Form 3115 for Cost Segregation: Fix Depreciation the Right Way

May 21, 2026Form 3115 is one of the most important forms real estate investors encounter after a cost segregation study on a property they already placed in service. It is used to request a change in accounting method when prior depreciation was calculated using the wrong recovery period, depreciation method, or convention. In cost segregation, that usually means a building was depreciated too slowly as 27.5-year or 39-year property when part of the basis should have been classified as shorter-life property. When used correctly, Form 3115 allows investors to catch up missed depreciation through a Section 481(a) adjustment instead of trying to amend several old returns.

Key Takeaways

- Form 3115 corrects adopted depreciation methods for prior-year properties.

- The form connects engineering classifications to tax accounting changes.

- A proper filing can unlock missed depreciation and cash flow.

- Form 3115 often applies to acquired, renovated, or older rentals.

- Timing the study and filing prevents avoidable compliance problems.

- A Section 481(a) adjustment can create major first-year deductions.

- The safest approach combines engineering support with tax procedure.

Understanding Form 3115 in Cost Segregation

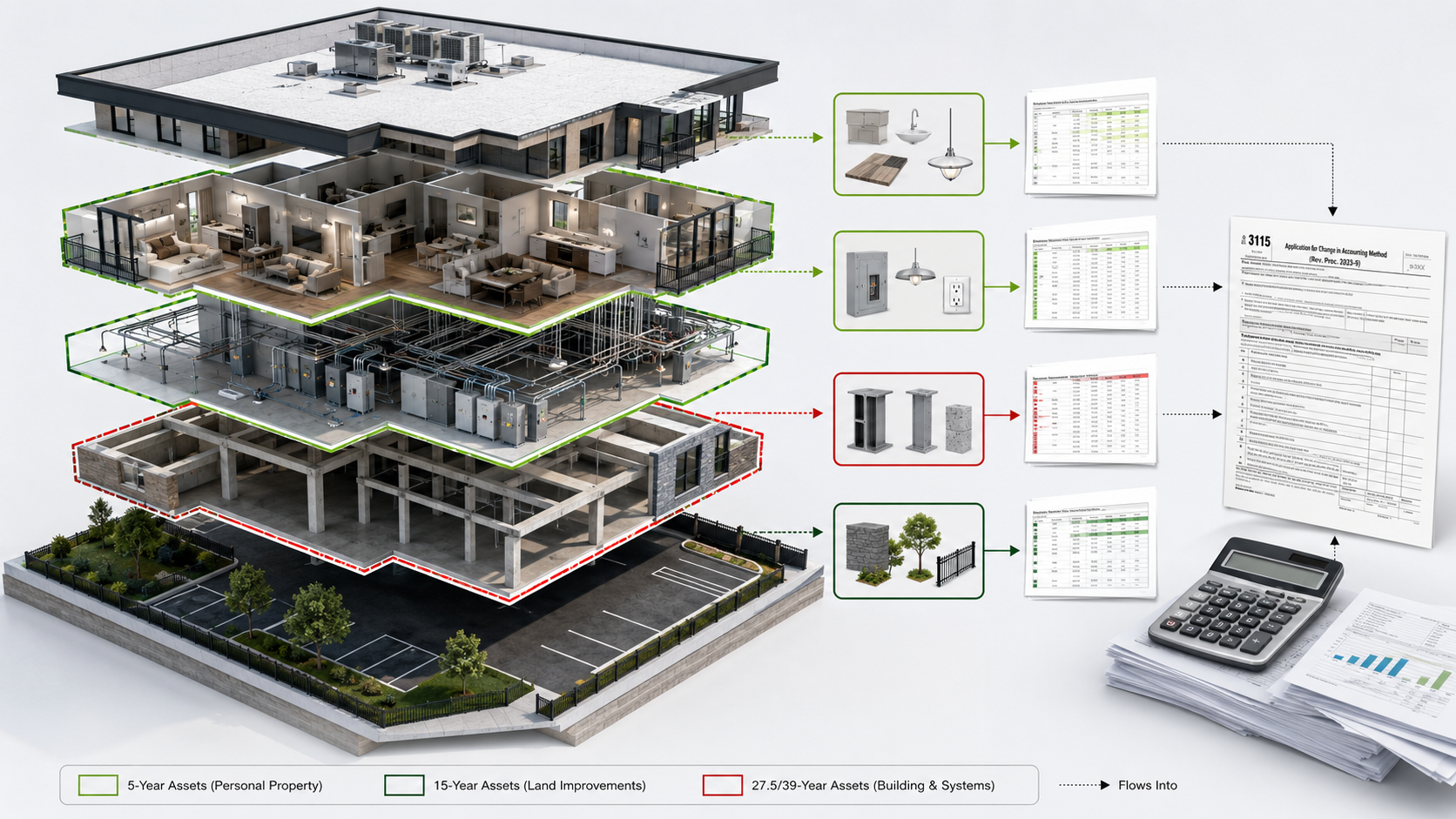

Form 3115, Application for Change in Accounting Method, is the IRS form used when a taxpayer needs permission to change how an item is treated for tax accounting purposes. In cost segregation, the key issue is depreciation. If a taxpayer has already adopted a depreciation method for a property, then later reclassifies part of the building into 5-year, 7-year, or 15-year property, the IRS generally views that as a change in accounting method.

This matters because cost segregation is not just a tax estimate. It is an engineering-based allocation of building costs into assets with different tax lives. The IRS Cost Segregation Audit Technique Guide explains that changes to depreciation method, recovery period, or convention resulting from property reclassification generally require Commissioner consent through Form 3115, with the income adjustment handled under Section 481(a).

For investors, this is where tax engineering and tax procedure meet. The study identifies the assets. Form 3115 is the procedural mechanism that tells the IRS the taxpayer is changing from an impermissible or less accurate depreciation method to a permissible one.

How Form 3115 Connects the Study to the Tax Return

A cost segregation study breaks down the property into tax categories. Some assets may remain 27.5-year residential rental property or 39-year nonresidential real property. Other assets may qualify as 5-year personal property, 7-year property, or 15-year land improvements. That asset classification is the foundation for accelerated depreciation.

Form 3115 becomes relevant when the property was already placed in service and at least one later return has already been filed using the old depreciation method. At that point, the taxpayer typically should not just amend old returns to “fix” the depreciation. The ATG states that once a method has been adopted, taxpayers are generally required to file Form 3115 under automatic or non-automatic change procedures, rather than changing the adopted method by amended return unless specific guidance allows it.

In practice, the process usually works like this. First, the cost segregation provider completes the engineering study and asset schedule. Second, the tax preparer calculates the depreciation that should have been taken under the corrected classifications. Third, the preparer compares that amount to the depreciation actually taken. Fourth, the difference becomes the Section 481(a) adjustment. Fifth, Form 3115 is attached to the timely filed federal return for the year of change, and for automatic changes, a duplicate copy is sent to the IRS office in Ogden, Utah within the required filing window.

This is why a quality cost segregation study matters. The tax preparer needs clear asset descriptions, placed-in-service dates, cost basis support, depreciation classifications, and methodology that can support the Form 3115 adjustment.

Why Form 3115 Matters for Investor Cash Flow

The main value of Form 3115 is that it can allow a real estate investor to claim missed depreciation in the current year through a catch-up adjustment. That can be powerful when an investor bought a property several years ago, depreciated the whole building over 27.5 or 39 years, and only later learned that a cost segregation study could have accelerated part of the basis.

Without Form 3115, the investor may lose timing efficiency or create procedural risk by trying to amend returns when a method change is required. With Form 3115, the investor has a path to align prior depreciation with the asset classifications from the study and bring the cumulative adjustment into the year of change.

The cash flow impact can be substantial. Cost segregation already helps investors reduce taxes and increase cash flow by moving eligible costs into shorter recovery periods. Form 3115 adds another layer because it can capture the missed depreciation from prior years instead of only improving depreciation going forward.

Investors should still avoid treating Form 3115 as a shortcut. The IRS focuses on whether the new method is permissible, whether the Section 481(a) adjustment is correct, and whether the underlying study supports the reclassification. The ATG lists common compliance issues such as incorrect revenue procedure use, failure to file Form 3115, lack of records to substantiate the Section 481(a) adjustment, and lack of detail to determine basis and recovery periods.

Where Form 3115 Commonly Applies

Form 3115 is most common when an investor completes a cost segregation study after the property has already been placed in service and tax returns have already been filed. This can happen with apartment buildings, short-term rentals, medical offices, retail centers, warehouses, self-storage facilities, industrial buildings, and mixed-use properties.

It is especially relevant for investors who acquired a property in a prior year and did not complete the study before filing the first tax return for that property. It can also apply when prior depreciation was calculated using broad straight-line treatment, then a later study identifies shorter-life assets. For investors comparing acceleration against conventional depreciation, cost segregation vs straight-line depreciation is the core planning issue.

Renovations can create additional opportunities and complexity. A commercial interior improvement may involve Qualified Improvement Property, 5-year personal property, 15-year land improvements, and 39-year building components. Residential renovation projects may include appliances, flooring, specialty electrical, site improvements, and other assets that need classification support. In these situations, Form 3115 may be part of the cleanup if the project was already filed using an overly broad depreciation treatment.

Bonus depreciation can also affect the analysis. If shorter-life assets are identified after the original return was filed, the taxpayer may need to determine whether bonus depreciation should have been claimed, whether an election out applied, and whether the correction now requires Form 3115. The ATG notes that when a cost segregation study is performed after the placed-in-service year return and later return have already been filed, the taxpayer may have adopted an impermissible method and may need Form 3115 to change to a permissible method.

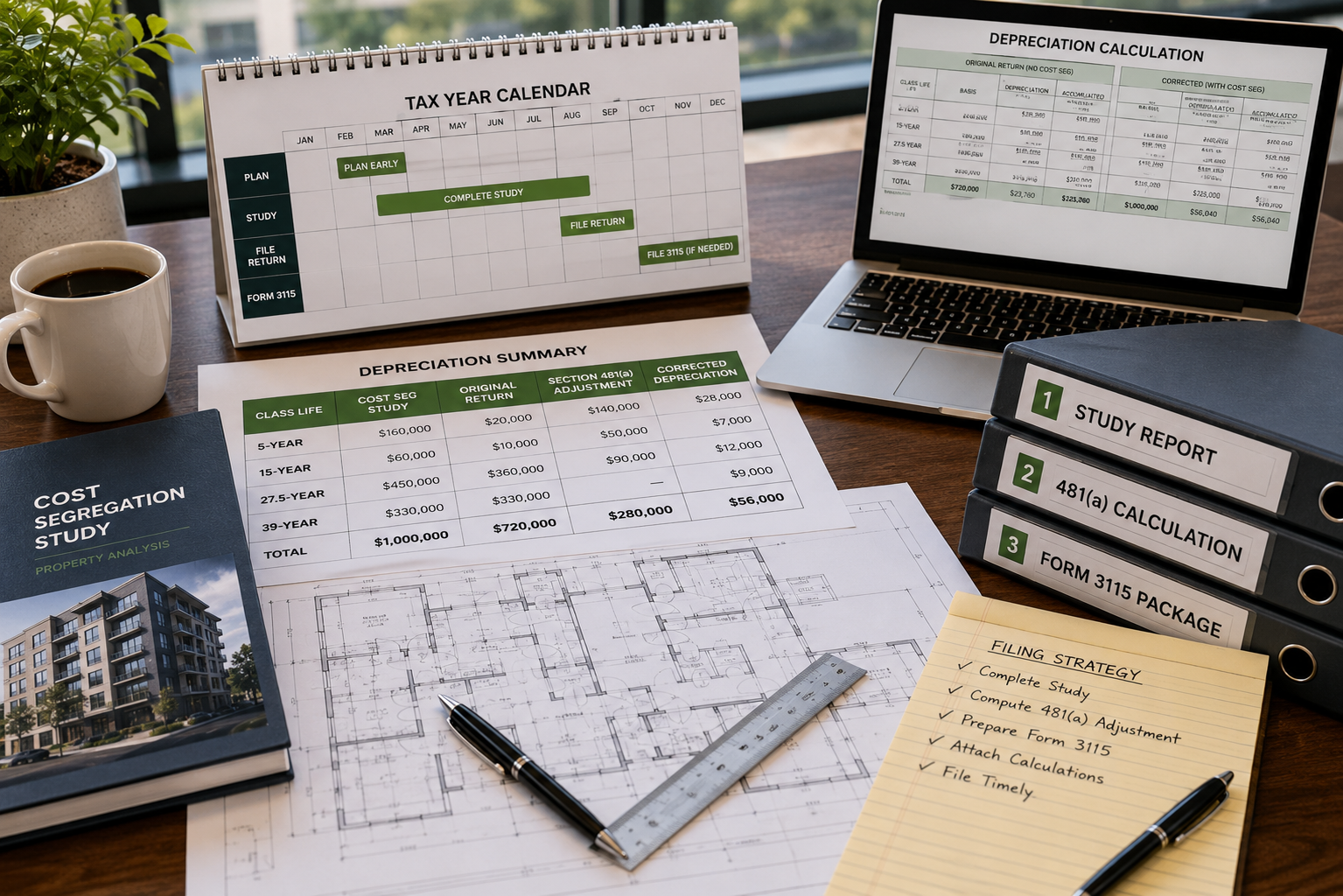

Planning the Form 3115 Filing Correctly

The best strategy is to complete the cost segregation study before the first return is filed for the property. When that happens, the taxpayer can usually report the correct depreciation from the beginning and avoid the additional complexity of a method change. That is why timing a cost segregation study matters so much.

When the study happens later, the investor and tax preparer need to coordinate carefully. The study should provide a detailed asset schedule with clear classifications and support. The CPA should determine whether the change qualifies for automatic consent or requires non-automatic procedures. The Section 481(a) adjustment must be calculated accurately, because this is the number that catches up the depreciation difference between the old method and the corrected method.

Execution also matters. For an automatic change, the original Form 3115 generally must be attached to the timely filed original federal income tax return for the year of change, including extensions. A duplicate copy must also be filed with the IRS office in Ogden, Utah no earlier than the first day of the year of change and no later than the date the original Form 3115 is filed with the federal return.

The investor should not try to handle this as a casual paperwork step. The classification work, depreciation schedules, Section 481(a) adjustment, and filing procedure all need to match. Mistakes can weaken the tax position even if the underlying cost segregation opportunity is real.

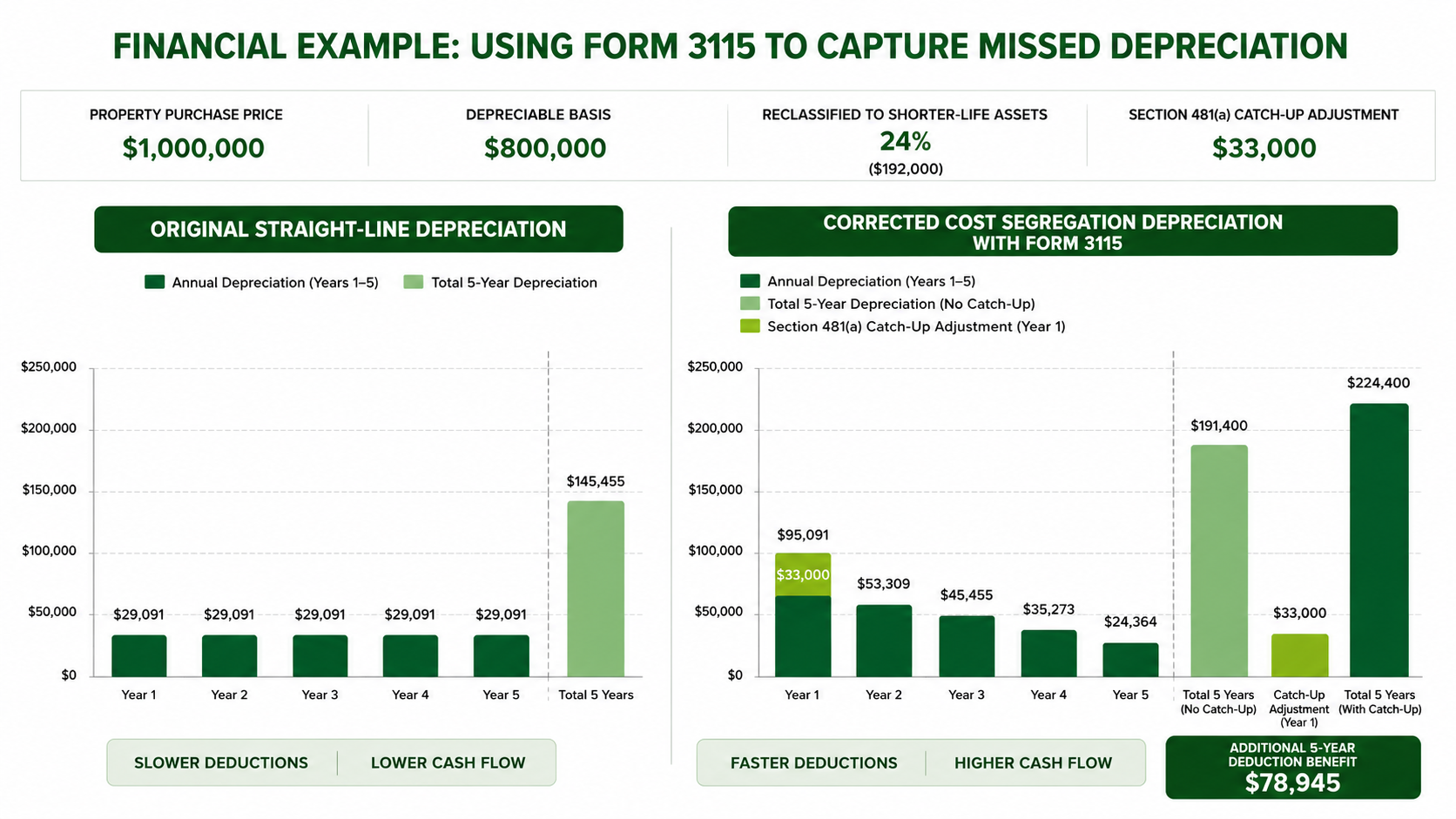

Financial Example: Using Form 3115 to Capture Missed Depreciation

Assume an investor purchased a $1,000,000 residential rental property three years ago. After allocating value to land, the depreciable building basis is $800,000. The investor originally depreciated the full $800,000 over 27.5 years using straight-line depreciation.

Three years later, the investor completes a cost segregation study. The study supports reclassifying 24% of the depreciable basis, or $192,000, into shorter-life assets. Most of the reclassified amount is 5-year property, with a smaller portion classified as 15-year land improvements. This is within the common 17% to 28% range often seen in supported studies, while results up to 32% should only be used when the engineering facts and documentation justify it.

If the investor should have claimed significantly more depreciation in the prior years, the CPA calculates the missed depreciation as a Section 481(a) adjustment. Instead of going back to amend multiple prior returns, Form 3115 may allow the taxpayer to claim that cumulative catch-up adjustment in the current year.

For example, if the corrected depreciation through the prior years should have been $120,000 and the investor only claimed $87,000, the Section 481(a) adjustment could be $33,000. That $33,000 deduction may reduce taxable income in the year of change, improving cash flow. If the investor is in a 35% combined tax bracket, that could represent approximately $11,550 in tax deferral value.

The real benefit depends on the property, basis, tax position, passive activity rules, bonus depreciation eligibility, and the investor’s broader income picture. But the logic is clear. Form 3115 can turn a late cost segregation study into a current-year planning tool when the filing is handled correctly.

The Right Way to Fix Depreciation

Form 3115 is not just an IRS form. It is the bridge between a cost segregation study and a corrected depreciation method for a property already filed on prior tax returns. When the study is engineering-based and the tax preparer calculates the Section 481(a) adjustment correctly, the investor can often capture missed depreciation while staying aligned with established tax procedure.

The safest approach starts with asset-level engineering support. It continues with careful classification under MACRS, accurate recovery periods, and a clear depreciation comparison between the old method and the corrected method. It ends with a Form 3115 filing that follows the applicable revenue procedure and gives the taxpayer a defensible path for the change.

For investors, the lesson is simple. Do the study early when possible. If the study happens later, do not treat the fix as a basic amendment decision. Form 3115 may be the right tool, but only when the numbers, documentation, and filing steps are handled with care.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.