Cost Segregation for Mobile Home Parks: Utility, Pads, Homes

Jun 23, 2026Mobile home parks are among the most misunderstood asset classes when it comes to cost segregation. Many investors assume most of the purchase price is tied to land and therefore offers limited depreciation opportunities. In reality, mobile home parks often contain substantial amounts of depreciable infrastructure that may qualify for accelerated depreciation when properly identified and documented.

The key question is not simply whether a park contains homes. Investors must determine who owns the homes, how utilities are delivered, what site improvements exist, and how those assets function within the overall property. These distinctions can materially impact the amount of basis allocated to 5-year property, 15-year land improvements, and longer-lived real property.

A properly executed engineering-based study evaluates each component separately rather than treating the entire property as a single asset category. This approach aligns with IRS guidance emphasizing asset identification, classification, and documentation within a quality cost segregation study.

Schedule a CostSegRx Strategy Call.

Key Takeaways

- Understand why mobile home parks differ from other real estate assets

- Learn how utility systems and pads are classified

- See why ownership structure affects depreciation opportunities

- Review common mobile home park investment scenarios

- Explore planning opportunities before acquisition and renovations

- Analyze a realistic mobile home park cost segregation example

- Understand how engineering methodology supports defensible classifications

What Makes Mobile Home Park Cost Segregation Unique?

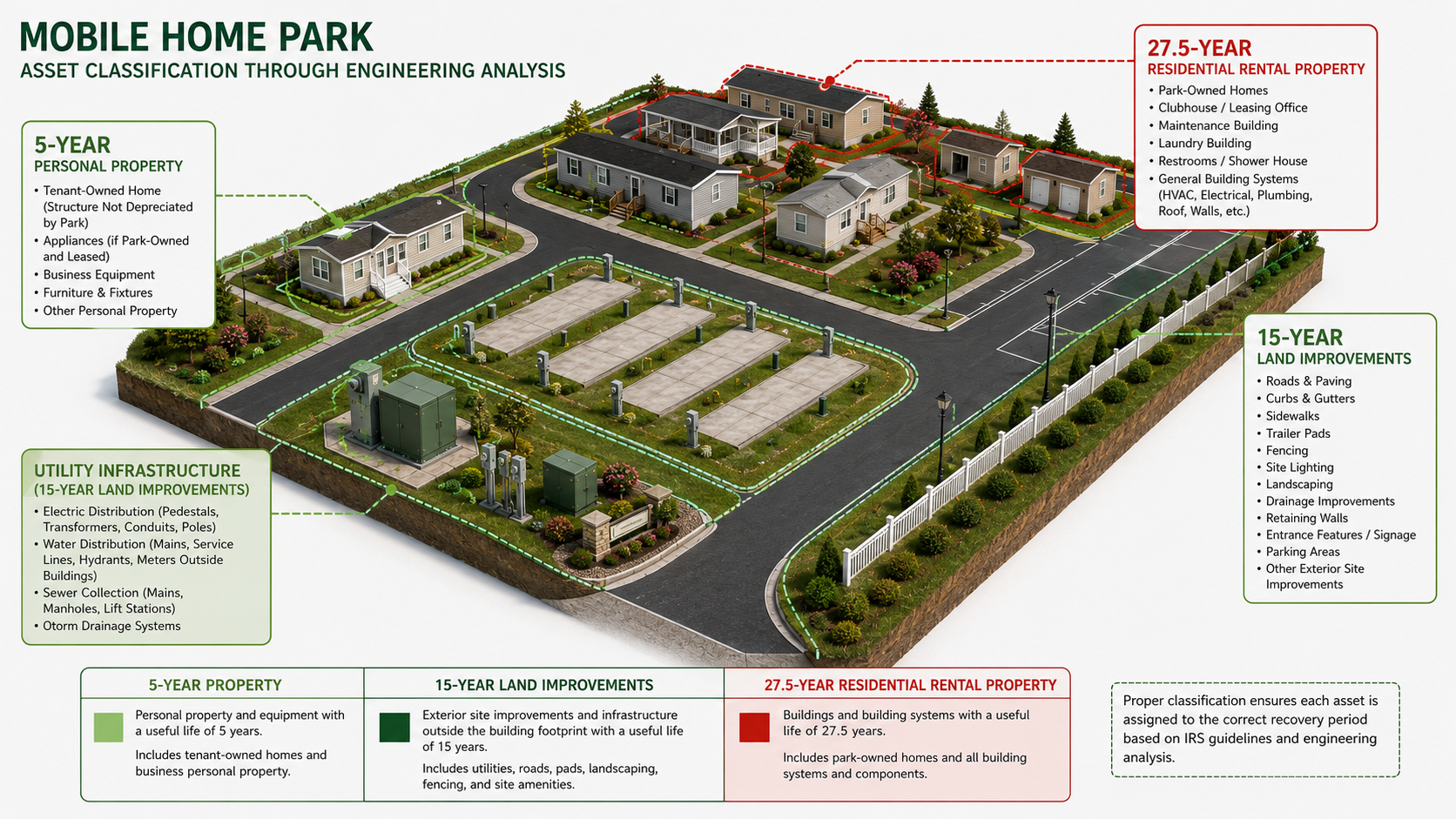

Unlike apartments or traditional residential rentals, mobile home parks frequently contain a large concentration of infrastructure assets outside the homes themselves. Many of these assets may qualify as depreciable land improvements or tangible personal property when properly analyzed.

Typical mobile home park assets include concrete trailer pads, utility hookups, water distribution systems, sewer systems, electrical pedestals, gas distribution systems, site lighting, roads, parking areas, sidewalks, fencing, landscaping, clubhouses, laundry facilities, and maintenance buildings.

The IRS Cost Segregation Audit Technique Guide recognizes that land improvements are separate from buildings and structural components and often carry different recovery periods. Assets such as roads, sidewalks, drainage systems, landscaping, and fencing commonly fall within the land improvement category.

Many investors overlook the substantial value associated with these improvements. In some mobile home parks, infrastructure and site improvements may represent a larger accelerated depreciation opportunity than the homes themselves.

For a deeper discussion of qualifying land improvement assets, see cost segregation for land improvement heavy businesses.

How Utility Infrastructure, Pads, and Homes Are Classified

Mobile home parks require a detailed asset-by-asset review because ownership and functionality drive classification.

Utility systems often include water mains, sewer mains, electrical distribution systems, electrical pedestals, gas distribution systems, and telecommunications infrastructure.

Some portions of these systems may qualify as 15-year land improvements while others require more detailed engineering analysis. The IRS ATG specifically discusses functional allocation issues involving electrical distribution systems and the importance of identifying assets that directly support qualifying property.

Investors interested in electrical classification issues should review electrical distribution systems in cost segregation studies.

Concrete and gravel pads are often among the most valuable land improvement assets within a mobile home park. Depending on construction and use, trailer pads commonly fall within the 15-year land improvement category rather than being treated as part of the underlying land.

Many mobile home parks operate under a ground-rent model where tenants own their homes and rent the lot. When residents own the homes, the investor generally does not depreciate the homes. The investor's basis is concentrated in land improvements, utility systems, common areas, roads, site infrastructure, and amenities.

Other parks own some or all manufactured homes. When the park owns the homes, each home must be evaluated separately. Depending on facts and circumstances, these assets may be classified differently than traditional site-built residential structures.

A quality engineering study evaluates home construction type, foundation system, utility connections, permanency characteristics, ownership structure, and placement method. The IRS ATG discusses the importance of determining whether assets are inherently permanent and evaluating facts and circumstances when classifying property.

Why Ownership Structure Changes the Tax Outcome

Two mobile home parks with identical purchase prices can produce dramatically different depreciation results.

A tenant-owned home community with extensive infrastructure, large utility systems, and numerous trailer pads may generate significantly more accelerated depreciation through infrastructure and land improvement allocations than a park-owned home community with minimal infrastructure improvements and limited common-area assets.

This is one reason experienced investors frequently compare depreciation opportunities during acquisition underwriting. A study that properly identifies 15-year property and 5-year property can materially improve after-tax cash flow.

Common Mobile Home Park Scenarios

Tenant-owned home communities are often strong candidates for cost segregation because the investor primarily owns utility infrastructure, roads, pads, common areas, and amenities. These properties often have substantial land improvement value.

Hybrid communities require separate treatment of infrastructure and housing assets because the investor owns some homes while residents own others.

Park-owned home communities require more detailed classification analysis because each housing asset may affect overall depreciation treatment.

Redevelopment and expansion projects may also create significant new depreciable basis when investors add new sites, roads, utility systems, or amenity areas.

For investors planning major upgrades, design-build cost segregation planning can help identify opportunities before construction begins.

Strategic Planning Opportunities for Mobile Home Park Owners

The most effective mobile home park studies begin before tax filing season.

Important planning considerations include acquisition due diligence, utility mapping, infrastructure documentation, site plans, historical construction records, capital improvement tracking, and expansion planning.

The IRS Cost Segregation ATG identifies documentation, engineering analysis, asset schedules, and reconciliation procedures as critical components of a quality study.

Investors should also understand what defines a quality cost segregation study before selecting a provider.

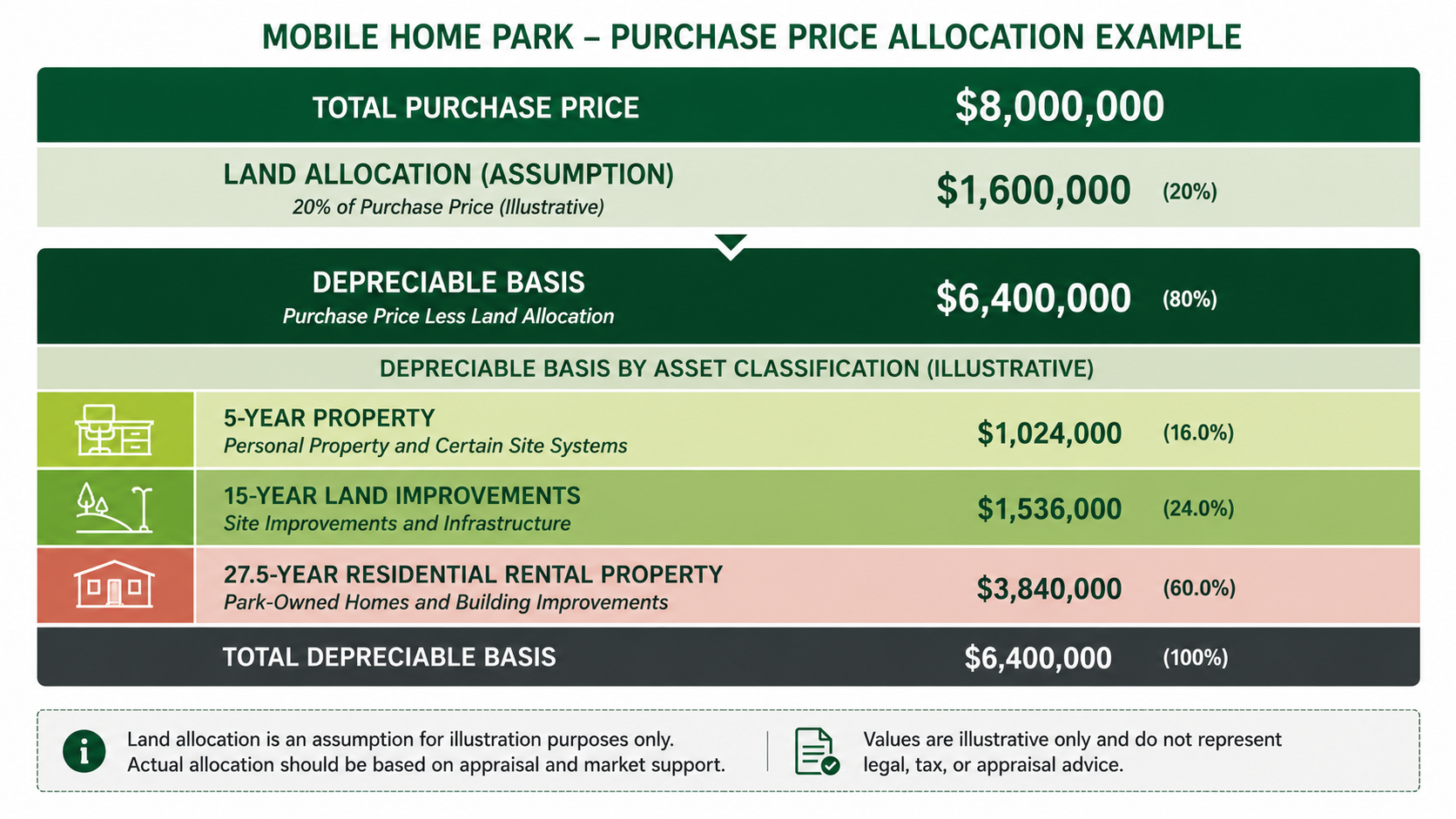

Mobile Home Park Financial Example

Assume an investor purchases a mobile home park for $8,000,000.

Purchase Price: $8,000,000

Land Allocation at 20%: $1,600,000

Basis = Purchase Price − Land Allocation

Depreciable Basis: $6,400,000

Assume the study identifies 18% as 5-year property, 10% as 15-year land improvements, and the remaining assets retained in longer-life real property categories.

Reclassified basis:

- 5-year property: $1,152,000

- 15-year land improvements: $640,000

- Remaining real property: $4,608,000

The dominant value driver is often the combination of utility infrastructure, pads, site improvements, and supporting assets throughout the park.

This type of reclassification can substantially accelerate depreciation compared to treating the entire depreciable basis as 27.5-year residential rental property.

Actual results vary depending on park age, utility design, home ownership structure, site improvements, available documentation, and engineering findings.

Conclusion

Mobile home parks present some of the most attractive cost segregation opportunities in real estate because significant value often exists outside traditional buildings. Utility infrastructure, trailer pads, roads, drainage systems, site lighting, fencing, and other land improvements may represent substantial accelerated depreciation opportunities when properly analyzed.

The ownership structure of the community is equally important. Whether residents own the homes or the park owns the homes can materially affect classification, depreciation treatment, and study methodology.

A quality engineering-based cost segregation study evaluates each asset category independently, reconciles classifications to project costs, and follows established tax authority and IRS guidance. When performed correctly, mobile home park cost segregation can provide investors with improved cash flow, better tax planning visibility, and stronger long-term investment performance.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.