Cost Segregation for Tenant Build-Outs in Leased Spaces

Jun 11, 2026You do not have to own the building to benefit from cost segregation. If your business paid for improvements inside a leased commercial space, those tenant improvements may create depreciable assets that can be reviewed for faster recovery. This matters for dental offices, salons, med spas, restaurants, fast food locations, fitness studios, specialty retail stores, veterinary clinics, and other tenants with build-outs that include specialized systems or business-specific assets. The key question is not just what type of business you operate, but who paid for the improvements, what was installed, how each asset functions, and whether the classifications are supported by an engineering-based study.

Let us walk you through your property. Schedule a call today.

- Tenants may use cost segregation on improvements they funded

- Build-outs often hide short-life assets inside contractor invoices

- Faster depreciation can improve cash flow for business operators

- Asset-heavy tenants often see the strongest study opportunities

- Lease terms and allowances can change the tax answer

- Tenant renovation math starts with improvement basis

- A defensible result depends on engineering and documentation

Tenant Build-Out Cost Segregation in Leased Space

Cost segregation is often marketed to real estate investors, but it is not limited to landlords or building owners. A tenant may also benefit when the tenant pays for improvements inside a leased commercial space and has a depreciable ownership interest in those improvements. These projects are often called tenant improvements, leasehold improvements, or business build-outs.

For tax purposes, the important issue is asset classification. A build-out may include long-life building components, Qualified Improvement Property, tangible personal property, specialty electrical, equipment supports, removable finishes, decorative elements, and other assets with different depreciation lives. A cost segregation study separates those costs instead of placing the entire project into one broad category.

This is especially relevant for tenants because build-out invoices are often bundled. A contractor might provide one large price for framing, plumbing, electrical, millwork, lighting, finishes, equipment connections, and indirect costs. Without a study, many of those costs may be depreciated more slowly than necessary.

Tenant improvements may also overlap with Qualified Improvement Property when interior improvements are made to nonresidential real property after the building was first placed in service. QIP can be valuable, but it does not replace cost segregation. A study can still identify 5-year property inside the larger tenant improvement project.

How Tenant Improvement Assets Are Classified

A tenant build-out usually begins with leases, construction drawings, contractor invoices, change orders, equipment lists, and payment applications. Cost segregation reviews those records to identify what was installed, what each asset serves, and how the cost should be allocated.

Some assets usually remain 39-year building property. Examples include structural components, standard walls, roof systems, general plumbing, general electrical, standard HVAC, ordinary building lighting, doors, ceilings, and components related to the general operation or maintenance of the building. These items do not become 5-year property simply because a tenant uses the space for business.

Other assets may qualify for faster depreciation when facts support the classification. Examples can include certain removable finishes, specialty lighting, dedicated electrical serving qualifying equipment, business-specific cabinetry, decorative elements, equipment connections, point-of-sale infrastructure, security systems, sound systems, and other tangible personal property.

The distinction between general building systems and business-specific systems is critical. A fast food tenant may have dedicated electrical and plumbing for kitchen equipment. A dental office may have specialty connections for dental chairs, compressors, vacuum systems, and imaging equipment. A salon may have dedicated circuits and plumbing for styling and shampoo areas. That is why dedicated vs general purpose electrical outlets can matter in tenant improvement studies.

A strong study uses an engineering method to connect the tax classification to the physical asset and cost records. The goal is to identify the asset, support the cost, document the use, assign the correct recovery period, and reconcile the final allocation back to the tenant’s actual depreciable basis.

Why Faster Depreciation Matters for Business Tenants

Tenant build-outs can consume major capital before a business reaches stable revenue. A restaurant may invest heavily in kitchen infrastructure. A dental office may spend heavily on treatment rooms and specialty systems. A fitness studio may need flooring, sound, lighting, locker areas, and equipment support. A salon or med spa may require plumbing, cabinetry, specialty lighting, and customer-facing finishes.

When all of those costs are depreciated slowly, the tax benefit may arrive long after the cash has already left the business. Cost segregation changes the timing of deductions by identifying assets that can be depreciated over shorter recovery periods. It does not change the total amount spent. It can change when the deductions become available.

That timing can matter for cash flow. Faster depreciation may reduce taxable income, preserve working capital, and help fund payroll, inventory, marketing, equipment, or expansion. For operators opening multiple locations, the timing benefit can become even more important because each new leased space may involve another major build-out.

For a broader comparison of slow depreciation versus accelerated classifications, see cost segregation vs straight-line depreciation. The same timing logic that helps property investors can also help tenants who paid for depreciable improvements.

Which Tenant Build-Outs Are Often the Best Fit

The best tenant candidates are usually asset-heavy businesses. These are tenants whose spaces require more than paint, carpet, and basic office improvements. The more specialized the build-out, the more likely it is that the project deserves a cost segregation review.

Restaurants and fast food locations are often strong candidates because they may include dedicated kitchen equipment connections, food service infrastructure, specialty plumbing, beverage systems, customer area finishes, signage, and equipment-related electrical. These projects can involve a meaningful mix of 5-year property, QIP 15-year property, and 39-year building components.

Dental offices, medical clinics, med spas, and veterinary clinics can also be strong candidates because their build-outs may include treatment rooms, specialized equipment connections, dedicated plumbing, specialty electrical, cabinetry, lighting, imaging support, sterilization areas, and patient-facing finishes. The value is not in labeling the whole clinic as 5-year property. The value is in separating the specific assets that qualify.

Salons, spas, fitness studios, childcare centers, specialty retail stores, and showroom spaces may also benefit when the tenant pays for meaningful improvements. A salon may have shampoo plumbing, styling stations, specialty lighting, and cabinetry. A fitness studio may have specialized flooring, mirrors, sound systems, lighting, and equipment supports. A retail tenant may have removable displays, decorative features, security systems, and specialty lighting.

The opportunity is usually weaker for basic office tenants with modest improvements and limited specialty systems. A small office refresh with paint, standard carpet, and basic partitions may not justify a full study. Cost segregation is most useful when the tenant improvement cost is large enough and the asset mix is specialized enough to create a meaningful cash-flow benefit.

How Tenants Should Plan Before Starting a Study

The first planning question is ownership. Who paid for the improvements, and who owns them for tax purposes? If the tenant paid directly and capitalized the build-out, the tenant may have depreciable basis. If the landlord paid through a tenant improvement allowance, the lease terms and tax treatment must be reviewed. In some cases, the tenant may have depreciable basis. In other cases, the landlord may own and depreciate the improvements.

The second question is timing. If the build-out is new, the study can help classify assets correctly from the start. If the build-out was completed in a prior year and placed on the books as 39-year property, the taxpayer may need to discuss a change in accounting method with their CPA. The study can provide the asset-level detail needed for that analysis.

The third question is documentation. Strong records may include the lease, tenant allowance provisions, contractor invoices, AIA payment applications, change orders, drawings, equipment schedules, fixed asset records, payment support, photos, and depreciation schedules. The IRS Audit Technique Guide focuses heavily on documentation, methodology, cost support, asset schedules, engineering procedures, and reconciliation to actual costs. That makes recordkeeping especially important for tenants because the study must tie back to the build-out costs the tenant actually paid.

The fourth question is scope. A defensible study should not overstate 5-year property. Standard HVAC, general plumbing, ordinary electrical, structural components, roof systems, walls, and foundation items generally remain building property unless a specific exception or QIP treatment applies. A strong tenant improvement study separates supported specialty systems from general Building MEP and avoids forcing ordinary construction into 5-year property.

Tenants planning a new location should consider depreciation before the project is closed out. During construction, it is easier to preserve invoices, identify specialty systems, document equipment connections, and organize costs. That is why commercial renovation tax planning can be valuable before the space opens for business.

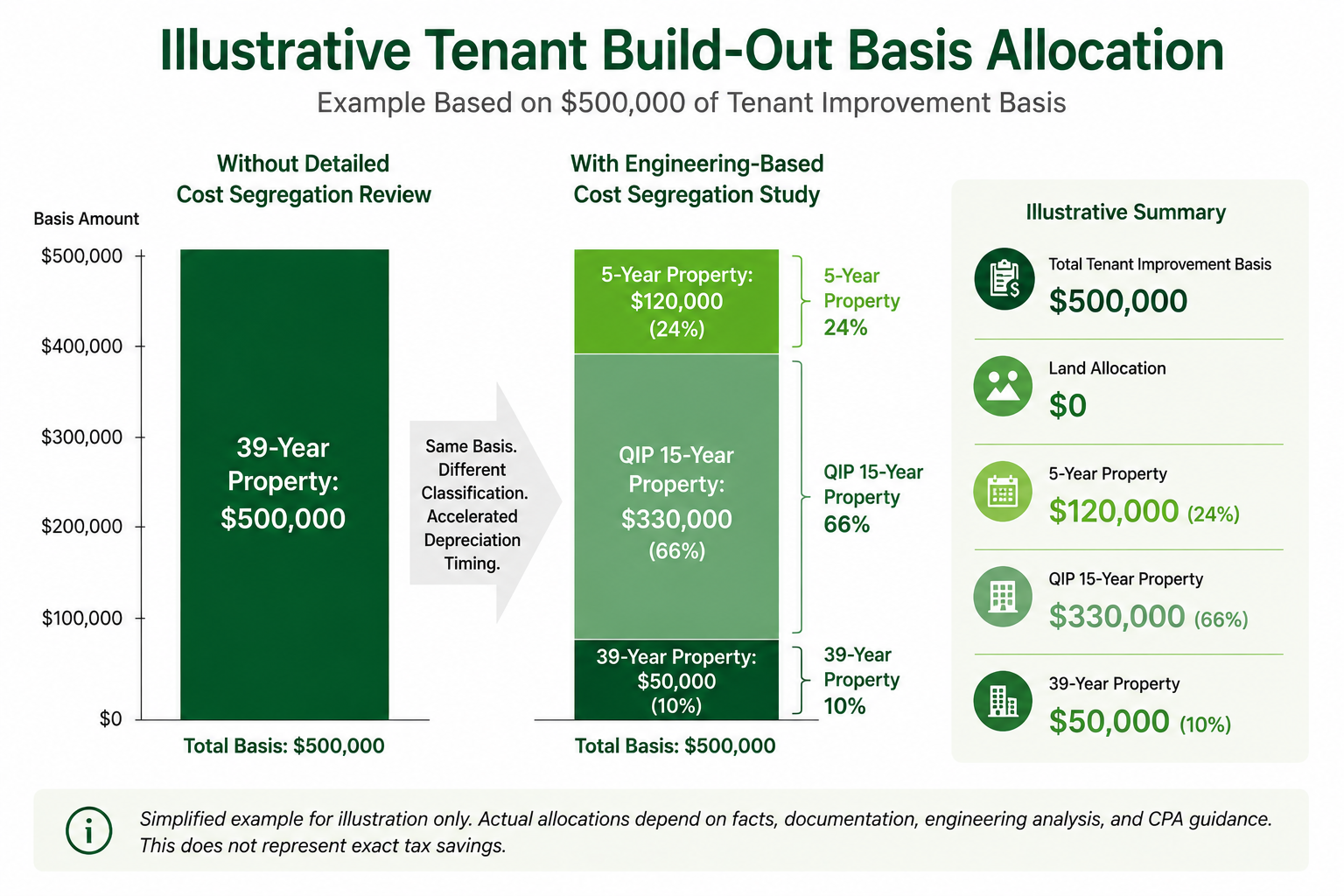

A Tenant Renovation Example Using Improvement Basis

Assume a tenant spends $500,000 to renovate the interior of a leased commercial space. This could be a dental office, restaurant, salon, med spa, fitness studio, veterinary clinic, or specialty retail space. Because the tenant is not buying land, the land allocation is $0. The tenant’s depreciable basis starts with the improvement costs the tenant paid for and owns: $500,000 minus $0 land allocation equals $500,000 of tenant improvement basis.

For an interior tenant renovation, the study usually focuses on separating the project into three practical buckets: 5-year property, QIP 15-year property, and 39-year property. The 5-year bucket may include supported personal property such as specialty equipment connections, removable finishes, certain cabinetry, decorative elements, business-specific fixtures, security systems, sound systems, and dedicated systems serving qualifying equipment.

The QIP 15-year bucket may include qualifying interior improvements to nonresidential real property that were made after the building was first placed in service. This can be very relevant in tenant build-outs because much of the interior renovation may qualify as QIP if it is not an enlargement, elevator or escalator work, or internal structural framework. QIP should be evaluated separately from 39-year property because it has its own rules and can materially affect depreciation planning.

The 39-year bucket generally includes nonresidential real property or building components that do not qualify as 5-year property or QIP 15-year property. This may include certain structural work, general building systems, or improvements that fall outside QIP treatment. Standard HVAC, general plumbing, ordinary electrical, walls, roof, structural components, and general Building MEP should not be treated as 5-year property simply because the tenant operates a specialized business in the space.

Now assume an engineering-based study supports the following allocation from the $500,000 tenant improvement basis:

- 5-year property: $120,000

- QIP 15-year property: $330,000

- 39-year property: $50,000

The total still equals the same $500,000 basis. The study does not create new deductions. It changes classification and timing by identifying which costs belong in each recovery period.

This is different from a building acquisition. If an investor buys a property, part of the purchase price usually must be allocated to land because land is not depreciable. But in a tenant-funded interior renovation, the tenant is generally not buying land. The analysis starts with the tenant’s actual improvement basis, then separates the assets based on function, documentation, and tax classification.

The cash-flow benefit comes from timing. If $120,000 can be treated as 5-year property and $330,000 can be treated as QIP 15-year property, the tenant may recover a meaningful portion of the renovation cost faster than if the full $500,000 were treated as 39-year property. The exact tax result depends on the tenant’s income, tax rate, entity structure, placed-in-service date, bonus depreciation rules, and CPA guidance.

The Bottom Line for Tenants in Leased Commercial Spaces

Cost segregation is not only a landlord strategy. Tenants may also benefit when they pay for and own improvements inside leased commercial space. The best opportunities often appear in asset-heavy build-outs such as restaurants, fast food locations, dental offices, medical clinics, med spas, salons, fitness studios, veterinary clinics, and specialty retail spaces.

The strongest results come from engineering-based analysis, not broad assumptions. A quality study should classify assets properly, identify § 1245 and § 1250 property, separate general Building MEP from supported specialty systems, document the cost basis, and reconcile allocations to actual tenant records. That approach supports both the tax benefit and the audit posture.

A tenant improvement study is not about calling every build-out cost 5-year property. It is about identifying the assets that already qualify for faster recovery under established tax treatment, documenting them clearly, and giving the business owner a practical depreciation strategy based on the improvements they actually funded.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.