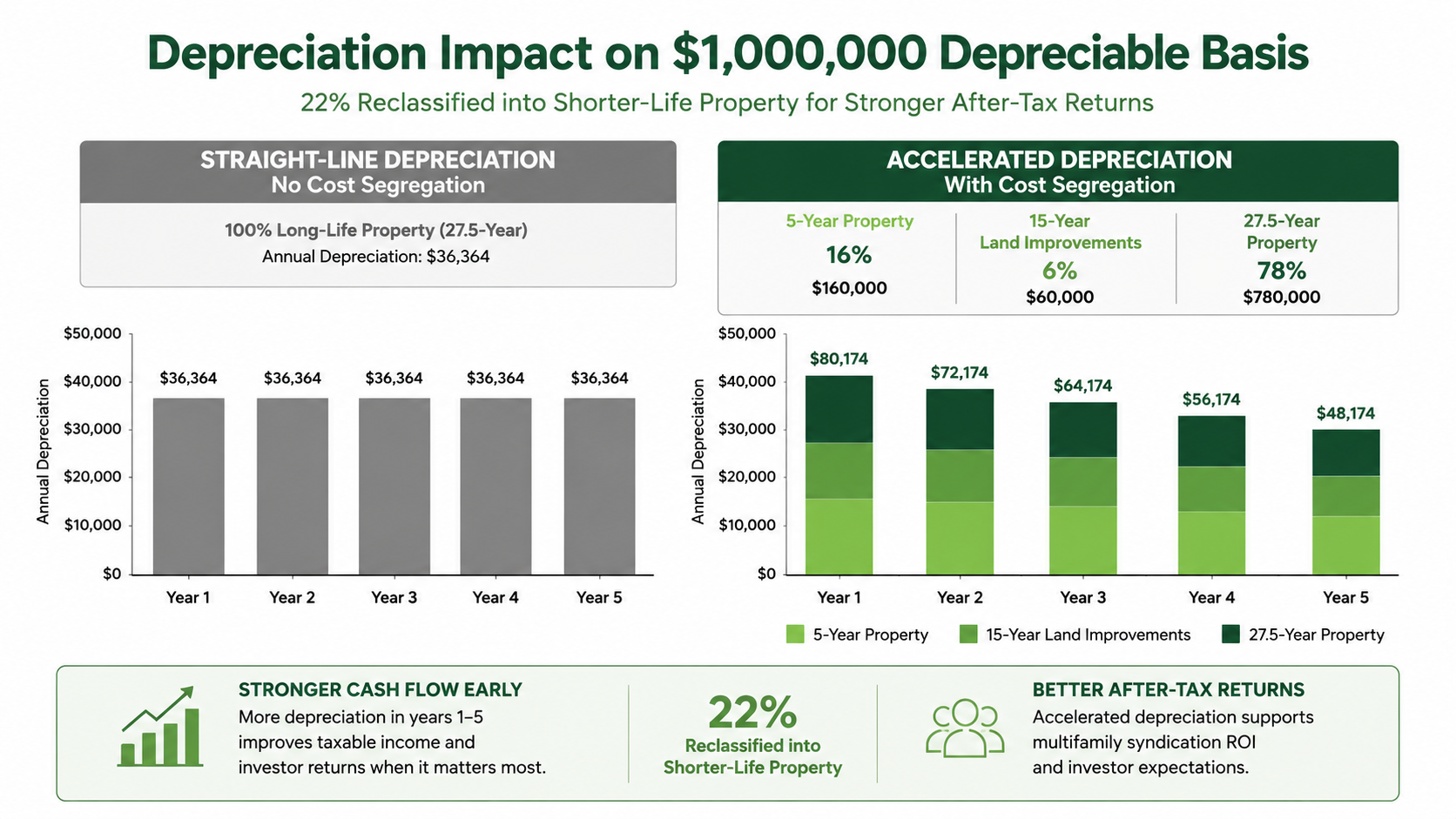

Financial Example: Multifamily Syndication Depreciation Impact

Assume a multifamily syndication acquires a 96-unit apartment property for $6,000,000. After allocating $1,200,000 to land, the depreciable building and improvement basis is $4,800,000.

Without cost segregation, most of that depreciable basis may be recovered over 27.5 years as residential rental property. That produces roughly $174,545 of annual straight-line depreciation before considering other adjustments.

Now assume an engineering-based cost segregation study identifies 22% of the depreciable basis as shorter-life property. That equals $1,056,000 reclassified from the 27.5-year building bucket into accelerated categories. In many multifamily studies, 5-year property is often the dominant short-life category, with 15-year land improvements also contributing depending on the site, amenities, and facts.

If $750,000 is classified as 5-year property and $306,000 is classified as 15-year property, the early-year deductions can increase materially compared with straight-line treatment. If eligible bonus depreciation applies to some or all of the short-life assets, the first-year impact may be even larger.

For the partners, the property-level deduction flows through the partnership reporting structure. A $1,056,000 reclassification does not mean every investor gets the same tax result. It means the partnership has a larger pool of accelerated depreciation to allocate according to the tax rules and operating agreement.

This can help a sponsor present a more complete after-tax investment picture. The internal rate of return, cash-on-cash return, and equity multiple are important, but tax timing can also shape investor outcomes. A responsible model should show that depreciation benefits depend on each investor’s tax profile and should not be treated as a guaranteed cash refund.

Using IRS-Aligned Methods for Syndicated Multifamily Deals

Cost segregation can be a strong strategy for multifamily syndications, but it should be handled with discipline. The IRS ATG emphasizes asset classification, documentation, methodology, and support. That is especially important when a deal has multiple partners relying on the same study.

A sponsor should want more than a high reclassification percentage. The better goal is a defensible result that aligns with the property facts, tax rules, engineering observations, and partnership reporting timeline. Overstating short-life assets may look attractive in a projection, but it can create problems if the classification is not supportable.

For multifamily syndications, the strongest studies connect the tax strategy to the physical property. They evaluate the building, site improvements, unit interiors, amenities, electrical systems, finishes, and supporting documentation. They also give the CPA a clearer basis for depreciation schedules and K-1 reporting.

When done well, cost segregation gives sponsors and partners a practical way to improve depreciation timing, increase early tax efficiency, and support investor-level planning through established tax treatment.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.