How Cost Segregation Helps Real Estate Investors Reduce Taxes and Increase Cash Flow

Feb 05, 2026Brian explains how real estate investors can reduce taxes and increase cash flow

Cost segregation is one of the most effective tax strategies available to real estate investors. It allows property owners to accelerate depreciation by reclassifying building components into shorter recovery periods. This creates larger upfront deductions without changing the economics of the property itself. The result is reduced taxable income and improved liquidity. For investors focused on scaling portfolios, this strategy directly impacts cash flow and reinvestment potential.

Key Takeaways

- Cost segregation reclassifies building assets into shorter depreciation lives

- Engineering-based studies identify 5, 7, and 15-year property

- Accelerated depreciation reduces taxable income early

- Applicable across commercial, residential, and renovation projects

- Timing and execution determine overall tax efficiency

- Bonus depreciation amplifies front-loaded deductions

- Improved cash flow supports reinvestment and growth

- Works for both new acquisitions and existing properties

What Is Cost Segregation

Cost segregation is a tax strategy that separates a property into individual components for depreciation purposes. Instead of depreciating the entire building over 27.5 or 39 years, specific assets such as flooring, electrical systems, and land improvements are classified into shorter recovery periods.

These shorter-life assets often fall into categories like 5-year property and 15-year property. This reclassification is supported by engineering analysis and tax law interpretation. According to IRS guidance, buildings contain multiple asset types with different recovery periods, which makes cost allocation both necessary and beneficial.

How It Works

A cost segregation study analyzes construction documents, site conditions, and asset usage to properly classify components. The goal is to identify which portions of the property qualify as shorter-life assets under tax law.

Engineering-based approaches are considered the most reliable because they rely on detailed cost records and documentation. These studies often include asset identification and classification, cost allocation using construction data, and application of depreciation schedules.

Once complete, the investor can apply accelerated depreciation methods. When paired with bonus depreciation and cost segregation, a significant portion of the property can be written off in the early years of ownership.

Why It Matters

The primary advantage of cost segregation is timing. Instead of spreading deductions evenly over decades, investors can front-load depreciation into the first few years.

This creates immediate tax savings by reducing taxable income. Lower tax liability translates into higher after-tax cash flow. That additional liquidity can be used to acquire new properties, fund renovations, or reduce debt.

Understanding the difference between cost segregation vs straight-line depreciation highlights how significant this timing shift can be. Accelerated strategies allow investors to control when deductions occur, which is critical for portfolio growth.

Applications Across Property Types

Cost segregation is not limited to a single asset class. It applies across a wide range of real estate investments, including multifamily properties, office buildings, retail centers, and industrial facilities.

It is also highly effective for renovation projects. Strategies involving Qualified Improvement Property allow interior improvements to qualify for accelerated depreciation.

Additionally, cost segregation can be performed retroactively. Investors who did not apply the strategy at acquisition can still benefit through a catch-up adjustment, often without amending prior returns.

Strategic Timing and Execution

Executing a cost segregation strategy requires proper timing and planning. The greatest benefits occur when the study is completed early in the ownership cycle. However, retroactive studies remain a viable option.

Investors should also evaluate when to deploy the strategy based on income levels and tax planning goals. Understanding when to perform a cost segregation study ensures deductions align with broader financial objectives.

Equally important is study quality. Poor methodology or aggressive assumptions can create audit risk. The IRS emphasizes that classifications must be supported by documentation and engineering analysis.

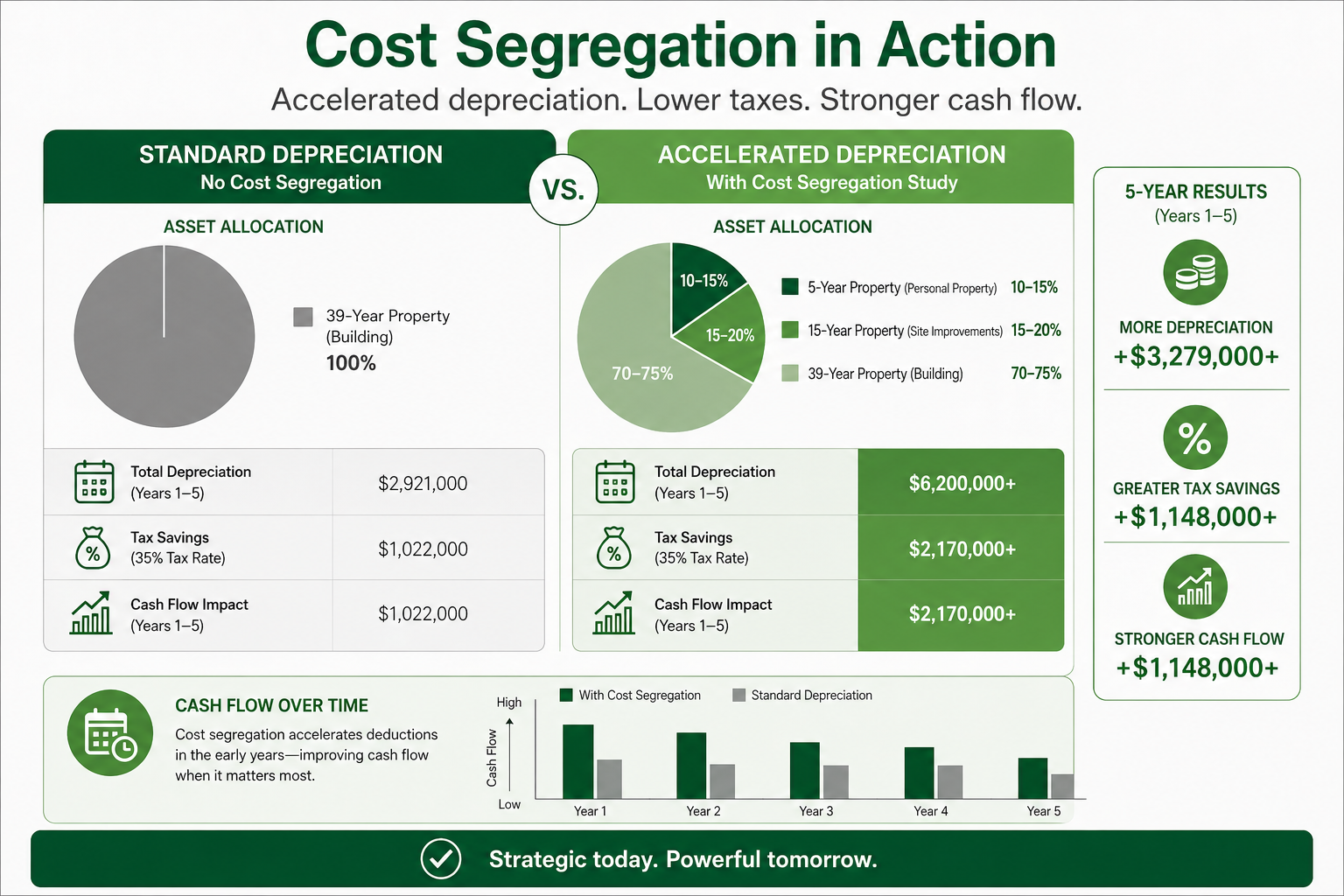

Scenario Analysis: Accelerated Depreciation Impact on Cash Flow

Consider a $2 million commercial property. Under standard depreciation, the annual deduction might be approximately $51,000. With cost segregation, 25 percent of the property may be reclassified into shorter-life assets.

This could generate several hundred thousand dollars in additional first-year depreciation. If combined with bonus depreciation, the investor may significantly reduce taxable income in year one.

The result is immediate tax savings that can be reinvested into new opportunities.

Building Long-Term Wealth Through Tax Efficiency

Cost segregation is not just a tax tactic. It is a capital allocation strategy. By accelerating depreciation, investors gain access to capital earlier in the investment lifecycle.

This creates a compounding effect. More cash flow leads to more acquisitions, which leads to more depreciation opportunities. Over time, this cycle enhances both portfolio scale and overall returns.

Investors who integrate cost segregation into their strategy position themselves to operate more efficiently and grow faster in competitive markets.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.