Cost Segregation vs Straight-Line Depreciation Strategy

May 01, 2026Depreciation is one of the most powerful tax tools available to real estate investors. Yet, the method used to calculate depreciation can dramatically change both short-term cash flow and long-term tax outcomes. Straight-line depreciation remains the default approach, but cost segregation introduces a more strategic alternative by accelerating deductions. Understanding the difference between these two methods is essential for investors focused on optimizing returns. The choice is not just accounting mechanics, it is a capital strategy.

Key Takeaways

- Straight-line depreciation spreads deductions evenly over time

- Cost segregation reclassifies assets into shorter recovery periods

- MACRS allows accelerated depreciation through asset classification

- Engineering-based studies drive cost segregation accuracy

- Acceleration increases early-year tax savings and liquidity

- Timing differences impact long-term tax positioning

- Different property types yield different acceleration benefits

- Bonus depreciation amplifies cost segregation outcomes

- Strategic timing determines overall ROI effectiveness

What Is Straight-Line vs Cost Segregation

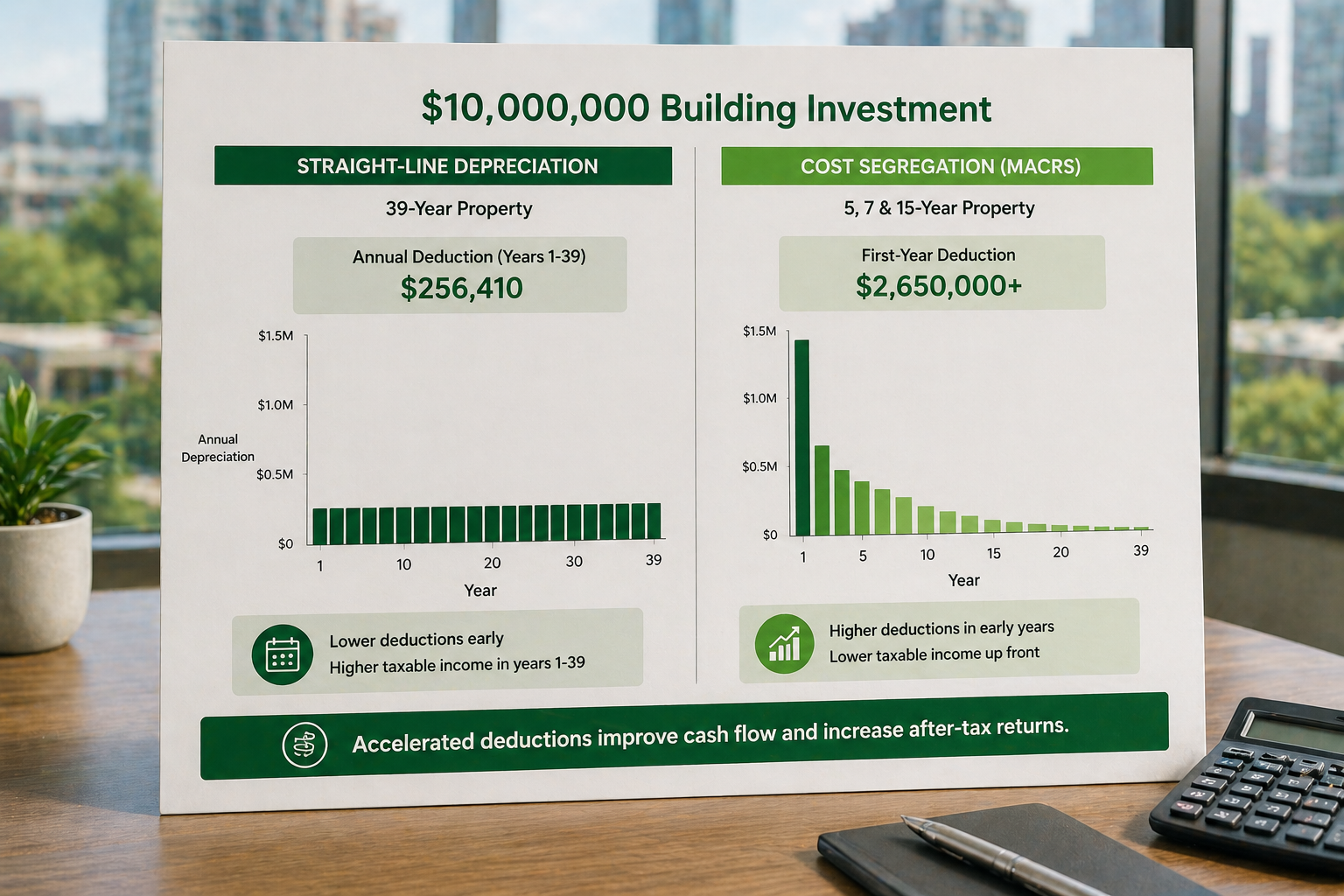

Straight-line depreciation allocates the cost of a property evenly across its IRS-defined recovery period. For residential rental property, this is typically 27.5 years, while commercial property is depreciated over 39 years. This method is simple, predictable, and widely used as the default approach.

Cost segregation, by contrast, is a detailed analysis that separates a property into individual components with shorter depreciable lives. Assets such as flooring, lighting, cabinetry, and certain electrical systems may qualify for 5, 7, or 15-year treatment instead of remaining in the 27.5 or 39-year category. This reclassification aligns with IRS guidance that different components of a property have different useful lives.

The result is not a change in total depreciation, but a shift in timing.

How the Strategy Works

Straight-line depreciation applies a uniform annual deduction. For example, a $1,000,000 residential building produces approximately $36,364 in annual depreciation.

Cost segregation uses an engineering-based approach to identify and allocate costs to shorter-life assets. IRS audit guidance identifies detailed engineering methods using actual cost records or estimates as among the most accurate approaches. These studies analyze construction documents, site conditions, and asset usage to determine proper classifications.

Investors often pair this strategy with bonus depreciation and cost segregation, allowing a significant portion of those short-life assets to be deducted in the first year.

For a deeper look at classification mechanics, see 5-year property and how assets qualify.

Why the Difference Matters for Investors

The core advantage of cost segregation is timing. Accelerating depreciation increases early-year deductions, which reduces taxable income and improves immediate cash flow.

Straight-line depreciation delays these benefits by spreading them evenly. While the total deduction remains the same over time, the present value of money makes earlier deductions significantly more valuable.

However, acceleration introduces planning considerations. Investors must evaluate future recapture, income projections, and exit strategy. Misclassification or aggressive assumptions can also create audit exposure, particularly if short-life assets are overstated. Understanding the risks of overestimating short-life assets is critical for maintaining compliance.

Where Each Strategy Applies

Straight-line depreciation is most appropriate for investors seeking simplicity or holding properties with minimal component variation. It requires no engineering study and involves minimal upfront cost.

Cost segregation is most effective for newly constructed properties, recently acquired commercial real estate, properties undergoing renovation, and assets with significant personal property components.

For example, investors pursuing Qualified Improvement Property strategies can combine cost segregation with accelerated depreciation on interior improvements.

Additionally, understanding when to perform a cost segregation study can materially impact results, especially when aligning with acquisition or renovation timelines.

Choosing the Right Depreciation Strategy

The decision between straight-line and cost segregation should be based on investor objectives, tax position, and portfolio strategy.

Key considerations include current taxable income versus future income expectations, holding period of the asset, eligibility for bonus depreciation, complexity tolerance and compliance requirements, and cost of performing a study relative to expected savings.

Investors focused on maximizing near-term cash flow often favor cost segregation. Those prioritizing simplicity or long-term stability may prefer straight-line treatment.

Accelerated Depreciation Impact Example

Consider a $2,000,000 commercial property.

Under straight-line depreciation, the annual deduction is approximately $51,282.

With cost segregation, assume 25 percent of the property is reclassified into shorter-life assets. If bonus depreciation is applied, a significant portion of that $500,000 may be deducted in year one.

This creates a substantial upfront tax benefit, improving liquidity and enabling reinvestment. The difference is not theoretical, it directly affects available capital.

Strategic Positioning for Long-Term Returns

Depreciation strategy is not just a tax decision, it is a capital allocation decision. Cost segregation shifts deductions forward, enhancing early cash flow and increasing investment velocity. Straight-line depreciation preserves simplicity and predictability.

The optimal approach depends on how an investor values timing, risk, and reinvestment opportunity. When used correctly, cost segregation becomes a lever for scaling portfolios, not just reducing taxes.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.