Self-Storage Cost Segregation for Faster Depreciation and Cash Flow

Jun 04, 2026Self-storage properties can look simple from the outside, but their tax treatment is often more layered than investors expect. A facility may include rental buildings, paving, fencing, gates, security systems, signage, exterior lighting, office buildouts, drainage, and site improvements. Without a cost segregation study, many of those costs may stay locked inside long-life real property. With the right engineering-based approach, self-storage investors can often accelerate depreciation and improve early-year cash flow.

Let us walk you through your property. Schedule a call today.

Key Takeaways

- Self-storage facilities often contain multiple shorter-life asset categories.

- Engineering analysis separates building costs from qualifying personal property.

- Faster depreciation can improve early cash flow after acquisition.

- Self-storage, climate-controlled, and mixed-use facilities may benefit.

- Timing the study early can strengthen tax planning decisions.

- A basis-based example shows how deductions may shift forward.

- A defensible study should align tax treatment with engineering facts.

Why Self-Storage Facilities Need Asset-Level Depreciation Review

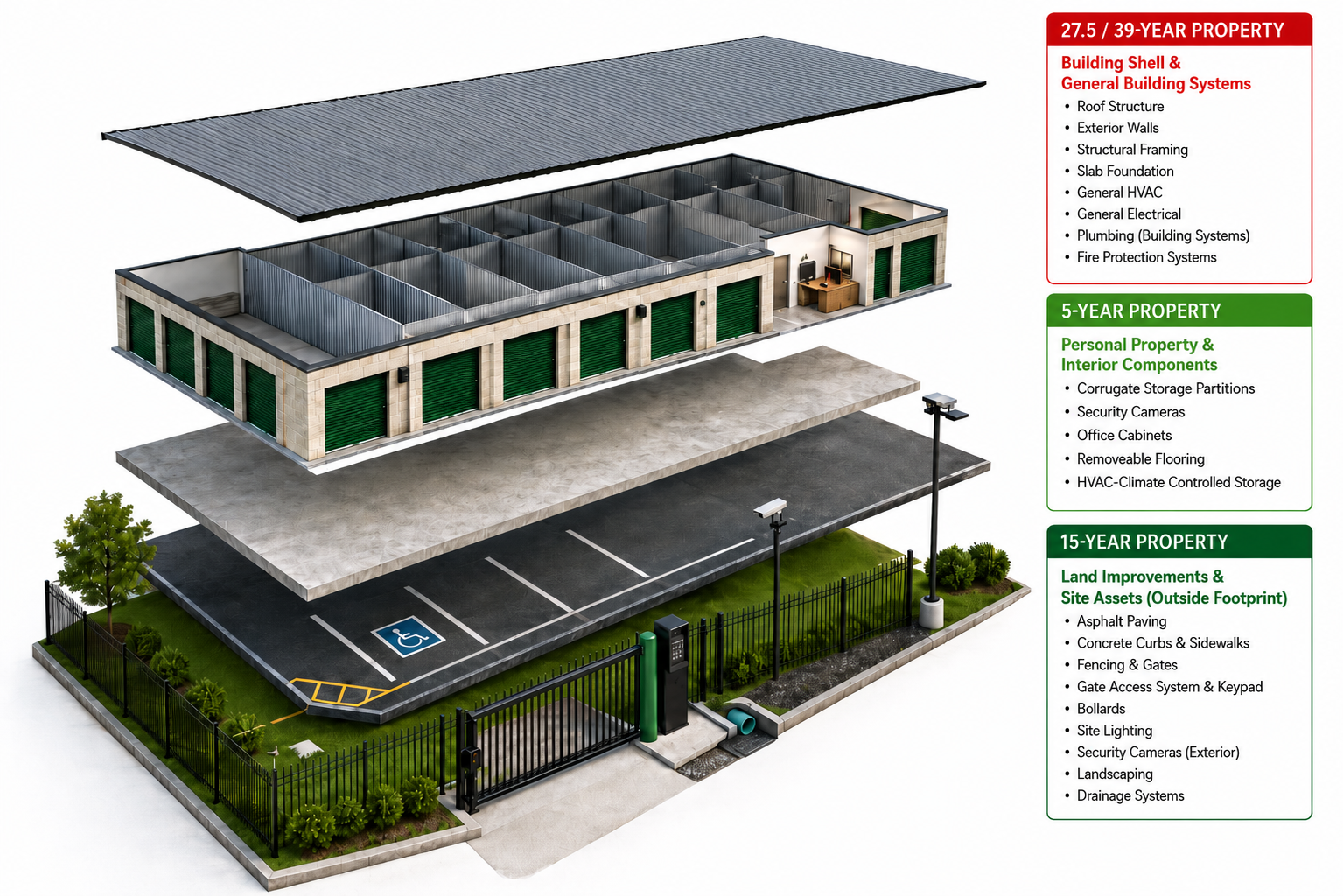

Self-storage cost segregation is the process of breaking a facility into the assets that make up the property and assigning each item to its proper tax recovery period. Instead of treating the entire facility as 39-year nonresidential real property, a study evaluates whether certain assets qualify for shorter recovery periods.

The tax logic comes from the distinction between real property and tangible personal property. A building and its structural components generally fall into longer-life real property. Certain equipment, removable finishes, dedicated systems, and property used for a specific business function may qualify as shorter-life property when the facts support that treatment.

Self-storage properties are especially important because the site often includes more than just storage buildings. Fencing, asphalt, concrete drives, lighting, gates, drainage, signage, access controls, office finishes, and security components may each need separate review. Some items may be 5-year property, some may be 15-year land improvements, and some will remain 39-year real property.

The IRS Cost Segregation Audit Technique Guide focuses heavily on methodology, documentation, asset classification, and the difference between §1245 and §1250 property. That means a good study is not just a tax estimate. It should connect engineering observations, cost data, and legal classification in a way that supports the depreciation position.

How Engineers Separate Storage Facility Components

A self-storage study usually starts with the purchase price or construction cost, then removes the land allocation because land is not depreciable. The remaining depreciable basis is analyzed using plans, site data, photos, contractor cost records, invoices, and engineering estimates.

The engineering team then identifies assets and groups them by tax class. A storage building’s structural shell, roof, walls, and general building systems usually remain long-life real property. But certain assets may be separated when they serve a qualifying function or are not structural components.

For example, site paving and fencing may often be evaluated as 15-year land improvements. Security cameras, gate access systems, certain office equipment, removable floor coverings, and dedicated electrical components may require separate analysis for potential shorter-life treatment. The correct answer depends on how the asset is installed, what it serves, and whether it relates to the operation or maintenance of the building.

This is where engineering substance matters. A strong study should use itemized cost records when available, or detailed engineering cost estimates when actual cost detail is limited. Investors comparing cost segregation vs straight-line depreciation should focus on the timing difference. Cost segregation does not create fake deductions. It changes when legitimate depreciation deductions are recognized.

Why Faster Depreciation Can Improve Self-Storage Returns

Self-storage investing is often driven by occupancy growth, revenue management, operating efficiency, and refinance timing. Depreciation strategy can affect each of those decisions because tax savings can improve after-tax cash flow during the years when capital is most valuable.

After acquisition, many investors spend heavily on repairs, signage, unit upgrades, security, office improvements, paving, or expansion. Accelerated depreciation may help offset taxable income and keep more cash available for improvements, reserves, or investor distributions.

The impact can be especially meaningful when the investor has taxable income that can use the deductions. Passive activity limitations, ownership structure, at-risk rules, and bonus depreciation rules all matter, so the study should be coordinated with a CPA or tax advisor.

Cost segregation can also improve planning before a refinance or sale. If early-year deductions create stronger cash flow, the investor may have more flexibility to reinvest in the property, manage debt service, or support a value-add plan. For a broader investor overview, see how cost segregation can reduce taxes and increase cash flow across real estate assets.

Where Self-Storage Investors Often Find Reclassification Opportunities

Not every self-storage property produces the same result. A basic drive-up facility with limited site improvements may have a different reclassification profile than a climate-controlled facility with offices, advanced access systems, elevators, security infrastructure, and extensive paved areas.

Drive-up facilities often include large amounts of paving, drainage, fencing, gates, exterior lighting, and signage. These assets can be important because land improvements may qualify for shorter recovery periods than the main building.

Climate-controlled facilities may include more interior systems, office space, corridors, security systems, and specialized electrical or HVAC considerations. Some systems will remain structural because they support the general building. Others may need deeper review if they serve specific equipment or business functions.

Mixed-use storage properties can add another layer. A facility may include a manager’s office, retail packing supply area, truck rental counter, vehicle storage, RV parking, or warehouse-style units. Each use can affect asset classification and cost allocation. This is why generic percentages can be risky. A study should match the actual property, not a shortcut template.

When to Order a Study for a Self-Storage Acquisition

The best time to evaluate self-storage cost segregation is usually soon after acquisition, construction, or major renovation. Early timing gives the investor and CPA more planning room before the return is filed.

For an acquisition, the study should start with the purchase price allocation. Land is separated first, then the depreciable basis is assigned across buildings, land improvements, and personal property. For new construction, contractor invoices, pay applications, plans, and change orders can make the study more precise.

For renovations, timing matters because removed assets, new improvements, repairs, and capitalized work may all need different treatment. A cost segregation review can help identify which assets are newly placed in service and which costs should be classified separately. Investors planning improvements should review commercial renovation tax planning before major work begins.

Bonus depreciation may also be part of the strategy if qualified assets are eligible under the rules in effect for the placed-in-service year. The study must identify the asset class first. Bonus depreciation is applied only after the property is properly classified.

Example: Self-Storage Facility Depreciation Shift

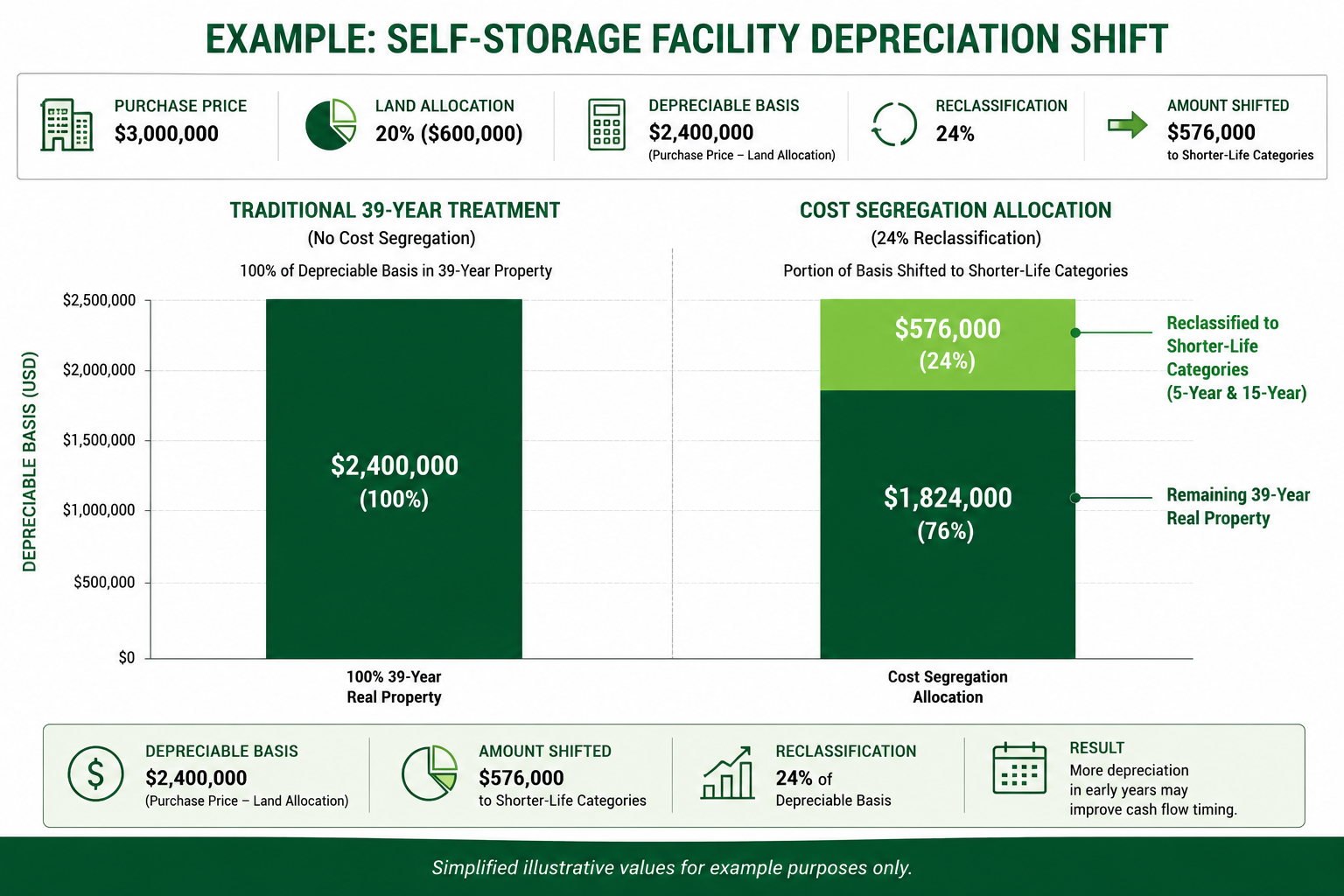

Assume an investor purchases a self-storage facility for $3,000,000. The land allocation is 20%, or $600,000. That leaves a depreciable basis of $2,400,000.

If the property is depreciated entirely as 39-year nonresidential real property, the first-year depreciation may be relatively limited. A cost segregation study reviews the depreciable basis and identifies assets that may qualify for shorter recovery periods.

For this example, assume the study supports 24% reclassification of depreciable basis into shorter-life categories. That equals $576,000 of assets moved out of 39-year treatment. A typical allocation may include a larger 5-year property category and a smaller 15-year land improvement category, depending on the actual asset mix.

Illustrative allocation:

Purchase price: $3,000,000

Land allocation: $600,000

Depreciable basis: $2,400,000

Reclassified assets at 24%: $576,000

Remaining 39-year real property: $1,824,000

If most of the reclassified amount is 5-year property, the investor may receive substantially more depreciation in the early years than straight-line treatment would provide. If eligible bonus depreciation applies, the timing benefit may increase further.

This example is simplified and should not be treated as a fixed savings estimate. The actual result depends on the facility design, site improvements, cost records, asset support, placed-in-service date, tax rate, passive activity status, and applicable bonus depreciation rules. For planning around accelerated deductions, review bonus depreciation and cost segregation with your tax advisor.

Build the Tax Strategy Around the Engineering Facts

Self-storage cost segregation works best when the study is grounded in engineering detail, IRS-aligned classification, and established tax treatment. The goal is not to force aggressive percentages. The goal is to identify the assets that are already present and depreciate them under the correct recovery periods.

A defensible study should document the property, explain the methodology, classify assets consistently, reconcile costs, and support the distinction between §1245 and §1250 property. That gives investors a stronger tax position and a clearer view of after-tax cash flow.

For self-storage owners, the opportunity can be practical and measurable. If you recently acquired, built, expanded, or renovated a facility, cost segregation may help move valid deductions into the years when cash flow matters most.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.