Depreciation Recapture After Cost Segregation Explained

Jul 07, 2026Cost segregation can improve cash flow by moving eligible building-related costs into 5-year property, 15-year land improvements, and QIP 15-year property when the facts support it. That upfront depreciation benefit is valuable, but investors also need to understand what happens when the property is sold. Depreciation recapture does not usually erase the value of cost segregation, but it can affect after-tax sale proceeds. The key is planning for both the hold period and the exit before the property goes under contract.

Let us walk you through your property. Schedule a call today.

Key Takeaways

- Understand how recapture changes after a cost segregation study

- Separate §1245 and §1250 treatment before selling property

- Plan sale proceeds around cash flow and tax timing

- Apply recapture planning across common investment property types

- Coordinate cost segregation, hold period, and exit strategy

- See how depreciation taken affects recapture exposure

- Use engineering support to avoid weak asset classifications

What Depreciation Recapture Means After Cost Segregation

Depreciation recapture is the tax concept that applies when a property owner sells an asset after claiming depreciation deductions. Cost segregation does not create recapture by itself. It changes the timing and classification of depreciation by identifying assets that may properly be treated as 5-year property, 15-year land improvements, QIP 15-year property, 27.5-year residential rental property, or 39-year nonresidential real property.

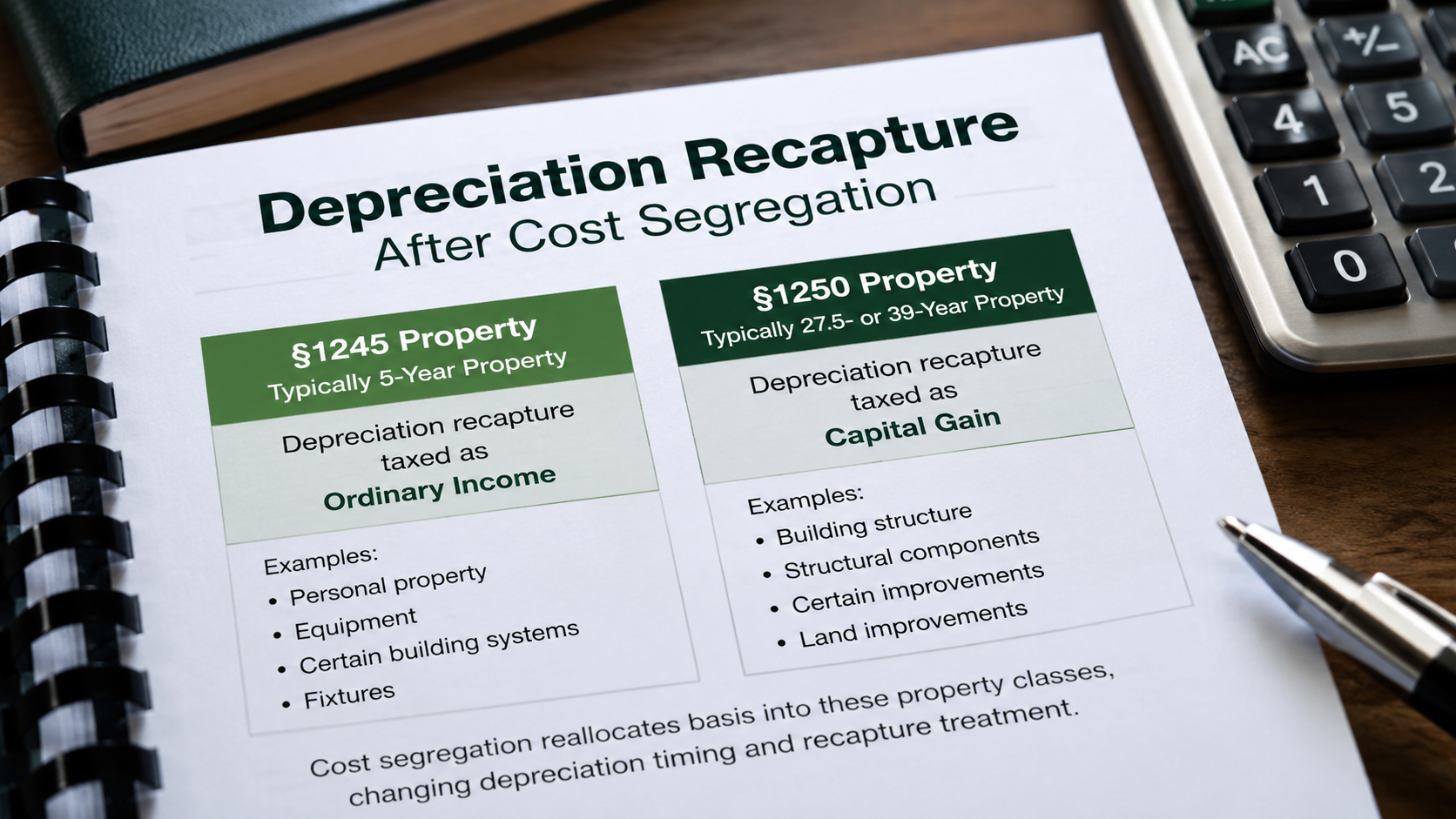

The IRS Cost Segregation Audit Technique Guide focuses heavily on whether assets are properly classified as §1245 property or §1250 property. That same distinction matters at sale. In broad terms, §1245 property is generally tied to tangible personal property and certain specialty assets, while §1250 property generally includes buildings and structural components.

This is why the front-end classification matters. A study that supports 5-year property with engineering logic gives the investor a clearer picture of both current depreciation and future sale consequences. Weak classification can create problems during both audit review and exit planning.

How Recapture Works by Asset Class

A cost segregation study separates depreciable basis into supported asset groups. Common classifications include 5-year property for qualifying tangible personal property, 15-year land improvements for qualifying site improvements, QIP 15-year property for qualifying interior improvements to nonresidential real property, 27.5-year residential rental property, and 39-year nonresidential real property.

When the property is sold, depreciation tied to §1245 property can generally be recaptured as ordinary income to the extent of gain and prior depreciation. That can affect assets such as certain specialty equipment, removable fixtures, dedicated equipment support, and other qualifying personal property. By contrast, depreciation tied to §1250 property is handled differently, with special treatment for real property depreciation.

This is one reason investors should not view cost segregation as a single tax number. The report should show what was moved, why it was moved, and how it was classified. Articles such as cost segregation vs straight-line depreciation help frame the larger strategy, but recapture planning requires looking at the asset schedule itself.

Why Recapture Planning Matters for Investor Returns

Investors often ask, “If I have to deal with recapture later, why do cost segregation now?” The practical answer is timing, cash flow, and reinvestment flexibility. A deduction today can help reduce taxable rental income, free up capital, improve debt service coverage, fund improvements, or support additional acquisitions.

Recapture is usually a future event. The value of cost segregation often comes from using tax savings during the ownership period instead of waiting decades to recover the same basis through 27.5-year residential rental property or 39-year nonresidential real property depreciation. That timing can be especially important for investors who are actively scaling a portfolio.

The issue is not whether recapture exists. The issue is whether the investor planned for it. A smart plan weighs current cash flow, expected holding period, exit price, passive activity rules, debt payoff, state tax exposure, and possible 1031 exchange planning.

Where Recapture Planning Shows Up Most Often

Recapture planning matters across many property types, but it becomes especially important when a property has meaningful 5-year property or 15-year land improvements. Multifamily properties, short-term rentals, self-storage facilities, medical offices, strip malls, car washes, mobile home parks, and industrial properties can all have different asset mixes.

For example, land improvement heavy properties may include parking lots, fencing, site lighting, drainage, landscaping, and similar assets that can create meaningful 15-year land improvements when properly supported. Investors evaluating these properties should understand both the upfront depreciation benefit and the later sale impact. This is why land improvement heavy cost segregation requires careful engineering review.

Commercial renovation projects can add another layer. Qualifying interior improvements may be QIP 15-year property, while other improvements remain part of 39-year nonresidential real property. That distinction can affect both depreciation timing and the tax profile of a later sale.

How to Plan for Recapture Before the Exit

The best time to think about recapture is before the cost segregation study is finalized, not after a buyer makes an offer. Investors, CPAs, and cost segregation specialists should understand the likely hold period, property type, financing plan, and exit strategy. A short hold, long hold, 1031 exchange, refinance, or partial disposition strategy can all change the analysis.

A quality study should be based on engineering methods, property records, invoices when available, site data, plans, photos, and reasonable cost allocation. It should not rely on unsupported percentages. The IRS ATG emphasizes the importance of methodology, documentation, asset descriptions, cost reconciliation, and legal analysis in a quality study.

This is also why investors should review what makes a quality cost segregation study defensible before relying on the numbers. Recapture planning is easier when the asset schedule is clear, the classifications are supportable, and the CPA can understand exactly what depreciation was claimed.

Financial Example: How Recapture Shows Up at Sale

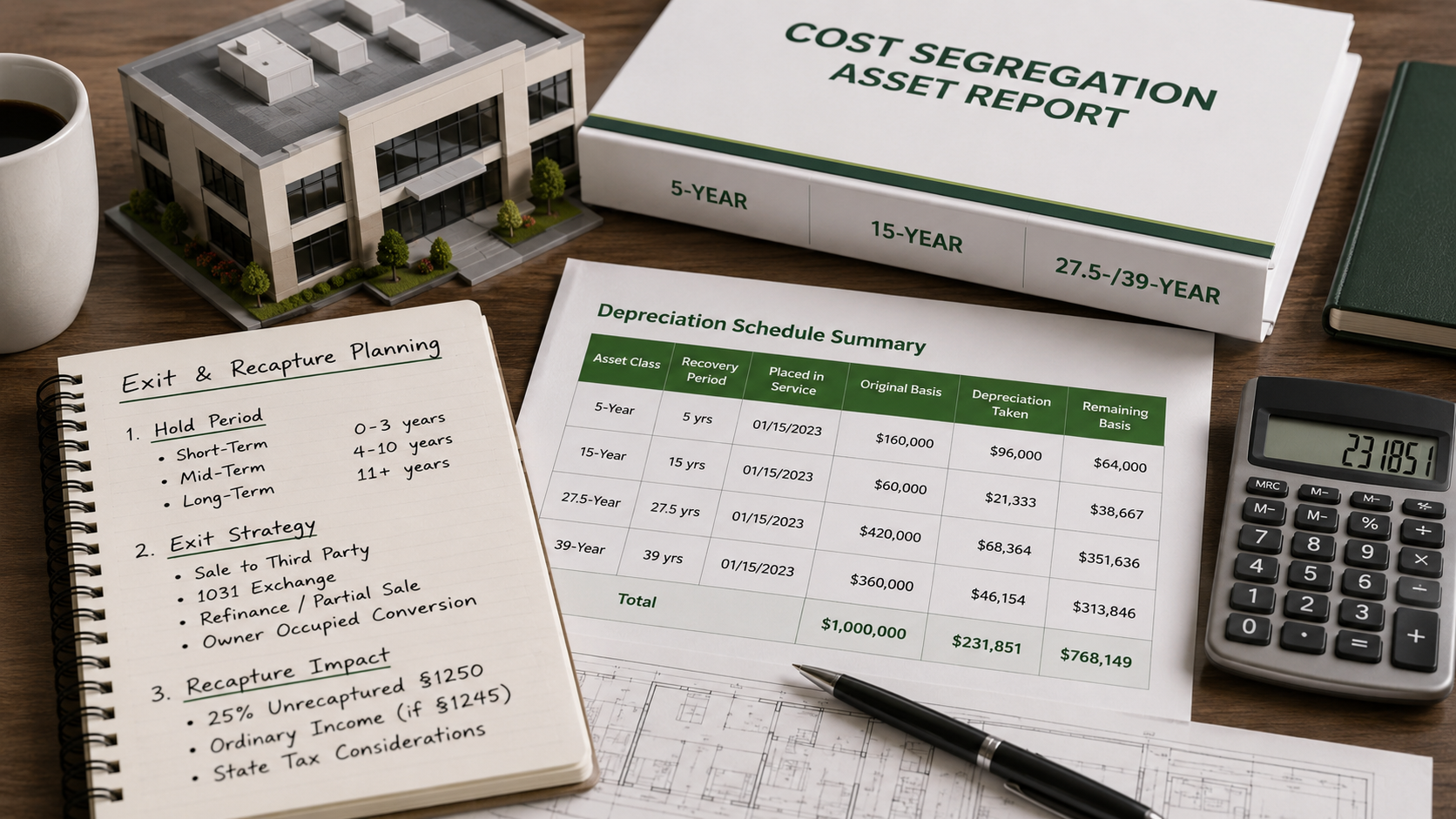

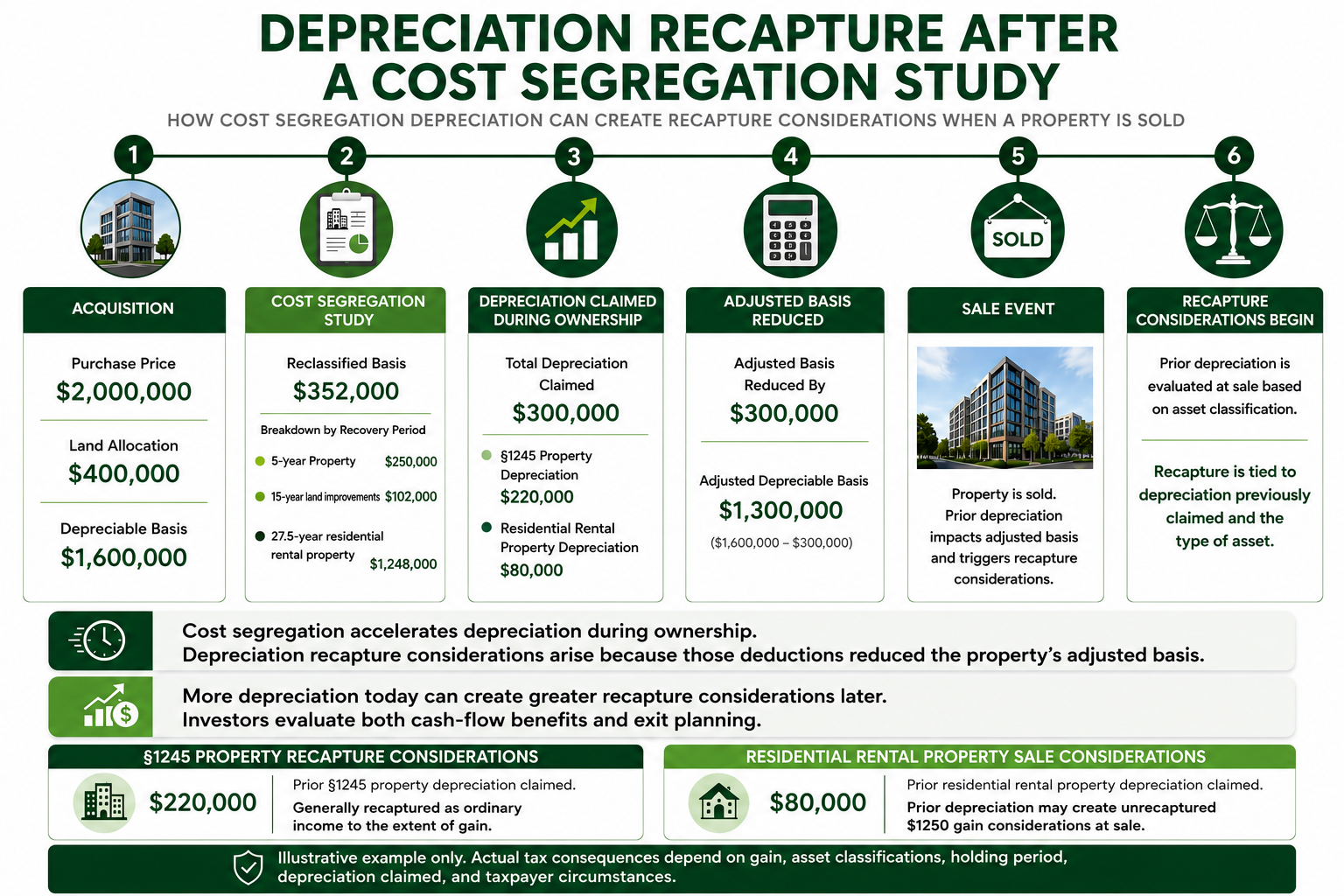

Assume an investor buys a small multifamily property for $2,000,000. Land is allocated at the default 20%, or $400,000. That leaves a depreciable basis of $1,600,000.

A cost segregation study reclassifies 22% of the depreciable basis into 5-year property and 15-year land improvements. That equals $352,000 of reclassified basis. In this example, $250,000 is allocated to 5-year property and $102,000 is allocated to 15-year land improvements. The remaining $1,248,000 stays primarily as 27.5-year residential rental property.

Now assume the investor holds the property for several years and claims $300,000 of total depreciation before selling. Of that amount, $220,000 came from the 5-year property and 15-year land improvements identified in the study, while $80,000 came from the 27.5-year residential rental property.

If the property later sells for a gain, the depreciation tied to the reclassified assets does not disappear. The $220,000 tied to §1245 property and related accelerated classifications may create ordinary income recapture to the extent of gain. The $80,000 tied to 27.5-year residential rental property is generally handled under §1250 rules.

This is the part many investors miss: recapture is not based on the original purchase price alone. It is driven by the depreciation already claimed, the adjusted basis, the sale price, and the asset classifications inside the cost segregation report.

That does not mean the study was a mistake. If the investor used the early tax savings to improve liquidity, reduce debt pressure, fund renovations, or buy another property, the timing benefit may still be valuable. The right question is not “Will there be recapture?” The better question is “Did the early cash-flow benefit outweigh the later tax cost, and was the exit planned properly?”

A Better Way to Think About Cost Segregation and Recapture

Cost segregation should not be sold as free tax savings with no future consequences. It is a timing and classification strategy that should be evaluated with the investor’s full plan in mind. When the study is accurate, it can help investors improve cash flow while giving their CPA a clearer asset-by-asset framework for sale planning.

The strongest studies align tax treatment with engineering support. They distinguish 5-year property, 15-year land improvements, QIP 15-year property, 27.5-year residential rental property, and 39-year nonresidential real property based on facts, records, and established tax treatment. That clarity helps investors make better decisions during acquisition, ownership, and exit.

Depreciation recapture is not a reason to ignore cost segregation. It is a reason to do it carefully, document it properly, and coordinate the strategy before the sale.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.