Cost Segregation Strategy Mistakes That Reduce Investor ROI

Apr 28, 2026Cost segregation is one of the most powerful tax strategies available to real estate investors, but its effectiveness depends entirely on execution. When applied correctly, it accelerates depreciation, improves near-term cash flow, and enhances overall returns. When applied incorrectly, it can create compliance issues, reduce tax efficiency, and even trigger costly adjustments during an audit.

Many investors assume that simply completing a study guarantees optimal results. In reality, strategy, timing, methodology, and documentation all influence outcomes. Small decisions at each stage can materially impact the financial performance of a property.

Understanding where cost segregation strategies commonly fail allows investors to avoid unnecessary risk and capture the full economic benefit. The following mistakes are among the most frequent and most costly.

Key Takeaways

- Misclassifying assets can distort depreciation and increase audit exposure

- Overestimating short-life property may inflate deductions but reduce defensibility

- Poor study timing limits the ability to maximize accelerated depreciation

- Inadequate documentation weakens the support behind allocations

- Relying on low-quality methodologies reduces accuracy and ROI

- Ignoring interaction with bonus depreciation leads to suboptimal results

- Failing to align strategy with investment goals reduces long-term value

- Treating all properties the same ignores asset-specific opportunities

What Is Cost Segregation Strategy

Cost segregation strategy extends beyond the study itself. It is the process of aligning asset classification, depreciation timing, and tax elections with broader investment objectives.

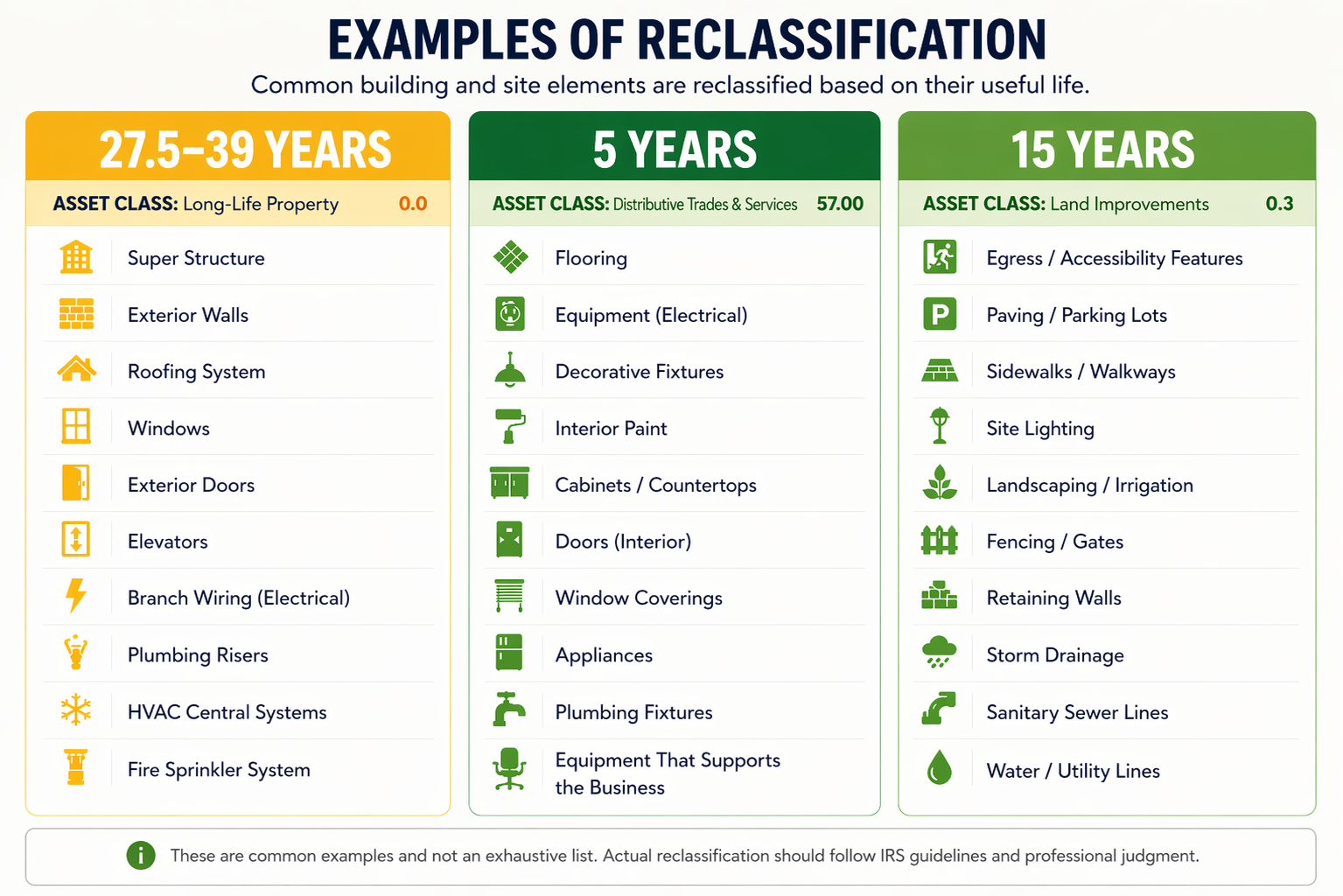

At its core, cost segregation reallocates portions of a property from long-life assets such as buildings into shorter-life categories like 5-year property and 15-year property, allowing accelerated depreciation. This reclassification creates earlier tax deductions, which improve after-tax cash flow.

However, the strategy component determines when the study is performed, how aggressively assets are classified, and how depreciation is integrated with other tax positions. Without a strategic framework, investors often leave value on the table or introduce unnecessary risk.

A disciplined approach ensures that cost segregation supports both short-term liquidity and long-term portfolio performance.

How Cost Segregation Works

Cost segregation works by breaking down a property into individual components and assigning each component to the appropriate tax classification. These classifications determine recovery periods and depreciation methods under the tax code.

Buildings are generally depreciated over long periods, while certain components qualify as tangible personal property with significantly shorter recovery lives. The incentive for investors is clear: shorter recovery periods produce larger deductions earlier in the ownership cycle.

A properly executed study identifies qualifying assets, assigns accurate costs, and reconciles totals to the overall project basis. The methodology used plays a critical role in accuracy. Engineering-based approaches relying on actual cost records or detailed estimates tend to produce the most defensible results, while simplified methods often sacrifice precision.

This technical foundation is where many strategic mistakes originate.

Why It Matters

Cost segregation directly impacts investor cash flow, tax liability, and internal rate of return. Accelerated depreciation can significantly reduce taxable income in early years, allowing capital to be reinvested into additional opportunities.

However, poorly executed strategies can reverse these benefits. Misclassification of assets may lead to disallowed deductions, while aggressive assumptions can increase audit scrutiny. Inconsistent methodologies can also distort financial projections, making investment performance appear stronger than it actually is.

Understanding cost segregation ROI requires more than measuring tax savings. It requires evaluating sustainability, compliance, and alignment with long-term goals.

Investors who treat cost segregation as a one-time tactic often miss its strategic implications across the lifecycle of an asset.

Applications in Real Estate Investing

Cost segregation is widely applied across property types, including multifamily, retail, industrial, and short-term rentals. Each asset class presents unique opportunities and risks.

For example, renovation-heavy projects require coordination with rules surrounding Qualified Improvement Property, where interior improvements may qualify for accelerated treatment. Misalignment in these scenarios can lead to incorrect classifications or missed deductions.

Similarly, investors acquiring stabilized assets must rely more heavily on estimation techniques, increasing the importance of methodology and documentation. In contrast, new construction projects benefit from detailed cost records, enabling more precise allocations.

The variability across property types reinforces the need for a tailored strategy rather than a standardized approach.

Strategy Mistakes That Reduce ROI

Several recurring mistakes undermine the effectiveness of cost segregation strategies. Each one introduces either inefficiency or risk, both of which reduce investor returns.

One of the most common issues is overestimating short-life assets. Inflating allocations to personal property may increase immediate deductions, but it weakens the defensibility of the study. The risks of overestimating short-life assets include potential reclassification during audits, which can reverse tax benefits and create penalties.

Another frequent mistake is poor timing. Investors who delay studies often miss the opportunity to align depreciation with peak income years. Understanding when to perform a cost segregation study is critical to maximizing impact, especially when combined with bonus depreciation.

Methodology is another major factor. Studies based on rule-of-thumb percentages or limited data tend to produce inconsistent results. In contrast, detailed engineering approaches provide stronger support and more accurate allocations, reducing both risk and uncertainty.

Finally, many investors fail to integrate cost segregation into a broader tax strategy. Ignoring interactions with depreciation elections, renovation rules, or portfolio-level planning can limit overall effectiveness.

Financial Impact of Strategic Errors

Consider a $5 million commercial property where 25 percent of costs are allocated to short-life assets. If the allocation is overstated by even 5 percent due to aggressive assumptions, the investor may claim excessive depreciation in early years.

While this may temporarily increase cash flow, it creates exposure to adjustment if the classification cannot be substantiated. Reversal of those deductions, combined with potential penalties, can significantly reduce net returns.

Conversely, under-allocating short-life assets due to conservative or incomplete analysis results in missed tax savings. In this case, the investor sacrifices immediate liquidity that could have been reinvested elsewhere.

Both scenarios highlight the importance of precision. Accurate classification is not just a compliance issue, it is a direct driver of financial performance.

![]()

Building a Defensible and Profitable Strategy

A high-performing cost segregation strategy balances acceleration with accuracy. It relies on detailed analysis, proper documentation, and alignment with broader investment goals.

This includes selecting the right methodology, validating asset classifications, and ensuring that all allocations are supported by credible data. It also requires coordination with tax planning strategies such as bonus depreciation, renovation treatment, and portfolio-level decisions.

Investors who approach cost segregation with discipline gain more than tax savings. They gain clarity, consistency, and confidence in their financial projections.

Closing Perspective on Maximizing Cost Segregation Value

Cost segregation is not inherently beneficial or risky. Its impact depends entirely on how it is executed. Strategic mistakes can quietly erode returns, while disciplined implementation can materially enhance them.

The difference lies in understanding the details, applying the right methodology, and integrating the study into a broader investment framework. Investors who recognize these factors position themselves to capture the full economic value of accelerated depreciation without compromising compliance or long-term performance.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.