Cost Segregation for Land Improvement Heavy Businesses With Big Tax Value

Jun 16, 2026Some of the best cost segregation opportunities are not always found inside large buildings. Many specialty properties create tax value through 15-year land improvements, 5-year property, equipment, paving, drainage, lighting, fencing, utility infrastructure, signage, and dedicated systems. That is especially true for car washes, mobile home parks, marinas, RV parks, parking operations, storage yards, and other businesses where the site improvements may represent a major part of the depreciable basis. If your property does not have a large building, that does not automatically mean cost segregation is off the table.

Popular land improvement heavy property types include car washes, mobile home parks, manufactured housing communities, marinas, RV parks, campgrounds, outdoor boat and RV storage, paid parking lots, truck yards, contractor yards, equipment rental yards, self-storage facilities, drive-thru-heavy quick service restaurants, auto dealerships, and service centers.

Key Takeaways

- Land improvement heavy properties can create major tax value.

- Engineering analysis separates site assets from building property.

- Better depreciation timing can improve owner cash flow.

- Car washes, mobile home parks, and marinas often qualify.

- Timing and documentation make the strategy more effective.

- Basis math shows how reclassification can affect deductions.

- A defensible study ties classifications to real assets.

What Are Land Improvement Heavy Businesses?

Land improvement heavy businesses are properties where a meaningful share of the depreciable value sits outside the main building. Instead of relying mostly on 39-year nonresidential real property or 27.5-year residential rental property, these properties often include substantial 15-year land improvements and, in some cases, 5-year property.

The IRS Cost Segregation Audit Technique Guide identifies Asset Class 00.3 Land Improvement as a 15-year property category and includes depreciable improvements made directly to or added to land. Examples include sidewalks, roads, waterways, drainage facilities, sewers, wharves and docks, bridges, fences, landscaping, shrubbery, and similar improvements, while excluding buildings and structural components.

That framework matters for business owners who assume cost segregation only works for large apartment buildings, warehouses, retail centers, or office buildings. A car wash may have a small building, but large equipment, paving, drainage, signage, and dedicated systems. A mobile home park may have minimal building area when residents own the homes, but significant roads, pads, fencing, lighting, drainage, and utility infrastructure. A marina may have docks, wharves, ramps, parking, lighting, fencing, storage yards, and utility pedestals.

The tax and engineering logic is not based on whether the building is impressive. It is based on what the owner actually bought, built, improved, and placed in service. The study should separate non-depreciable land from depreciable assets, then classify those assets into the correct categories, including 5-year property, 15-year land improvements, QIP 15-year property where applicable, 27.5-year residential rental property, and 39-year nonresidential real property.

How Cost Segregation Works for Site Improvements and Specialty Assets

A land improvement heavy cost segregation study starts by identifying the full depreciable basis of the property. That usually means starting with the purchase price, separating land, then analyzing the remaining basis across buildings, site improvements, equipment, fixtures, and specialty systems.

A quality study should classify assets into property classes, explain the rationale for treating assets as § 1245 or § 1250 property, substantiate the cost basis of each asset, and reconcile the total allocated costs to the actual total costs. The ATG describes a quality study as accurate and well documented, with elements such as an experienced preparer, detailed methodology, appropriate documentation, engineering take-offs, organized asset lists, and reconciliation of allocated costs.

For land improvement heavy properties, the engineering review often focuses on items such as:

- Roadways, curbs, sidewalks, and parking areas

- Drainage systems, site utilities, and sewers

- Fencing, gates, bollards, and security infrastructure

- Site lighting, poles, pylons, and signage structures

- Pads, paved areas, ramps, docks, wharves, and storage yards

- Specialty equipment and dedicated support systems

- Business fixtures, payment systems, controls, and equipment connections

This is where classification details matter. A general building plumbing system usually remains part of the building. But a dedicated water or gas branch connected directly to qualifying equipment may receive different treatment when the facts support it. A general building electrical system is not the same as electrical infrastructure that supports qualifying equipment. The ATG’s discussion of electrical distribution systems recognizes a functional allocation concept that distinguishes power used for building operations from power used for equipment or qualifying business functions.

For owners who want a deeper asset-class explanation, this guide to cost segregation 15-year property is a useful starting point. For equipment and specialty assets, owners should also understand how 5-year property can apply when the facts and documentation support the classification.

Why This Can Matter More Than the Building Size

The biggest mistake many owners make is judging the opportunity by the size of the building. That can cause car wash owners, marina owners, mobile home park investors, and outdoor storage operators to overlook depreciation value sitting across the property.

Cost segregation is about depreciation timing. When part of the depreciable basis is classified as 15-year land improvements or 5-year property instead of 39-year nonresidential real property, deductions may move forward into earlier tax years. That can improve cash flow, support reinvestment, and help owners plan around debt service, expansion, repairs, and capital improvements.

This can be especially valuable for businesses that require ongoing reinvestment. Car washes need equipment maintenance, water systems, controls, signage, lighting, paving, and customer experience upgrades. Mobile home parks often need road repairs, pad work, utility improvements, drainage work, and common area maintenance. Marinas may need dock work, ramps, lighting, utility pedestals, storage areas, and waterfront infrastructure.

The opportunity is not automatic. Land itself is not depreciable. Some landscaping may be non-depreciable if it is inextricably associated with the land. Standard building components, roofs, walls, foundations, ordinary building lighting, general HVAC, standard plumbing, and standard electrical systems generally remain 39-year nonresidential real property or 27.5-year residential rental property. The study has to separate the real opportunity from items that should stay with the building.

That is why this strategy should be practical, not aggressive. The goal is not to call everything 15-year land improvements or 5-year property. The goal is to identify the assets that truly belong in those classes and document them well enough that the classifications make sense. For broader planning context, see how cost segregation benefits can support investor cash flow.

Popular Land Improvement Heavy Businesses to Review

Several property types should be evaluated before the owner assumes cost segregation is not worthwhile.

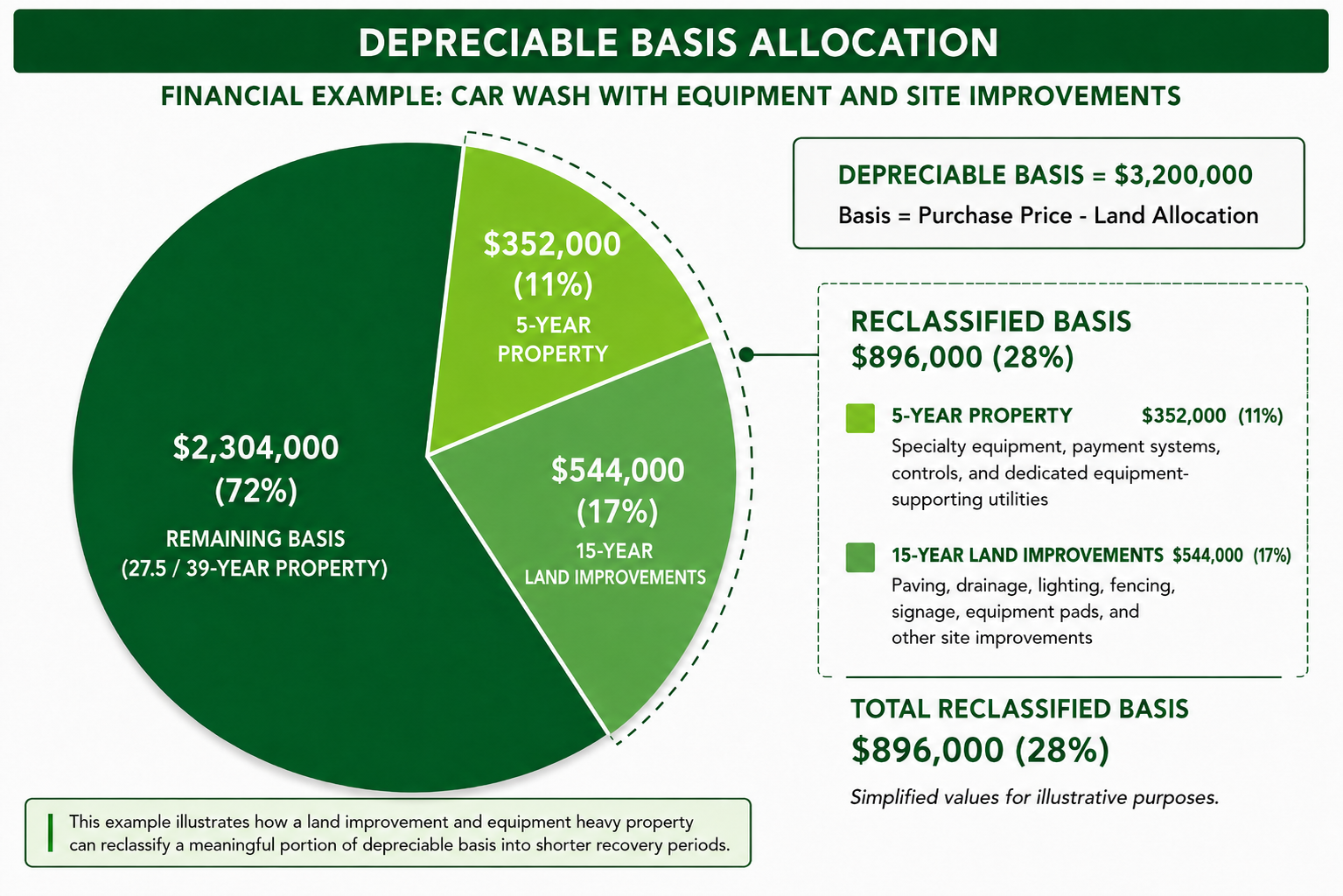

Car washes are often one of the strongest examples. The building may be modest compared with the total investment, while the business depends on specialty equipment, controls, water systems, reclaim systems, pumps, tanks, dedicated plumbing, dedicated electrical, equipment pads, drainage, paving, signage, curbs, lighting, and payment systems. In many car wash studies, 5-year property may be dominant over 15-year land improvements because the business relies so heavily on qualifying equipment and dedicated systems. The 15-year land improvements still matter, especially for paving, drainage, site lighting, curbs, signage structures, and other exterior improvements.

Mobile home parks and manufactured housing communities are another strong fit. When residents own the homes, the investor may own the land, infrastructure, roads, pads, utilities, fencing, lighting, drainage, sidewalks, signage, common areas, and perhaps a small office or clubhouse. The owner may not have a large apartment-style building basis, but the property may include meaningful 15-year land improvements. If the investor owns rental homes inside the park, those assets need separate analysis because some may involve 27.5-year residential rental property and other classifications.

Marinas can also be strong candidates, although they are more specialized. A marina may include docks, wharves, boat slips, ramps, parking areas, storage yards, utility pedestals, lighting, fencing, gates, signage, drainage, and service areas. The ATG specifically includes wharves and docks among examples that may fall under Asset Class 00.3 Land Improvement when the improvements are depreciable. The study still needs to review the facts because some assets may be tied to other classifications, and waterfront properties often have unique documentation and valuation issues.

RV parks and campgrounds can look similar to mobile home parks. They may include pads, roads, hookups, bathhouse support, drainage, site lighting, fencing, landscaping, signage, and recreational improvements. Outdoor boat and RV storage can be even more site-driven, with paving, gravel, fencing, gates, lighting, security systems, drainage, signage, and minimal building value.

Paid parking lots, truck yards, contractor yards, and equipment rental yards can also fit the strategy. The ATG identifies grade-level parking lots as 15-year land improvements and includes items such as asphalt, concrete or similar surfaces, bumper blocks, curb cuts, curb work, striping, landscape islands, perimeter fences, sidewalks, and traffic control systems.

Self-storage facilities, drive-thru-heavy quick service restaurants, auto dealerships, and service centers may also benefit, but they are more mixed. These properties often have meaningful buildings, but they may also have substantial paving, lighting, gates, security, signage, drive lanes, bollards, drainage, display lots, and dedicated equipment systems. The right answer depends on the asset mix, not the property label.

How Owners Should Plan the Study

The best time to evaluate cost segregation is usually right after acquisition, construction, or a major improvement project. That is when settlement statements, appraisals, drawings, invoices, contractor schedules, site plans, and equipment records are easier to access. Better documentation usually leads to better classification support.

For acquired properties, the first step is separating land from the purchase price. Land is not depreciable, so the study should use a reasonable land allocation before analyzing the remaining depreciable basis. After that, the study can allocate costs to building components, 15-year land improvements, 5-year property, and other relevant categories.

For newly constructed or renovated properties, the study team should review actual cost records when available. That can include contractor invoices, payment applications, equipment schedules, site drawings, utility plans, electrical plans, plumbing plans, and change orders. If actual costs are not detailed enough, engineering estimates may be needed.

Owners should also involve their CPA early. Cost segregation affects depreciation, but the benefit depends on the taxpayer’s broader position. Passive activity rules, bonus depreciation eligibility, placed-in-service dates, material participation, entity structure, financing, and future sale plans can all influence the outcome.

This is especially important for owners who bought the property in a prior year. A cost segregation study may still be useful through a change in accounting method, subject to CPA review. That can allow the owner to adjust depreciation without amending prior returns in many situations.

A defensible study should not rely on generic percentages. Land improvement heavy properties need a careful asset review because every site is different. A tunnel car wash, self-serve car wash, express wash, mobile home park, marina, RV campground, and storage yard can all have very different asset mixes. This article on a quality cost segregation study explains why documentation and methodology matter.

The Bottom Line for Land Improvement Heavy Businesses

Cost segregation is not only a building strategy. For many specialty businesses, the tax value may be spread across the site, equipment, infrastructure, and dedicated systems. Car washes, mobile home parks, marinas, RV parks, parking operations, storage yards, and similar properties should not be dismissed just because the main building is small.

The key is using an engineering method that matches the property. The study should identify the assets, inspect the site, review available records, separate non-depreciable land, classify 5-year property and 15-year land improvements where supported, and leave structural components in 27.5-year residential rental property or 39-year nonresidential real property where appropriate.

When the facts support the classifications, land improvement heavy businesses can use cost segregation to improve depreciation timing, increase planning visibility, and support cash flow. The opportunity is not based on whether the building dominates the property. It is based on what the owner actually owns, operates, and places in service.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.