How to Defend 5-Year Property in an IRS Cost Seg Audit

May 19, 2026An IRS cost segregation audit usually comes down to one question: can the study defend why certain assets were classified as shorter-life property? For investors, 5-year property is especially important because it can accelerate depreciation, improve early cash flow, and increase the value of a cost segregation strategy. But 5-year classifications also need clear support because the IRS looks closely at whether an asset is truly § 1245 tangible personal property or part of the building. A defensible study does not rely on broad percentages or assumptions. It connects each classification to engineering analysis, documentation, and tax treatment that aligns with established cost segregation principles.

Key Takeaways

- 5-year property requires a defensible § 1245 classification, not assumptions.

- Engineering methods connect asset use, cost data, and depreciation categories.

- Defensible classifications protect deductions, cash flow, and investor confidence.

- Audit issues often involve electrical, finishes, appliances, and specialty assets.

- Strong documentation should be built before an IRS review begins.

- A $1,000,000 study shows how support protects accelerated deductions.

- IRS alignment starts with engineering, documentation, and disciplined classification.

Why 5-Year Property Drives IRS Audit Questions

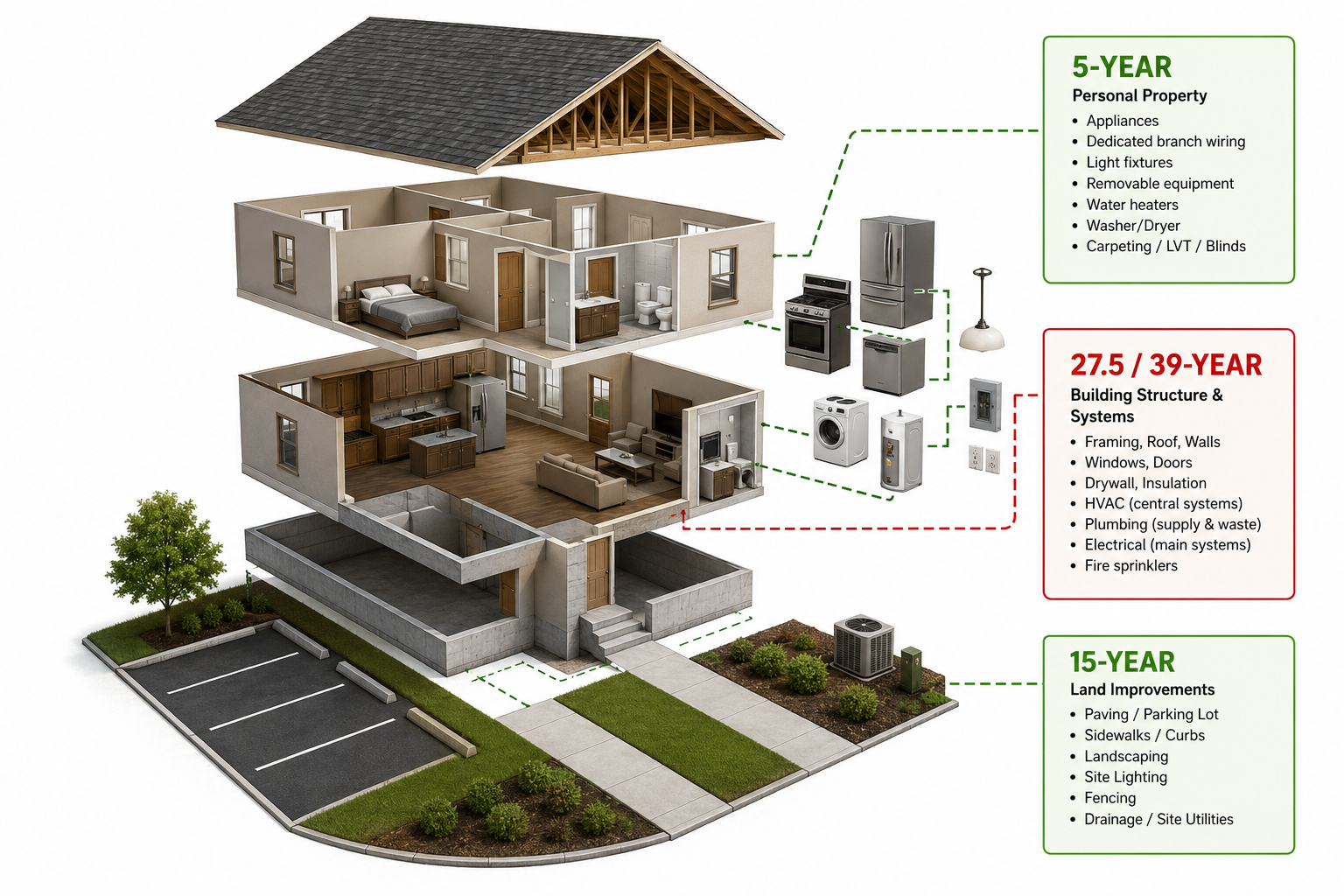

In cost segregation, 5-year property generally refers to shorter-life assets that can be classified as § 1245 tangible personal property under MACRS. These assets are different from § 1250 real property, which generally includes buildings and structural components depreciated over 27.5 years for residential rental property or 39 years for nonresidential real property. The classification matters because § 1245 property can often qualify for faster depreciation than the building itself.

The IRS Cost Segregation Audit Technique Guide focuses heavily on the distinction between § 1245 and § 1250 property. A study must show why an item is not simply part of the building’s operation or maintenance. Furniture, equipment, certain removable finishes, appliances, and dedicated systems may qualify, but the facts matter. A classification is stronger when the asset’s function, attachment, removability, and relationship to the business use are documented.

This is why investors should not view a cost segregation study as a spreadsheet exercise. A quality cost segregation study explains what was classified, why it was classified that way, and how the costs were assigned. In an audit, that explanation is often more valuable than the deduction itself.

How Engineers Classify Defensible 5-Year Assets

A defensible 5-year property classification begins with asset identification. The engineer reviews building components, purchase records, construction documents, site photos, invoices, and property use. The goal is to separate assets into proper depreciation categories based on function and tax treatment, not just appearance.

For example, a refrigerator in a residential rental unit may be treated differently from kitchen cabinets, counters, plumbing, and general electrical wiring. Dedicated branch wiring that serves qualifying equipment may be analyzed separately from wiring that serves general building functions. In commercial properties, specialty equipment, removable partitions, decorative elements, or business-specific systems may require item-by-item review.

The IRS ATG gives significant attention to methodology. Detailed engineering approaches are stronger than rule-of-thumb estimates because they connect actual property conditions to cost allocations. A defensible study should include clear asset descriptions, cost sources, allocation logic, depreciation categories, and reconciliation to total project or purchase cost. This is also where investors should be careful about short-life asset classification risks, because overreaching can weaken the entire study.

Why Defensible Classifications Protect Investor Cash Flow

The financial benefit of 5-year property comes from timing. Moving supported costs from 27.5-year or 39-year depreciation into 5-year property can front-load deductions, which may reduce taxable income and improve after-tax cash flow. For investors using bonus depreciation when available, those shorter-life classifications can have an even larger near-term impact.

But the value of the deduction depends on the strength of the support. If an IRS examiner challenges a classification and the study cannot defend it, the investor may face reclassification, reduced deductions, amended tax exposure, interest, or penalties depending on the facts. A larger deduction is not better if it cannot survive review.

That is why audit defense should be part of the ROI discussion from the beginning. The right question is not only how much depreciation can be accelerated. The better question is how much can be accelerated with documentation that supports the position. When done correctly, cost segregation benefits are tied to both tax savings and technical credibility.

Where 5-Year Property Issues Show Up Most Often

Audit questions around 5-year property often appear in assets that sit close to the line between personal property and building components. Electrical systems are a common example. General building electrical systems are usually tied to the operation or maintenance of the building, while certain dedicated electrical components may support qualifying § 1245 property. The analysis must show the relationship between the electrical component and the end-use asset.

Interior finishes can also create audit risk. Some wall coverings, decorative elements, and removable finishes may qualify in specific fact patterns, while permanent finishes attached with mortar, cement, grout, nails, screws, or permanent adhesives may be treated as building components. Similar issues can appear with specialty lighting, signage, security systems, appliances, plumbing connections, and tenant-specific improvements.

Residential rental properties have their own pressure points. Appliances may qualify as 5-year property, while cabinets, sinks, general plumbing, general kitchen electrical, and other structural components usually follow the building life. Commercial properties may involve more complex business-use systems, dedicated equipment, and industry-specific assets. In each case, investors need an asset-by-asset explanation rather than a broad allocation.

How to Prepare Before an IRS Cost Seg Review

The best audit defense is built before the IRS ever asks a question. Investors should start by keeping purchase documents, closing statements, construction invoices, improvement records, plans, photos, and placed-in-service support. For acquired properties, documentation should help explain how the purchase price was allocated among land, building, land improvements, and personal property. For renovations or new construction, actual cost records can be especially valuable.

A strong study should also avoid unsupported percentages. Reclassifying 5-year property based on generic estimates can create risk when the examiner asks how the number was developed. Better support includes takeoffs, cost detail, engineering judgment, photographs, invoice review, and reconciliation to total basis.

Investors should also coordinate with their CPA before filing. The study should fit the tax return position, depreciation schedules, bonus depreciation treatment, and any accounting method considerations. This is where planning matters. Knowing when to perform a cost segregation study can help investors align documentation, tax strategy, and filing deadlines before the study becomes part of an IRS review.

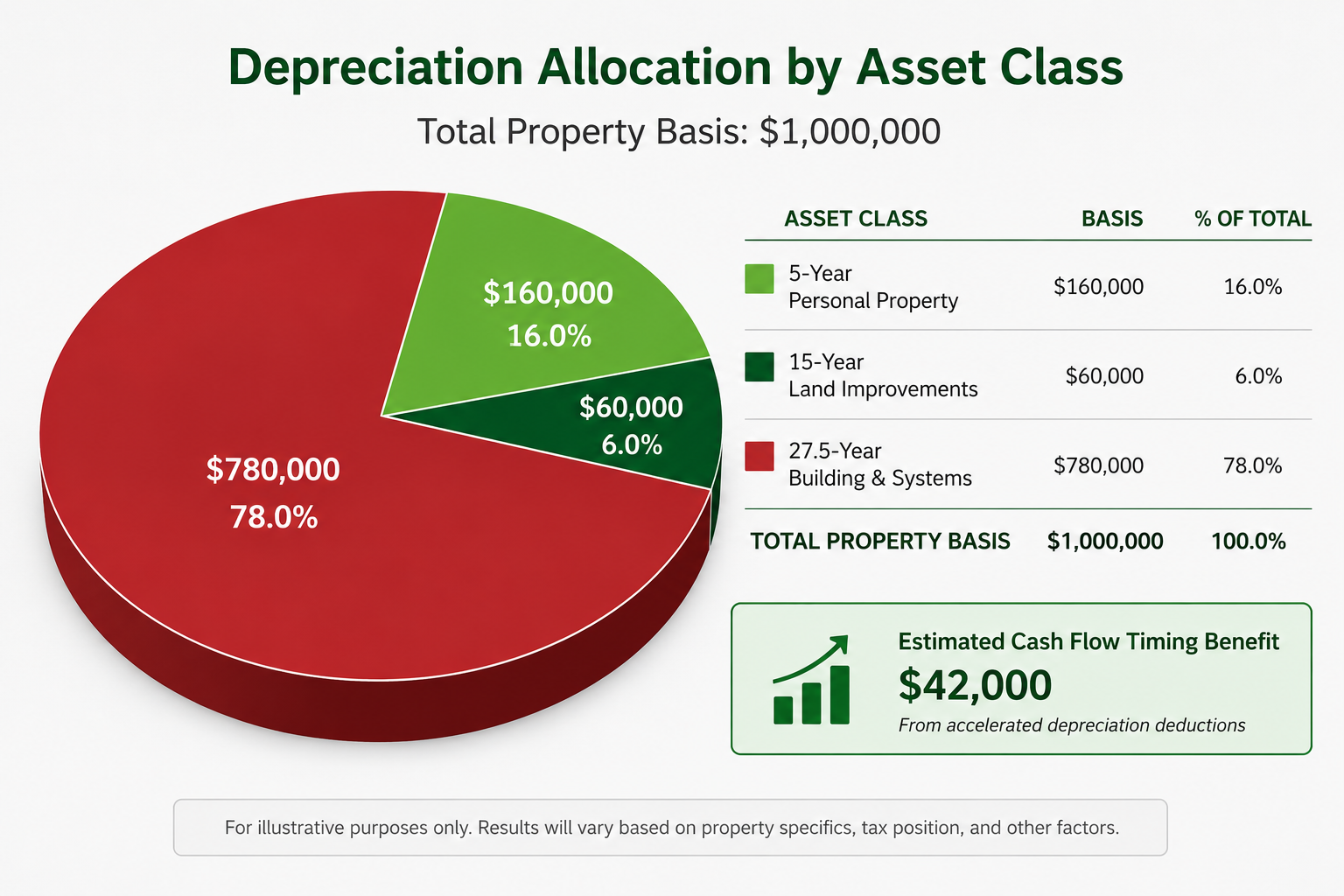

Audit Defense Example for a $1,000,000 Rental Property

Assume an investor purchases a residential rental property with a $1,000,000 depreciable building basis after land is removed. A cost segregation study identifies 22% of the basis, or $220,000, as shorter-life property and land improvements. Of that amount, $160,000 is supported as 5-year § 1245 property, while $60,000 is classified as 15-year land improvements. The remaining $780,000 stays in 27.5-year residential rental property.

The 5-year portion might include supported appliances, dedicated branch electrical for qualifying appliances, certain removable assets, and other tangible personal property. The 15-year portion might include qualifying land improvements. The building portion would include structural components such as walls, roof systems, general electrical, general plumbing, cabinets, and permanent building systems.

From a cash flow perspective, the $160,000 of 5-year property is the most powerful part of the study because it accelerates deductions into the early years. But in an audit, the investor must show why each item belongs in 5-year property. If the study simply lists a percentage without asset descriptions, cost logic, photos, or engineering support, the deduction is harder to defend. If the study ties each item to its function, cost source, recovery period, and § 1245 reasoning, the investor has a much stronger position.

Build Your Defense Before the IRS Asks

Defending 5-year property in an IRS cost segregation audit is not about being aggressive. It is about being specific, consistent, and well documented. The strongest studies connect tax law, engineering analysis, property facts, and cost data in a way that an examiner can follow.

Investors should expect 5-year classifications to receive attention because they can materially change depreciation timing. That attention is manageable when the study explains the asset, the use, the cost, and the recovery period. It becomes risky when the study relies on unsupported assumptions or pushes building components into short-life categories without a clear basis.

Cost segregation remains an established tax strategy, but the quality of the study matters. A defensible 5-year property position starts with engineering methodology, IRS-aligned classification logic, and documentation that is strong enough to support the deduction long after the return is filed.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.