Electrical Distribution Systems in Cost Segregation Studies

May 12, 2026Electrical distribution systems can be one of the most technical areas in a cost segregation study. For many investors, electrical work looks like one large building system, but tax classification depends on what the system serves. General building power is usually treated differently than electrical infrastructure dedicated to qualifying equipment. When the study uses engineering support, load analysis, and proper documentation, EDS classification can improve depreciation results while staying aligned with established IRS audit guidance.

Key Takeaways

- EDS classification separates building power from equipment power.

- Functional allocation ties electrical costs to supported assets.

- Correct EDS treatment can improve cash flow materially.

- EDS analysis applies across equipment-heavy property types.

- Planning documents help support stronger electrical allocations.

- A realistic allocation can shift major basis forward.

- Defensible EDS results require engineering support and tax alignment.

How EDS Classification Separates Building Power From Equipment Power

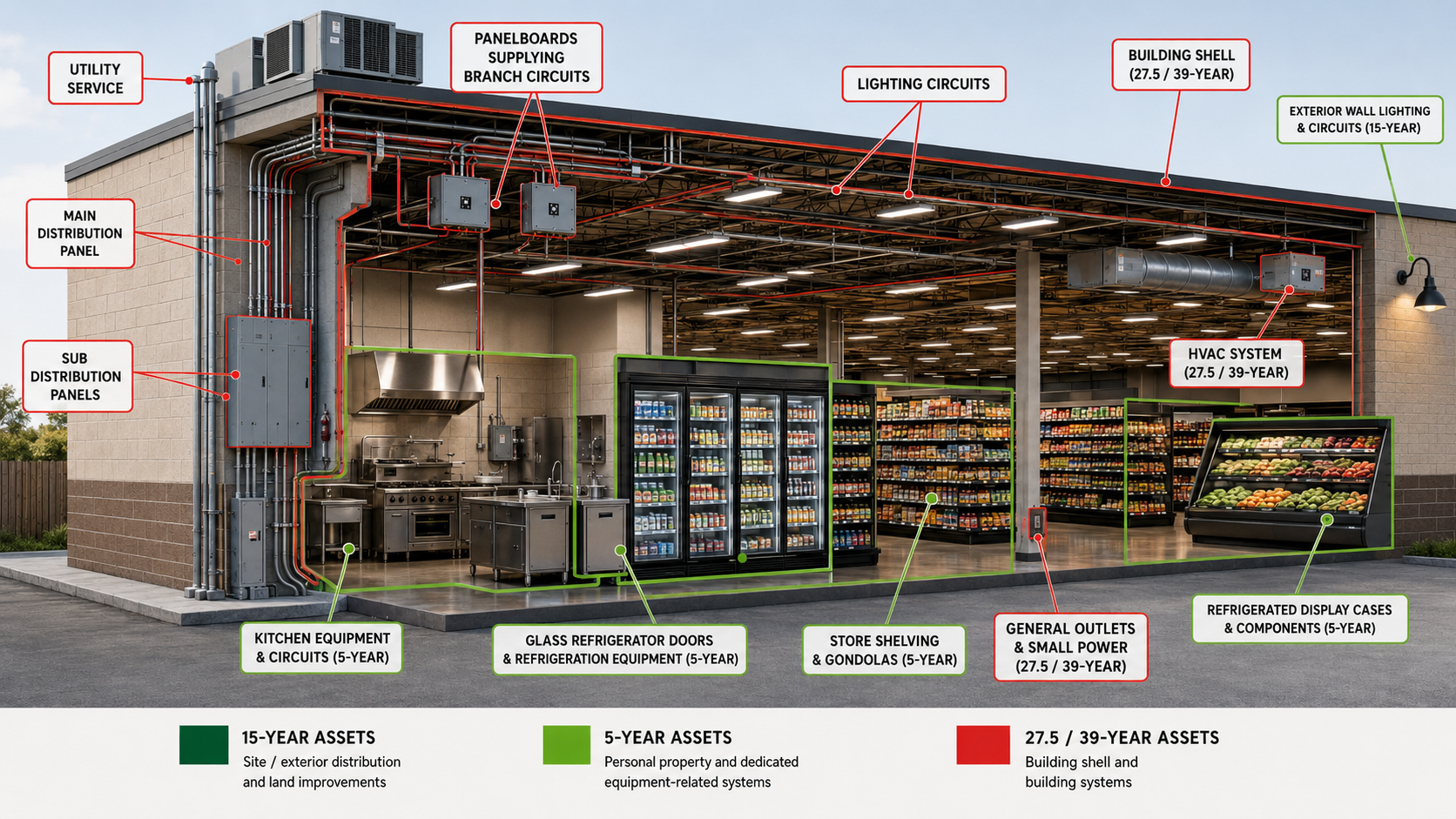

An electrical distribution system, often called EDS, includes the infrastructure that moves power through a building. Depending on the property, that may include service entrance equipment, transformers, switchgear, panels, subpanels, conduit, feeder wiring, branch circuits, breakers, and dedicated electrical connections.

In cost segregation, the core question is not simply whether the system is electrical. The question is what each portion of the system does. Electrical components that support general building operations are typically associated with § 1250 real property. That includes power for general lighting, HVAC, common-use outlets, and other systems that operate or maintain the building.

By contrast, electrical components that are necessary for, and directly connected to, qualifying machinery or equipment may support § 1245 personal property treatment. A common example is a dedicated circuit serving a specific piece of equipment. This is why investors should understand the distinction between dedicated vs general purpose electrical outlets. A general outlet in a room is not the same as a dedicated electrical connection designed for a specific qualifying asset.

This classification logic is consistent with the broader tax and engineering framework used in cost segregation. The system must be reviewed by function, design, connection, and support role. A broad estimate is not enough when electrical costs are significant.

How Functional Allocation Works in an Engineering Study

The functional allocation approach is used when an electrical distribution system supports both building operations and qualifying personal property. Instead of treating the entire system as one category, the study allocates costs based on the power demand served by different end uses.

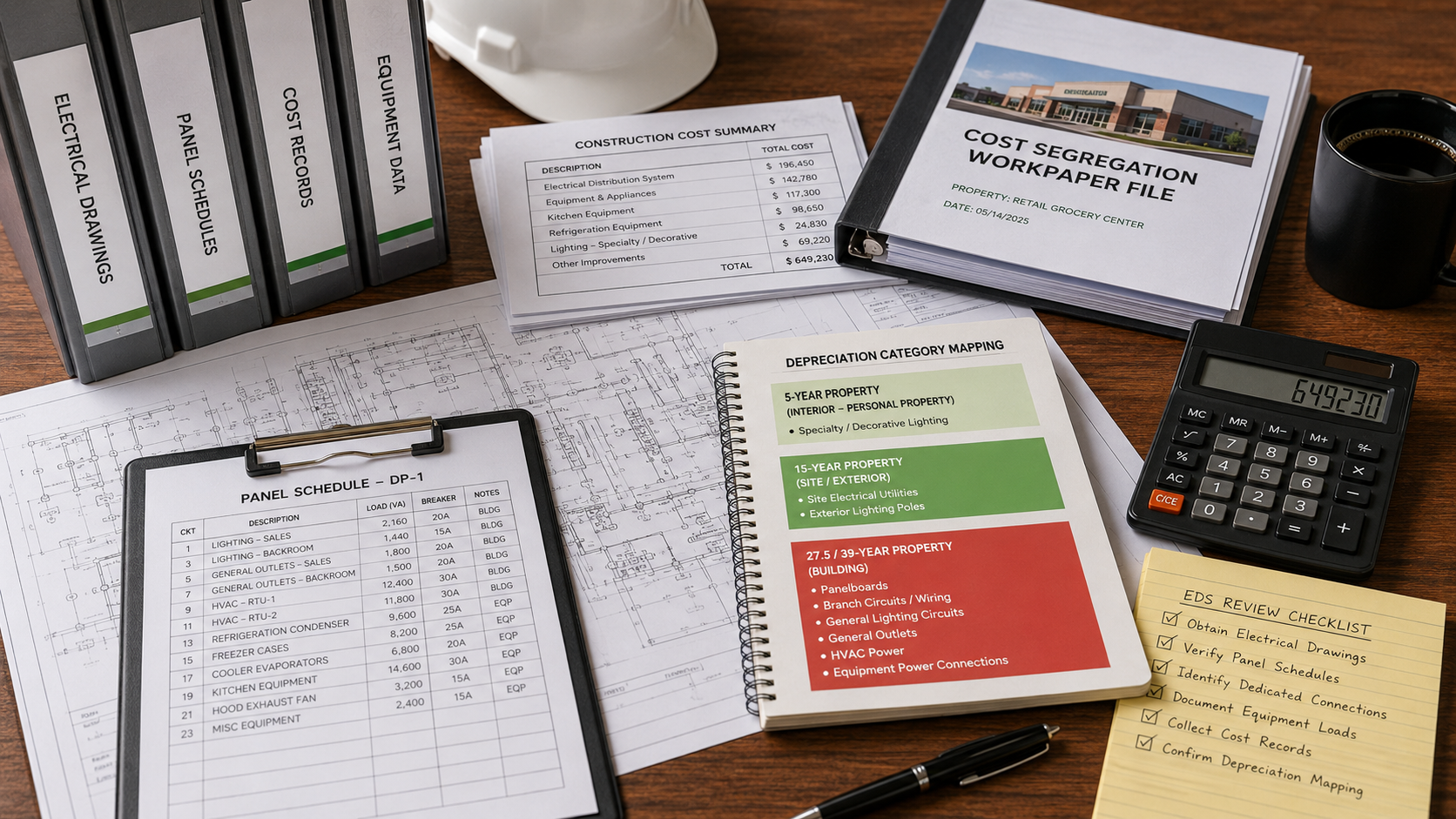

In practice, the engineering team reviews electrical drawings, panel schedules, load calculations, equipment lists, and site conditions. The goal is to determine what portion of the EDS supports general building functions and what portion supports qualifying equipment. The analysis may separate service entrance equipment, primary distribution, secondary distribution, branch circuits, and dedicated equipment connections.

For example, a grocery store may use a large share of its power for refrigeration compressors, kitchen equipment, food preparation equipment, signs, and other specialized assets. Those loads are different from lighting, HVAC, office outlets, or general building power. The study should identify the demand load associated with each use and allocate the electrical distribution cost accordingly.

This is also where asset classification discipline matters. Not every electrical item should be pushed into short-life property. A defensible study distinguishes between electrical infrastructure used for building operation and electrical infrastructure directly supporting qualifying assets. That distinction connects closely to broader 5-year property analysis, because many equipment-related electrical components may follow the recovery period of the qualifying asset they serve.

The best studies do not rely on shortcuts. They use drawings, engineering takeoffs, interviews, photographs, and reconciliation to the total project cost or purchase price allocation. That is what separates a technical EDS allocation from a rough percentage.

Why EDS Treatment Can Change Investor Cash Flow

EDS classification can create meaningful tax timing differences because building property and personal property recover over very different periods. Nonresidential real property is generally depreciated over 39 years. Residential rental property is generally depreciated over 27.5 years. Qualifying personal property may often fall into shorter recovery periods, commonly 5 or 7 years depending on the asset class and use.

For an investor, that timing difference can affect first-year deductions, taxable income, and cash flow planning. The tax benefit is not created by inventing deductions. It comes from identifying the correct recovery period for each asset based on its use and classification.

Electrical systems are especially important in properties with significant equipment loads. A warehouse with specialized processing equipment, a restaurant with kitchen equipment, a medical facility with dedicated equipment connections, or a grocery store with refrigeration systems may have more EDS classification opportunity than a simple office building.

The risk is overreach. If a study treats general building electrical work as short-life property without support, the allocation can become vulnerable under review. Investors should avoid strategies that chase aggressive percentages without engineering evidence. That is why short-life asset classification risks are especially relevant when electrical costs are large.

A strong EDS allocation improves cash flow because it is specific, documented, and connected to actual equipment use. A weak allocation increases audit exposure because it depends on assumptions rather than engineering support.

Where EDS Analysis Applies Across Property Types

EDS analysis is most valuable when a property has meaningful electrical loads tied to equipment, operations, or specialized tenant improvements. It is common in commercial, industrial, retail, hospitality, restaurant, medical, manufacturing, and certain residential rental settings.

Restaurants may have dedicated electrical connections for ovens, refrigeration, dishwashing equipment, prep equipment, and point-of-sale systems. Grocery stores and convenience stores may have electrical loads tied to coolers, freezers, compressors, food service equipment, signage, and backroom equipment. Medical and dental offices may have dedicated power for imaging, sterilization, lab, or procedure equipment. Manufacturing and production facilities may have process equipment with dedicated distribution needs.

Residential rental property can also include EDS analysis, but the opportunity depends on the facts. Dedicated electrical connections for appliances may be treated differently from general branch circuits and common building power. The same principle applies. The study must determine whether the electrical component supports general building operations or a specific qualifying asset.

This is where property type matters, but facts matter more. A multifamily building, restaurant, and manufacturing facility may all have electrical systems, but the allocation logic changes based on the end-use equipment, design loads, and documentation. A good study does not force one template onto every property. It evaluates the actual system.

Planning EDS Documentation Before the Study Starts

The best time to support EDS classification is before the study begins. Investors who have access to electrical drawings, construction invoices, panel schedules, equipment specifications, and tenant improvement documents can help the engineering team classify assets more accurately.

For acquired properties, documentation may be incomplete. In that case, the site inspection becomes more important. Photographs, equipment nameplates, observed dedicated connections, breaker panels, and field notes can help support the allocation. For newly built or renovated properties, construction records can provide a stronger basis for tracing electrical costs to specific systems and assets.

Investors should also coordinate the study timing with purchase, renovation, or placed-in-service planning. Electrical data is easier to capture when contractors, architects, and project managers are still available. Once a project closes out and records get scattered, the study may require more estimation.

EDS planning should also fit within the broader study methodology. The electrical allocation must reconcile back to the total depreciable basis. It should not create unsupported costs or double count assets already classified elsewhere. This is one reason investors benefit from understanding what makes a quality cost segregation study. The report should explain the methodology, documentation, assumptions, and asset groupings clearly enough for review.

Financial Example: Supermarket EDS Allocation and First-Year Tax Impact

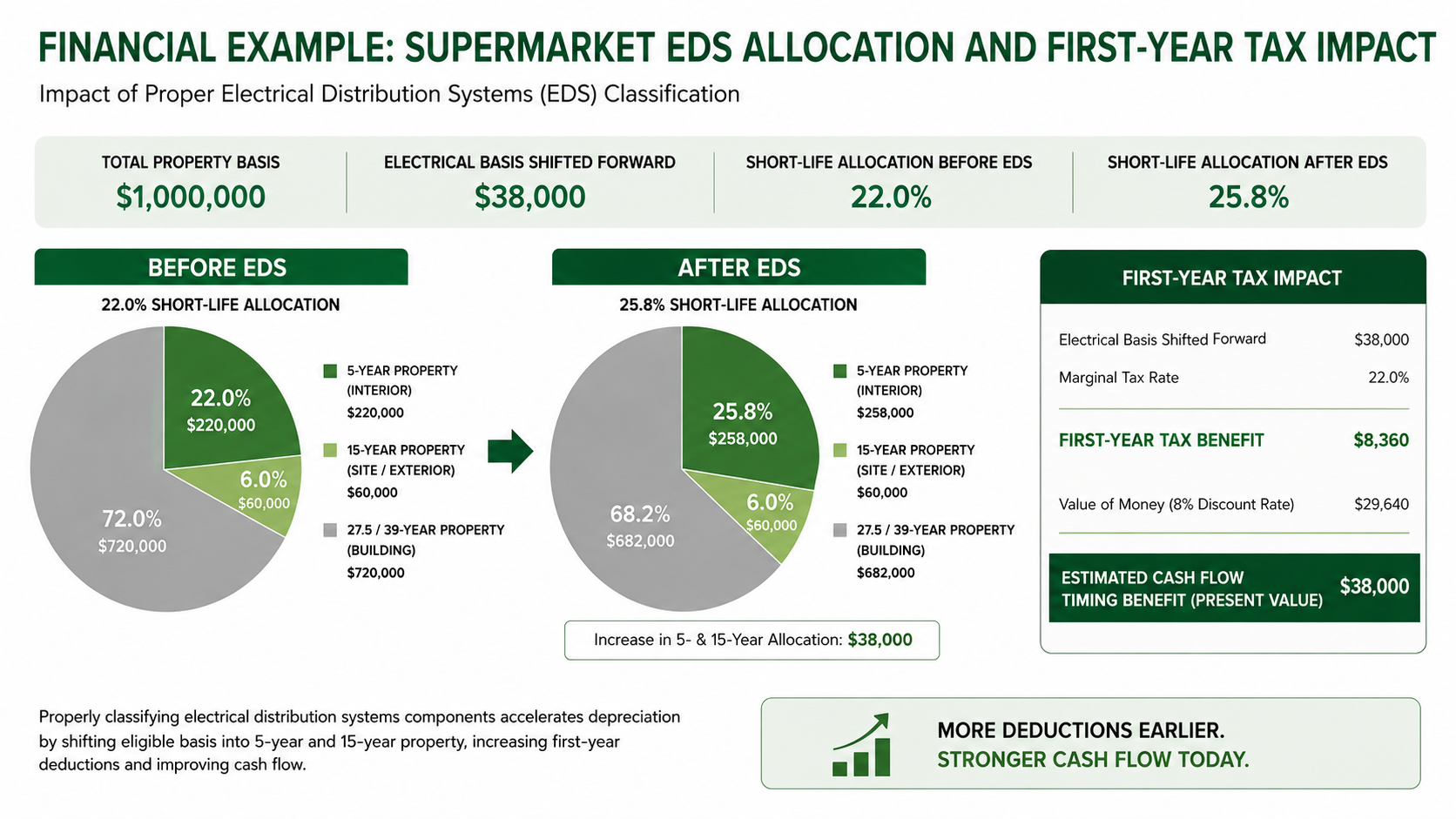

Consider an investor who purchases a grocery-anchored retail property with a $1,000,000 depreciable building basis allocated to cost segregation analysis. The property includes refrigeration systems, food preparation equipment, display cases, compressors, specialized signage, and general building systems.

Assume the study identifies $220,000, or 22% of the depreciable basis, as short-life property before considering the electrical distribution allocation. Most of that short-life basis is 5-year property tied to equipment, fixtures, and dedicated connections. The remaining basis is primarily 39-year nonresidential real property, with some 15-year land improvements.

Now assume the building has a $100,000 electrical distribution system cost embedded in the project basis. After reviewing panel schedules and demand loads, the engineering team determines that 38% of the EDS supports qualifying equipment and 62% supports general building operations. That shifts $38,000 of EDS basis into shorter-life property and leaves $62,000 as 39-year building property.

The result is a revised short-life allocation of $258,000, or 25.8% of the $1,000,000 basis. That is within the range investors often see when a property has meaningful equipment and specialty systems, but it is supported by a specific engineering analysis rather than a flat assumption.

For tax timing, the difference can be significant. Without cost segregation, the $1,000,000 building basis would generally be depreciated over 39 years, producing roughly $25,641 of annual depreciation before conventions. With the study, $258,000 is moved into accelerated recovery categories, with the 5-year category carrying the largest share of the reclassification. Depending on the placed-in-service date, tax profile, and bonus depreciation rules in effect, the first-year deduction can increase materially compared with straight-line depreciation.

For an investor in a 37% federal tax bracket, every additional $50,000 of first-year depreciation may represent up to $18,500 of federal tax deferral. The exact result depends on passive activity rules, taxable income, state taxes, financing, and the investor’s broader tax situation. The key point is that a properly supported EDS allocation can turn hidden electrical costs into measurable cash flow timing benefits.

Closing: Defensible EDS Results Come From Engineering Support

Electrical distribution systems are not a simple checkbox in a cost segregation study. They require technical review, asset classification judgment, and documentation that connects electrical costs to the property’s actual use.

The strongest results come from engineering methodology, not rule-of-thumb percentages. A defensible EDS allocation identifies what the system serves, separates building power from equipment power, reconciles costs, and aligns the tax treatment with established classification principles.

For investors, the upside is practical. A well-supported EDS analysis can increase accelerated depreciation, improve after-tax cash flow, and create a clearer record if the study is ever reviewed. The goal is not to classify more electrical cost as short-life property at any cost. The goal is to classify the right electrical costs correctly.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.