What Defines a Quality Cost Segregation Study for Investors

Apr 24, 2026Cost segregation can significantly accelerate depreciation, but not all studies deliver the same financial outcome or level of protection. For investors, the difference between a high-quality study and a low-quality one is not just technical, it directly impacts cash flow, audit risk, and long-term tax strategy. A poorly executed study may overstate short-life assets or lack proper documentation, increasing exposure under IRS review.

A quality cost segregation study is defined by its methodology, documentation, and defensibility. These elements determine whether the study withstands scrutiny and produces sustainable tax benefits. Investors who understand these standards are better positioned to evaluate providers and avoid costly mistakes.

Key Takeaways

- Strong engineering-based methodologies improve accuracy and defensibility

- Detailed records support asset classification and cost allocations

- Proper classification relies on established tax law and precedent

- Physical inspection and technical review increase reliability

- Total costs must reconcile to actual project or acquisition values

- Quality studies reduce audit exposure and reclassification risk

- Accurate separation of §1245 and §1250 property is critical

- Proper allocation of indirect costs impacts total depreciation

- Higher quality studies produce more predictable tax outcomes

Why Methodology Determines Financial Outcomes

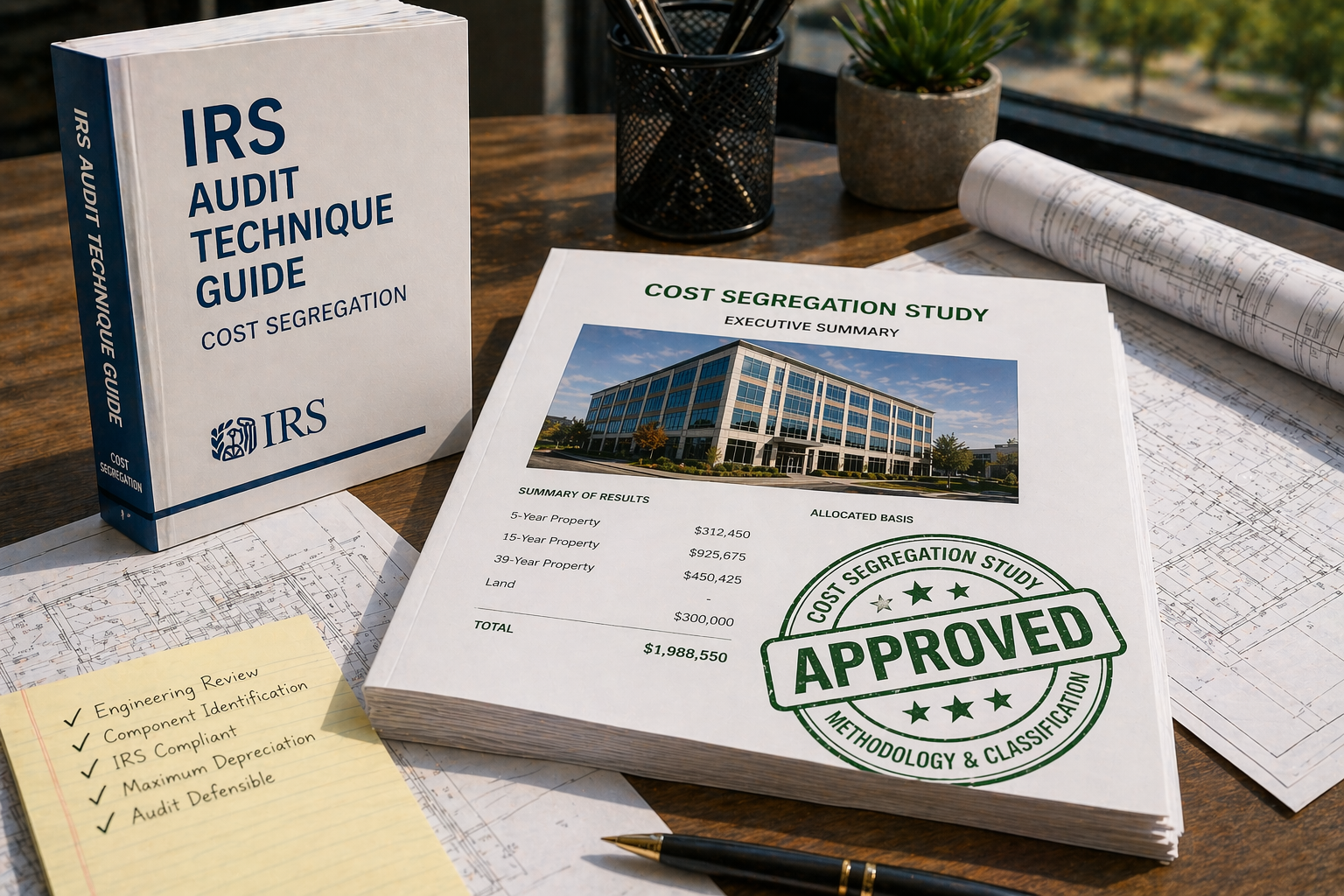

A quality study begins with a defensible methodology. The most reliable approach uses detailed engineering analysis based on actual cost records or well-supported cost estimates. This method identifies individual building components and assigns them to appropriate asset classes.

The IRS Cost Segregation Audit Technique Guide emphasizes that cost segregation is fundamentally an allocation process requiring accurate identification of asset types and recovery periods.

Lower-quality studies often rely on shortcuts such as rule-of-thumb percentages or residual estimation. These approaches may inflate short-life assets, creating short-term tax benefits but increasing long-term risk. Investors should prioritize studies that clearly explain how costs were derived and allocated.

How Engineering Analysis Strengthens Accuracy

A defining feature of a quality study is the use of engineering-based analysis. This includes site inspections, review of construction documents, and detailed cost breakdowns.

Engineering analysis allows for:

- Identification of specific components within a property

- Accurate classification of assets based on use and function

- Supportable cost allocation tied to real-world construction data

The IRS highlights that detailed engineering approaches using actual cost records are generally the most accurate method available. This level of precision reduces the likelihood of misclassification, particularly in complex systems such as electrical or plumbing infrastructure.

In contrast, studies that lack physical inspection or rely solely on estimates often miss critical details that affect classification and depreciation.

Why Legal Classification Drives Compliance

Cost segregation is not just an engineering exercise. It is a legal classification process governed by tax law. A quality study must clearly justify why assets are classified as shorter-life property.

The distinction between §1245 and §1250 property is central. Tangible personal property qualifies for accelerated depreciation, while structural components of a building do not. This classification depends on facts and circumstances rather than fixed rules.

A strong study includes:

- Legal analysis supporting each classification

- References to relevant case law and IRS guidance

- Clear explanation of how assets meet classification criteria

Without this legal framework, even technically accurate allocations may fail under audit review.

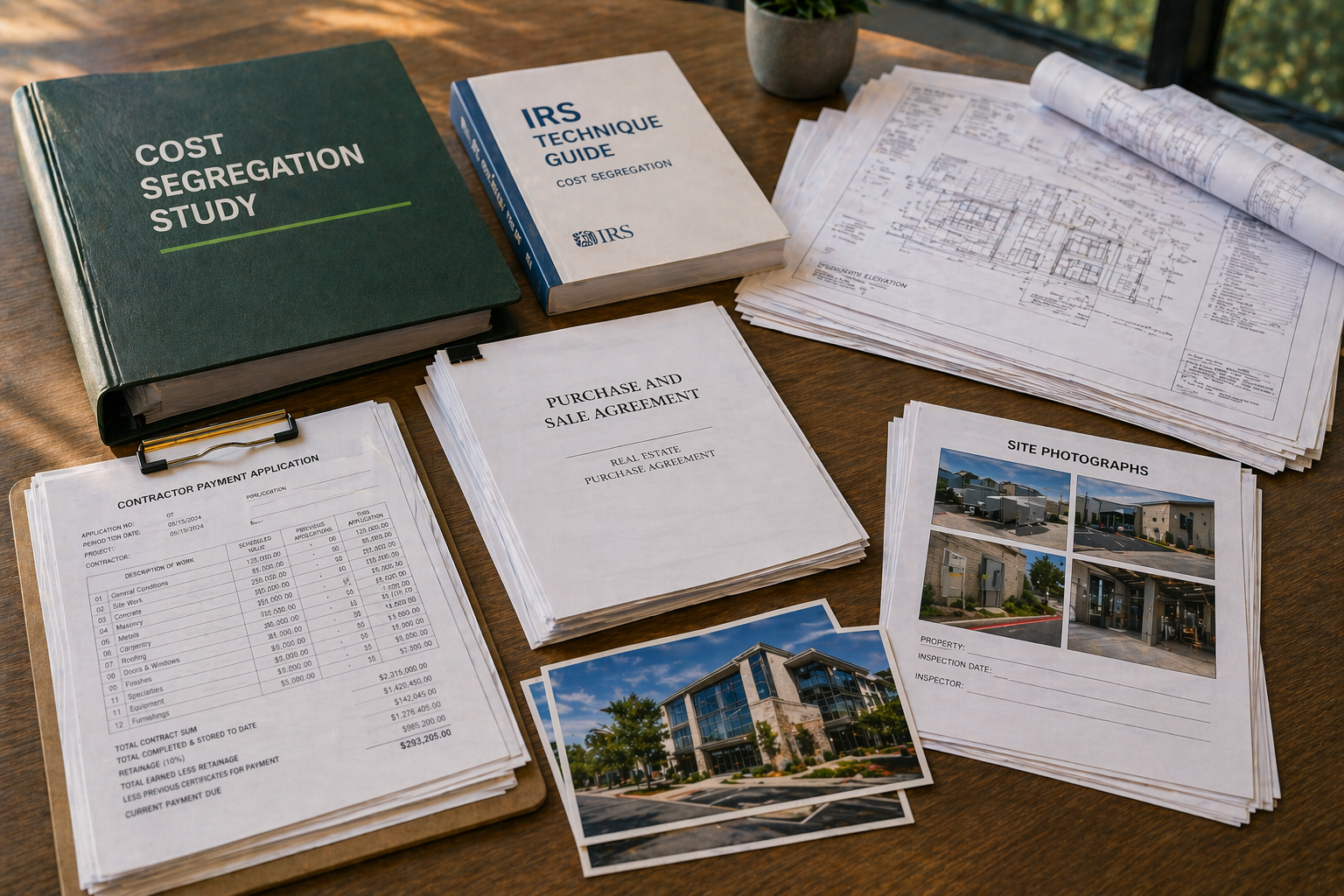

Where Documentation Becomes a Risk Factor

Documentation is often the dividing line between a defensible study and one that creates exposure. A quality cost segregation study uses the best available records to support every allocation.

This includes:

- Construction drawings and specifications

- Contractor payment applications and invoices

- Purchase agreements for acquired properties

- Site photographs and inspection records

The IRS specifically notes that cost segregation studies vary widely in documentation quality, and this inconsistency contributes to audit challenges. Studies lacking documentation force auditors to question assumptions, increasing the likelihood of adjustments.

Investors should view documentation not as a formality but as a critical component of risk management.

How Cost Reconciliation Protects Investors

A quality study must reconcile total allocated costs to actual project or acquisition costs. This ensures that no value is artificially created or misallocated across asset classes.

Failure to reconcile costs is a common issue in lower-quality studies. For example, applying arbitrary adjustments to match purchase price without supporting analysis can indicate inaccurate estimates.

The IRS emphasizes that total allocated costs should align with actual costs or properly estimated values. When this reconciliation is missing, the reliability of the entire study is compromised.

For investors, this directly affects the credibility of depreciation deductions and increases the risk of reclassification.

How Indirect Cost Allocation Impacts Results

Indirect costs, such as engineering fees, permits, and overhead, must be properly allocated across asset classes. A quality study clearly explains how these costs are treated.

Some indirect costs apply broadly across the project, while others relate to specific assets. Misallocating these costs can distort depreciation outcomes and lead to inaccurate tax positions.

Proper allocation requires:

- Identification of all indirect costs

- Logical assignment based on asset relationships

- Consistent methodology across the study

This level of detail ensures that depreciation calculations reflect the true economic structure of the property.

Investor Scenario: Comparing Study Quality Outcomes

Consider two investors acquiring similar commercial properties. Both commission cost segregation studies, but the methodologies differ.

The first study uses a detailed engineering approach with full documentation, site inspection, and cost reconciliation. The second relies on industry averages and limited supporting data.

The first investor receives:

- Accurate asset classification

- Defensible depreciation schedules

- Lower audit exposure

The second investor may initially see higher deductions, but faces:

- Increased risk of IRS adjustment

- Potential recapture or penalties

- Uncertain long-term tax outcomes

This contrast highlights that study quality is not just about maximizing deductions, but about sustaining them.

Strategic Considerations for Investors

Investors should evaluate cost segregation providers based on their ability to deliver a quality study, not just projected tax savings.

Key considerations include:

- Whether the study uses engineering-based methodology

- The depth and quality of supporting documentation

- The presence of legal analysis supporting classifications

- The ability to reconcile costs accurately

- The experience and qualifications of the preparer

A quality study aligns tax strategy with compliance, ensuring that accelerated depreciation benefits are both achievable and sustainable.

Protecting Long-Term Tax Efficiency

A quality cost segregation study is ultimately a risk-adjusted investment decision. While accelerated depreciation improves short-term cash flow, its long-term value depends on the study’s accuracy and defensibility.

Investors who prioritize quality gain more than tax savings. They gain predictability, reduced audit exposure, and confidence in their financial reporting. In a market where tax strategy plays a central role in returns, the integrity of a cost segregation study becomes a critical component of overall investment performance.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.