How to Properly Perform Cost Segregation on New Construction Projects

Jul 09, 2026New construction projects often appear to be the easiest properties for cost segregation. After all, the project is brand new, construction records exist, and contractors have already tracked costs throughout the build. However, many investors and advisors discover that the records provided at project completion are not detailed enough to support accurate asset classification. In many cases, the most commonly available documents were created for construction payment purposes, not tax depreciation analysis.

This distinction matters because a quality cost segregation study depends on understanding what was built, where it was installed, and how individual assets function within the property. Without that level of detail, important assets may remain buried inside broad construction categories, resulting in less accurate depreciation allocations and weaker documentation.

Key Takeaways

- Understand why new construction cost segregation requires engineering analysis

- Learn why G702 forms rarely provide sufficient asset detail

- See how better classifications improve depreciation accuracy

- Review common project types where detailed analysis matters

- Identify the records needed for a defensible study

- See how construction documentation affects 5-year property support

- Understand what defines a quality new construction study

Why New Construction Cost Segregation Requires More Than Construction Accounting

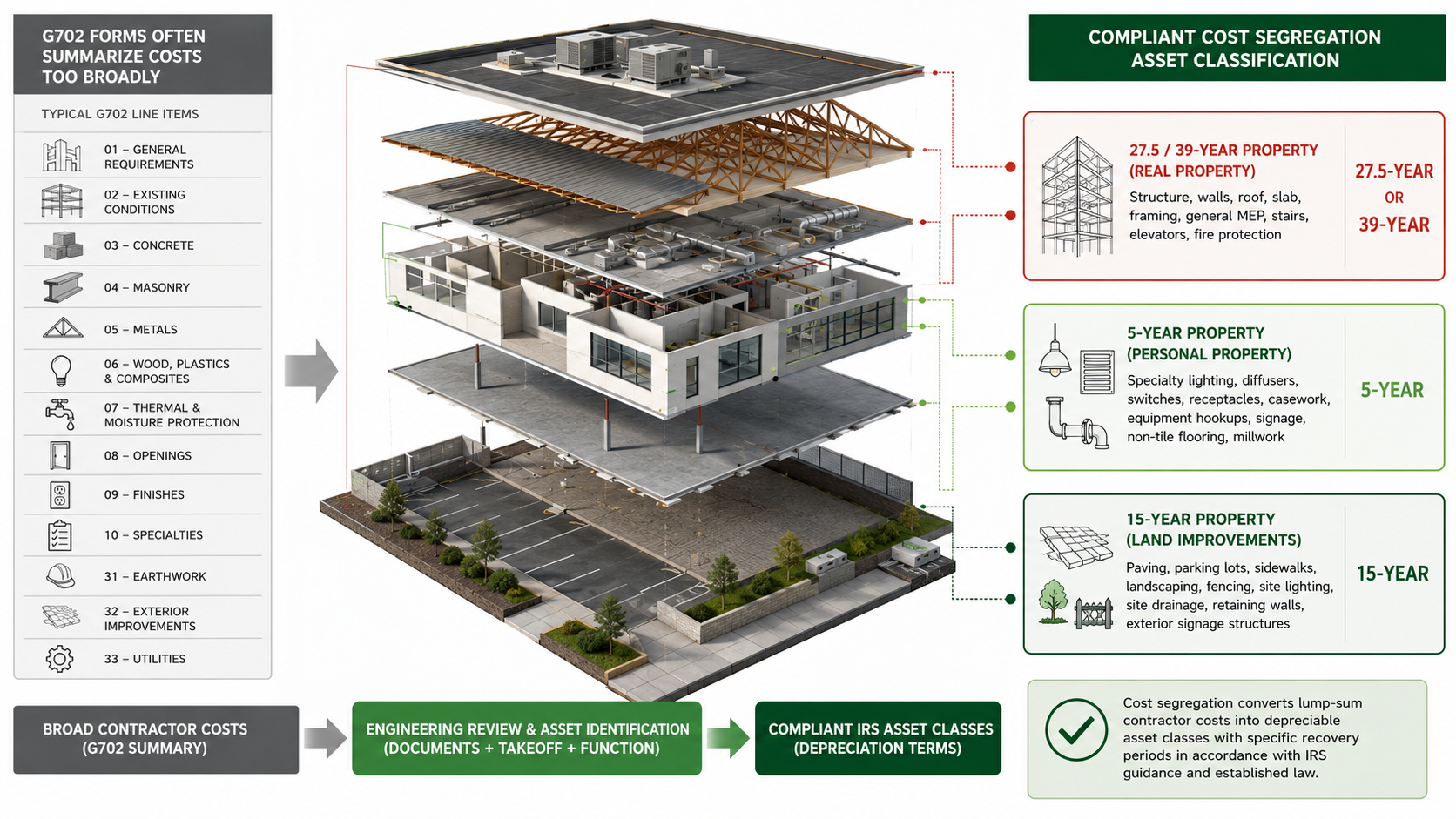

A new construction cost segregation study identifies assets that qualify for treatment as 5-year property, 15-year land improvements, QIP 15-year property when applicable, 27.5-year residential rental property, or 39-year nonresidential real property. While the construction process creates substantial documentation, much of that information was developed for budgeting, payment approvals, and project management rather than tax classification.

The IRS Cost Segregation Audit Technique Guide emphasizes the importance of documentation, engineering analysis, cost reconciliation, legal analysis, and proper asset identification in a quality study. Simply knowing how much was spent on electrical work, plumbing work, or finishes is often not enough. The study must determine which portions of those systems support qualifying assets and which portions remain part of the building. The ATG discusses the importance of identifying §1245 property separately from §1250 property and documenting the methodology used to support those classifications.

This distinction is particularly important when evaluating systems that may partially support qualifying assets. For example, articles discussing electrical distribution systems in cost segregation studies demonstrate how engineering analysis may be required to properly allocate portions of a system to supported classifications.

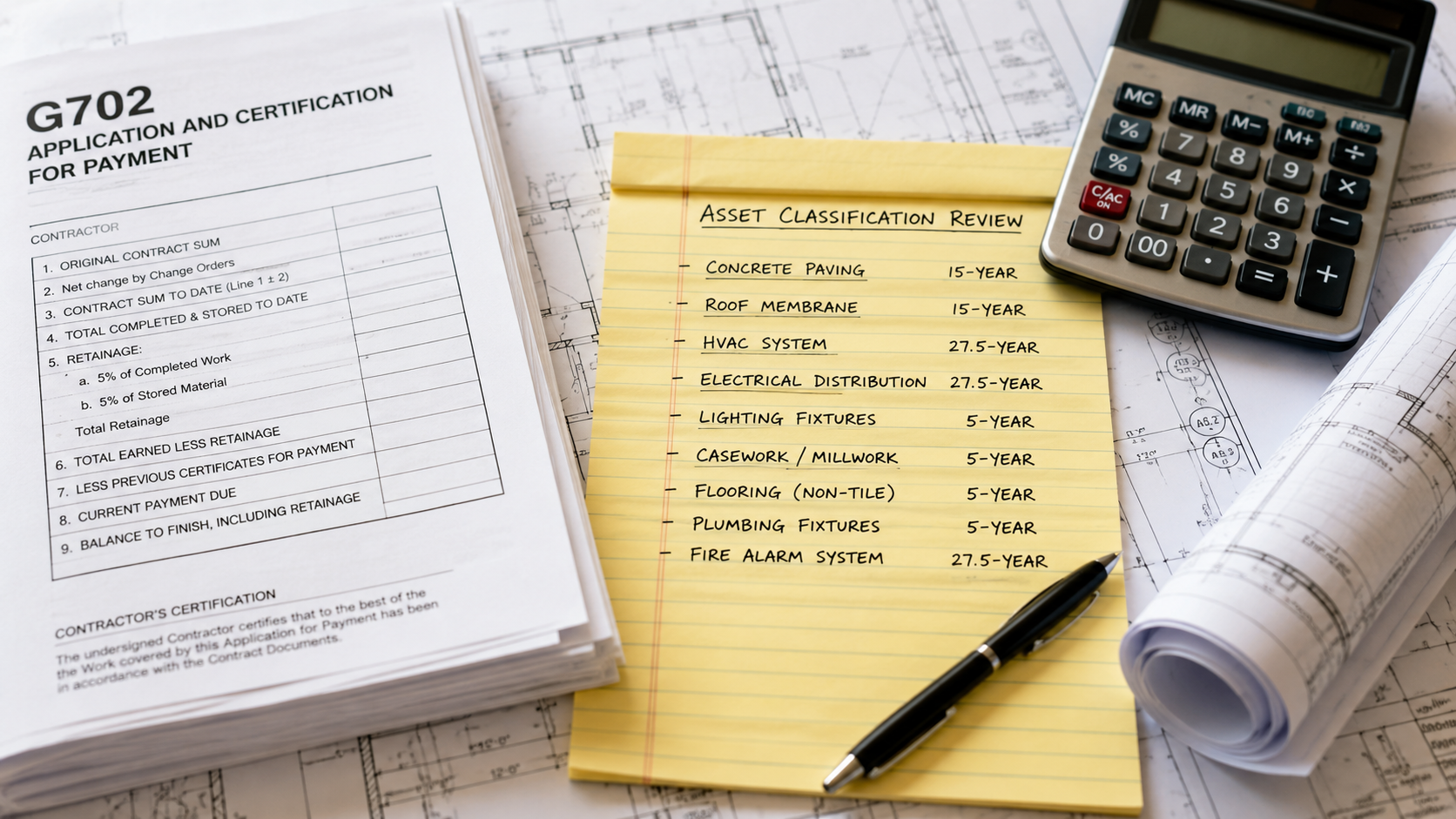

Why G702 Forms Rarely Tell the Full Story

Many developers receive an AIA G702 application and certificate for payment as one of the primary project cost summaries. These forms serve an important purpose during construction by documenting payment requests, completed work, retainage, and project progress. However, they typically summarize costs into broad divisions and do not identify individual depreciable assets.

For example, a G702 may show a lump-sum electrical amount, but it generally does not separate dedicated electrical systems supporting qualifying equipment from building electrical infrastructure that remains part of 39-year nonresidential real property or 27.5-year residential rental property. The same challenge often appears with plumbing, specialty finishes, millwork, concrete work, and site improvements.

A quality engineering-based study frequently requires additional information such as construction drawings, specifications, subcontractor schedules, equipment schedules, approved submittals, site photographs, contractor cost breakdowns, and owner interviews. This approach aligns more closely with the principles discussed in what makes a quality cost segregation study defensible than relying solely on summary-level construction accounting.

Why Detailed Classification Matters for Investors

The goal of cost segregation is not simply to accelerate depreciation. The goal is to accurately classify assets according to established tax treatment. When construction costs are grouped too broadly, qualifying assets may remain embedded within building costs and continue depreciating over 27.5 years or 39 years.

Accurate classification can affect investor cash flow, project underwriting, tax planning, and long-term return calculations. It can also improve the quality of documentation available if questions arise during a future review.

This is particularly important because construction projects often contain a significant mix of asset types. Dedicated systems, specialty finishes, site improvements, and certain equipment support infrastructure may require different treatment than general building components. Investors evaluating the potential benefits of cost segregation benefits should understand that the quality of the classification process often matters as much as the final percentages.

Where This Issue Appears Most Often

The challenge is not limited to one property type. New construction cost segregation studies commonly involve multifamily developments, medical offices, industrial facilities, self-storage projects, retail centers, hospitality properties, and specialized commercial buildings.

Medical and dental facilities frequently include dedicated infrastructure supporting equipment and specialized operations. Industrial facilities may contain process-related systems that require detailed evaluation. Self-storage developments often include significant site improvements that may qualify as 15-year land improvements. Large multifamily projects frequently contain extensive site development, amenity areas, and supporting infrastructure.

Projects delivered through design-build methods can create additional challenges because cost records are often consolidated into broader reporting categories. This is one reason many developers explore design-build cost segregation planning before project completion.

The Records That Support a Defensible New Construction Study

The strongest new construction studies combine engineering review with comprehensive project documentation. Rather than relying solely on payment applications, the study team evaluates multiple sources of information to identify and classify assets.

Important records often include:

- Architectural and engineering plans

- Construction specifications

- Subcontractor schedules of values

- Equipment schedules

- Owner-provided project information

- Site inspection data

- Photographic documentation

- Cost reconciliation records

The IRS ATG identifies detailed engineering approaches, cost reconciliation, asset schedules, legal analysis, and supporting documentation as important characteristics of a quality study. Unsupported percentages and rule-of-thumb allocations generally provide weaker support than engineering-based methodologies.

Financial Example: The Same Building With Two Different Outcomes

Assume two developers each complete an identical medical office building with a total project cost of $10,000,000. Land is allocated at an estimated 20%, or $2,000,000. Each project has the same $8,000,000 depreciable basis.

The buildings are virtually identical. The construction methods, materials, and completed facilities are the same. The difference is how construction information was preserved during the project.

Scenario A: The Typical Closeout Package

Developer A does not consider cost segregation until after construction is complete. The records available for the study include G702 payment applications, broad subcontractor totals, lump-sum electrical costs, lump-sum plumbing costs, and general contractor closeout documentation.

The engineering team can still perform a cost segregation study, but many potential 5-year property assets are embedded within larger building categories. Without supporting detail, those costs generally remain classified as 39-year nonresidential real property.

The issue is not that qualifying assets do not exist. The issue is that the documentation needed to support separate classifications may no longer be available.

Scenario B: Cost Segregation Planning During Construction

Developer B discusses cost segregation while the project is being built. The goal is not to track every screw, nail, wire, or pipe. Instead, the project team preserves information for assets most likely to affect classification.

Examples include dedicated electrical systems, specialty plumbing, equipment support infrastructure, millwork categories, decorative finishes, specialty flooring, and site improvements. These records can often be captured through subcontractor schedules, equipment schedules, construction drawings, specifications, and targeted documentation requests during the project.

Because the supporting information exists, the engineering team can identify and support additional qualifying assets when the study is performed.

The Key Lesson

The building did not change.

The depreciable basis did not change.

The construction cost did not change.

The documentation changed.

For many new construction projects, the biggest opportunity is not performing the study after completion. The biggest opportunity is preserving the information needed to support asset classifications while construction is still underway. When important details disappear into broad contractor reporting categories, potential 5-year property classifications may become more difficult to identify and support later.

What Defines a Quality New Construction Cost Segregation Study

New construction projects provide an enormous amount of information, but not all construction records were designed for tax depreciation analysis. Payment applications, G702 summaries, and broad cost categories help manage construction projects, but they rarely provide enough detail to support complete asset classification on their own.

A quality study combines engineering analysis, project documentation, cost reconciliation, and established tax treatment to identify assets accurately. By evaluating plans, specifications, schedules, site data, and supporting records, the study can distinguish qualifying 5-year property, 15-year land improvements, QIP 15-year property when applicable, 27.5-year residential rental property, and 39-year nonresidential real property based on the facts of the project.

The result is not simply accelerated depreciation. The result is a more accurate and defensible classification of construction costs that aligns with engineering support and established tax treatment.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.