Cost Segregation Audit Readiness for Quality Studies

Jul 02, 2026Stop sending more money to the IRS than you legally have to.

Many real estate investors overpay because they treat most of their property as 27.5-year residential rental property or 39-year nonresidential real property by default. Cost segregation helps identify assets that may qualify as 5-year property, 15-year land improvements, or QIP 15-year property, creating deductions that can improve cash flow.

The strategy is not a loophole. It is established tax treatment that works best when supported by engineering analysis and audit-ready documentation. That is where CostSegRx helps.

Most investors evaluate a cost segregation study based on projected tax savings. While cash flow benefits are important, audit readiness should be equally important when selecting a provider. A study that produces aggressive allocations without sufficient engineering support can create unnecessary risk if questions arise later.

The IRS Cost Segregation Audit Technique Guide places significant emphasis on methodology, documentation, asset classification, and reconciliation of costs. A quality study should be prepared with those standards in mind from the beginning. Investors who understand what makes a study defensible are better positioned to protect both current deductions and future tax positions.

Let us walk you through your property. Schedule a call today.

Key Takeaways

- Understand what separates a quality study from aggressive allocations

- Learn how engineering methodology supports asset classifications

- See why documentation matters during IRS examinations

- Review property types that benefit from audit-ready studies

- Explore planning steps that improve study defensibility

- See how weak studies can create costly problems later

- Focus on long-term compliance while maximizing depreciation benefits

What Is Cost Segregation Audit Readiness?

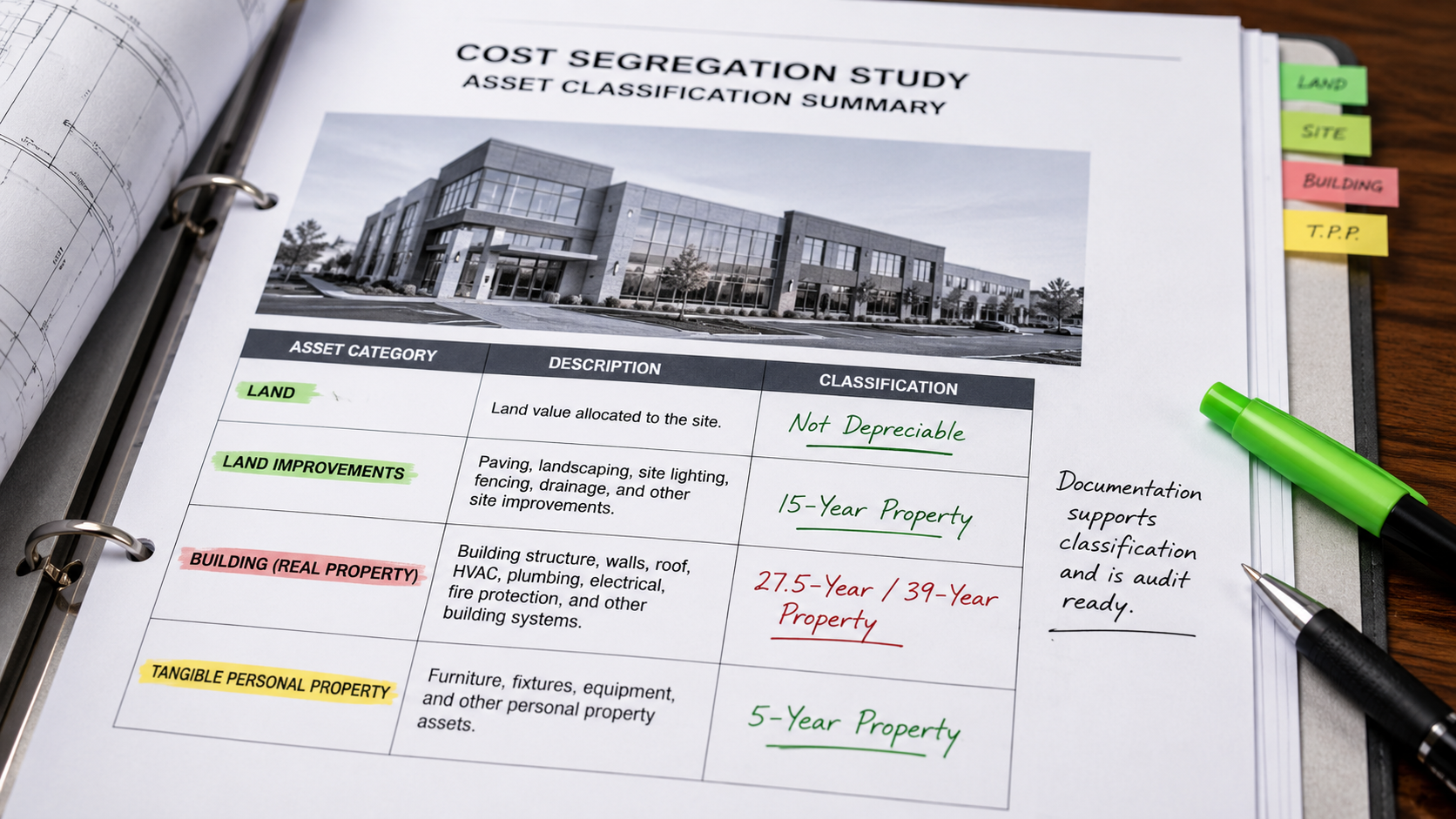

Cost segregation audit readiness refers to the ability of a study and supporting documentation to withstand IRS review. The IRS identifies cost segregation studies as analyses that allocate costs among land, land improvements, buildings, and tangible personal property when lump-sum project costs must be separated into individual asset classifications.

A quality study goes beyond generating accelerated depreciation deductions. It documents the reasoning behind each classification and provides support for the placement of assets into categories such as 5-year property, 15-year land improvements, QIP 15-year property, 27.5-year residential rental property, and 39-year nonresidential real property.

Investors seeking stronger compliance foundations often focus on what defines a quality cost segregation study before evaluating projected tax savings.

How Quality Studies Support Asset Classification

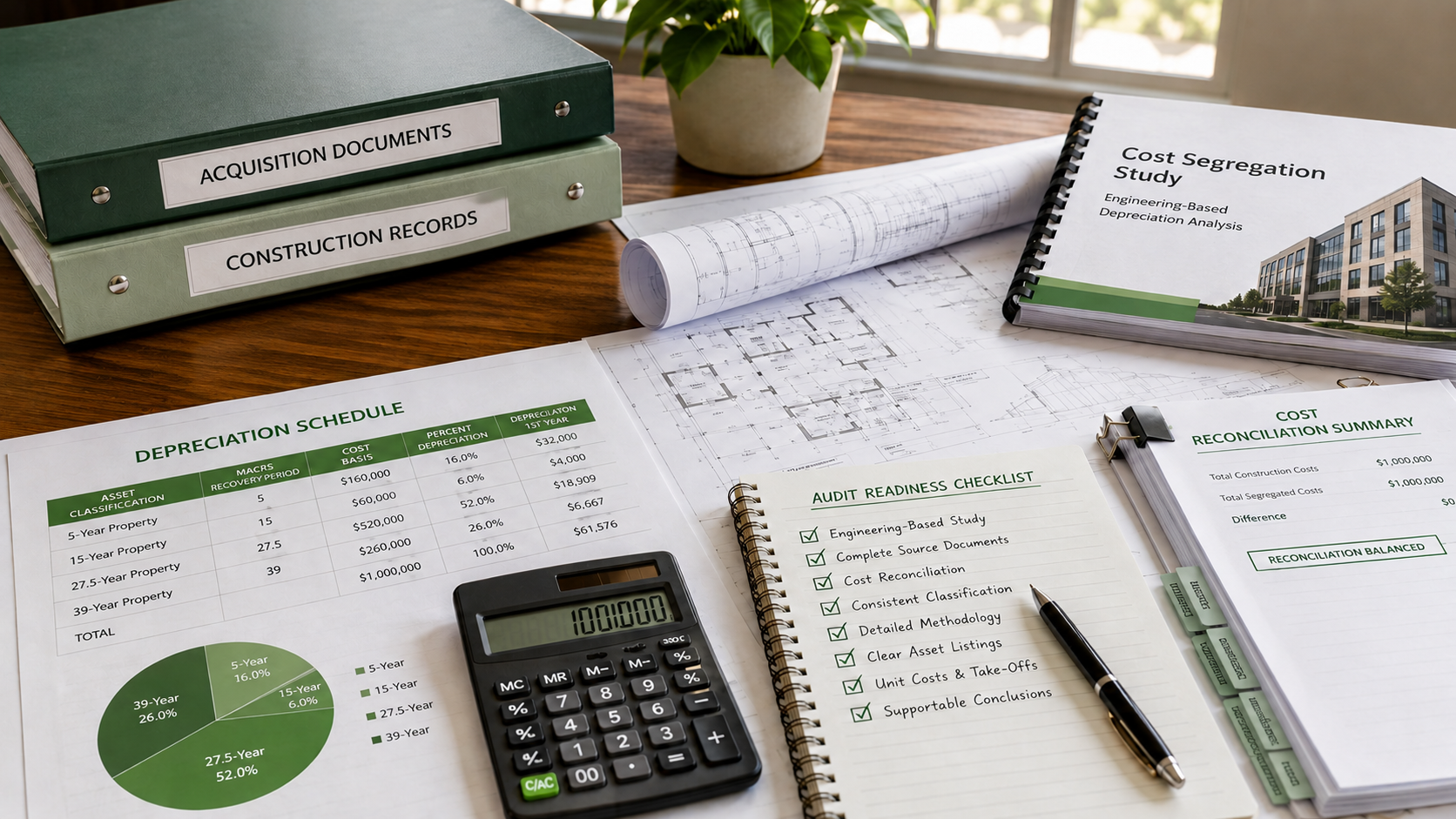

The IRS Audit Technique Guide discusses several approaches used in cost segregation studies and highlights detailed engineering approaches as the strongest methodologies when supported by appropriate documentation. Quality studies typically include engineering analysis, construction document review, cost reconciliation, and asset-level classification support.

For example, a study may identify 5-year property such as specialty equipment, removable finishes, and qualifying dedicated systems; 15-year land improvements such as parking areas, landscaping, sidewalks, and site improvements; QIP 15-year property for qualifying interior improvements to nonresidential real property; 27.5-year residential rental property; and 39-year nonresidential real property.

Asset classifications frequently depend on detailed engineering analysis. Topics such as electrical distribution systems in cost segregation studies often require functional allocation and supporting documentation rather than broad assumptions.

Why Audit Readiness Matters for Investors

A study that lacks supporting documentation may create challenges years after the original tax return is filed. Investors often assume the primary objective is maximizing accelerated depreciation, but preserving deductions during an examination is equally important.

The IRS specifically identifies documentation quality, methodology transparency, cost reconciliation, legal analysis, and asset support as important elements of a quality study.

Strong documentation can help investors support depreciation deductions, improve confidence during lender or investor reviews, reduce disputes regarding asset classifications, and maintain consistency across future acquisitions.

Understanding common cost segregation strategy mistakes can help investors avoid preventable compliance issues.

Applications Across Property Types

Audit-ready studies can benefit a wide range of property owners, including multifamily investors, self-storage owners, retail centers, medical offices, industrial facilities, mobile home parks, and hospitality properties.

Each property type presents unique asset classification opportunities and documentation requirements. For example, investors in properties with substantial site improvements often benefit from understanding how land improvement heavy cost segregation can affect depreciation allocations.

The key principle remains consistent regardless of property type: classifications should be supported by facts, engineering analysis, and applicable tax authority.

Audit Readiness Strategy for Property Owners

Audit readiness begins long before a tax return is filed.

Investors should prioritize engineering-based studies rather than percentage estimates, comprehensive construction and acquisition documentation, asset-level support where appropriate, cost reconciliation to total project costs, and consistent classification methodology.

Timing also matters. Conducting a study while project records remain accessible can improve documentation quality. Investors evaluating acquisition timing often benefit from understanding when to perform a cost segregation study as part of their overall tax planning process.

Financial Example

Assume a multifamily investor purchases a property for $5,000,000.

Purchase Price: $5,000,000

Land Allocation (20%): $1,000,000

Depreciable Basis: $4,000,000

Two cost segregation providers deliver studies on the same property.

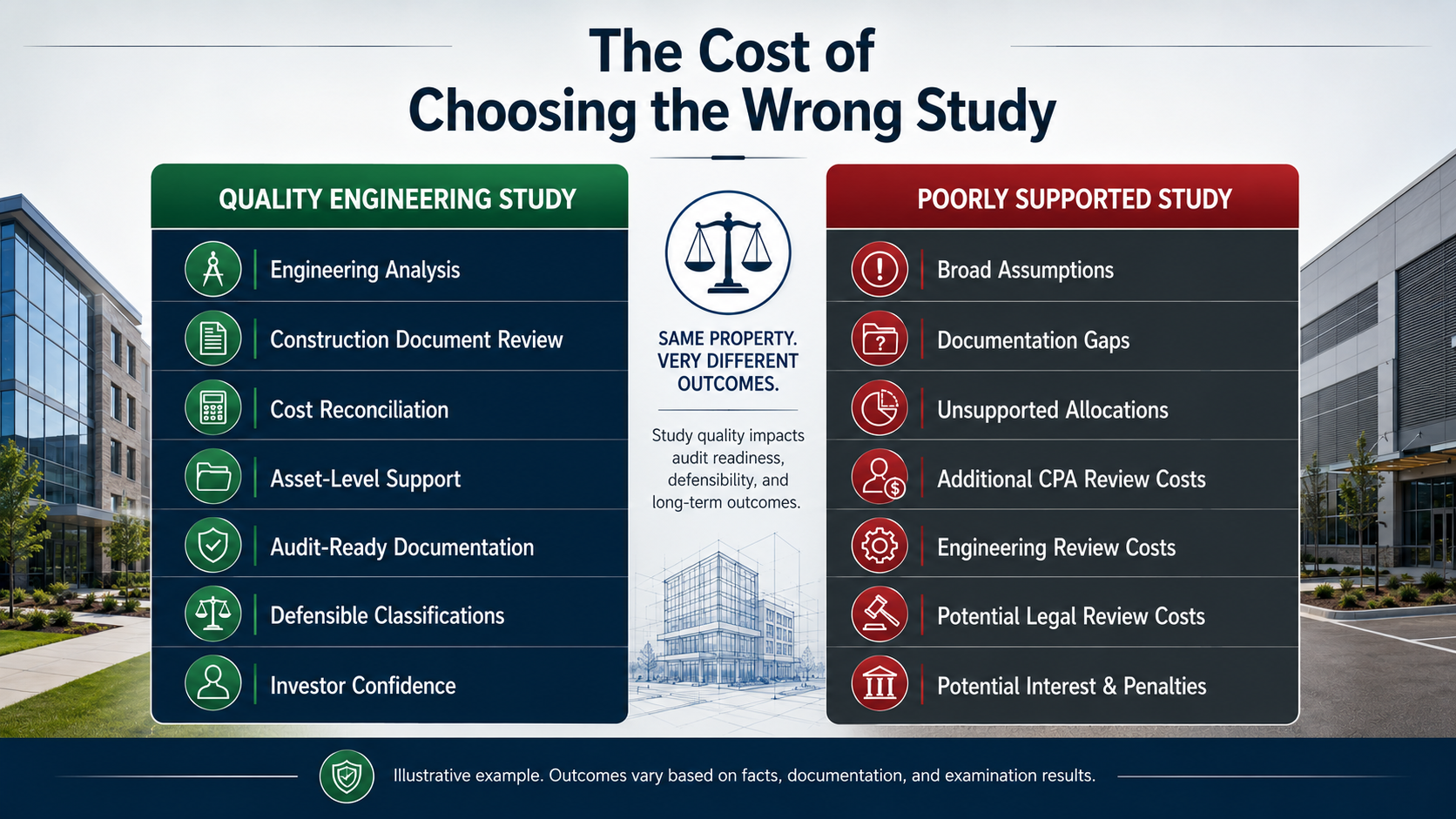

Study A includes engineering analysis, construction document review, cost reconciliation, asset-level support, and detailed documentation designed to support classifications years after the original tax return is filed.

Study B relies on broad assumptions, limited documentation, and weak support for asset classifications.

Several years later, the property is refinanced, sold, or becomes subject to a broader tax review. The investor who relied on Study B discovers that portions of the report cannot be adequately supported. Additional documentation requests follow, requiring significant time, professional review, and additional expense.

While every situation is different, poorly supported studies can create risks that extend far beyond the original tax return. Investors may face additional CPA review costs, engineering review costs, potential legal review costs, increased scrutiny of asset classifications, and potential interest or penalties depending on the facts and circumstances.

The purpose of a quality cost segregation study is not simply to generate larger deductions. The purpose is to generate deductions that can be supported years later through a documented engineering methodology and defensible asset classification process.

Building Confidence Through Quality Documentation

The strongest cost segregation studies are designed to balance tax efficiency with documentation quality. The IRS Audit Technique Guide repeatedly emphasizes methodology, supporting records, engineering analysis, and asset classification support as important characteristics of a quality study.

For investors, audit readiness is not about being conservative or aggressive. It is about ensuring that accelerated depreciation deductions are supported by a well-documented engineering process, appropriate asset classifications, and established tax treatment principles. When those elements work together, a cost segregation study can provide both tax benefits and long-term confidence.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.