Stop Paying Too Much Tax on Your Investment Property Income

Jun 02, 2026Real estate investors often focus on rent growth, financing, and appreciation, but miss one of the most practical levers inside the property itself: depreciation. If your building is being treated as one long-life asset, you may be paying tax sooner than necessary. Cost segregation helps identify building components that can be depreciated over shorter recovery periods instead of waiting 27.5 or 39 years. For investors, that can mean stronger after-tax cash flow, better reinvestment capacity, and less money unnecessarily tied up with the IRS.

Let us walk you through your property. Schedule a call today.

Key Takeaways

- See why investors often overpay tax through slow depreciation.

- Learn how engineers separate short-life assets from building costs.

- Understand how accelerated depreciation improves after-tax cash flow.

- Identify property types where hidden tax savings may exist.

- Plan cost segregation around acquisitions, renovations, and tax timing.

- Review how reclassification can shift deductions into earlier years.

- Use IRS-aligned engineering to support defensible investor savings.

Stop Treating Every Dollar Like a 27.5 or 39-Year Asset

The tax problem is simple: many investors buy or improve real estate, then depreciate most of the property as if every component is part of the building structure. Residential rental buildings are generally depreciated over 27.5 years, and nonresidential buildings are generally depreciated over 39 years. That treatment may be correct for walls, structural systems, and many building components, but it does not mean every depreciable dollar belongs in the same bucket.

Cost segregation applies tax and engineering logic to determine which portions of a property may be classified as shorter-life property. The IRS ATG describes cost segregation as a method for allocating property costs among assets such as land, land improvements, buildings, equipment, furniture, and fixtures when lump-sum costs need to be separated. For investors, the goal is not to create deductions out of thin air. The goal is to classify the property correctly so depreciation better matches the actual assets inside and around the building.

That classification matters because certain assets may qualify as 5-year, 7-year, or 15-year property instead of remaining inside the long-life building category. Items such as certain specialty electrical components, dedicated equipment support, removable finishes, site improvements, and personal property may require separate analysis. The IRS framework focuses heavily on whether an asset is tangible personal property, a land improvement, a building component, or part of the building’s structural system.

This is why a serious study is not just a tax estimate. It is an engineering-based classification process tied to tax rules, construction documents, asset use, and cost support. Investors who want a deeper overview of how the strategy works can review cost segregation benefits before deciding whether a study fits their property.

How Engineers Find the Tax Savings Inside the Building

A cost segregation study starts by breaking the property into asset categories. Instead of viewing the building as one large number, the study reviews components, costs, drawings, invoices, site conditions, and asset use. The goal is to determine which items should remain as building property and which items may be separated into shorter recovery periods.

The strongest studies rely on an engineering methodology, not a generic percentage. The IRS ATG identifies detailed engineering approaches as common cost segregation methods and emphasizes documentation, methodology, cost basis support, and asset classification. This matters because the result needs to be useful not only for tax planning, but also for support if the study is ever reviewed.

The practical investor benefit comes from moving eligible costs into faster depreciation categories. Many studies identify a meaningful amount of 5-year property, some 15-year land improvements, and a remaining long-life building balance. The 5-year category is especially important because it often produces the strongest near-term depreciation impact. Investors researching this category can use cost segregation 5-year property as a helpful reference point.

Cost segregation is also different from simply choosing accelerated depreciation on the entire building. The building itself generally stays in its long-life category. The study identifies separate assets that may be depreciated differently because they are not part of the building structure for depreciation classification purposes. That distinction is what makes the engineering review so valuable.

Why Paying Less Tax Now Can Change the Investor Math

The value of cost segregation is not just a lower tax bill. It is the timing of deductions. A dollar of depreciation used earlier can improve cash flow, reduce taxable income, and give an investor more flexibility to pay down debt, fund improvements, build reserves, or acquire another property.

Without cost segregation, an investor may wait decades to recover costs that could potentially be depreciated much faster. That delay creates a cash flow drag. The investor still receives depreciation, but too slowly to fully support near-term portfolio growth. This is why cost segregation vs straight-line depreciation is such an important comparison for rental property owners.

Bonus depreciation can make the timing difference even more powerful when the property and assets qualify. Current IRS guidance states that the 100% additional first-year depreciation deduction has been restored for certain qualified property acquired and placed in service after January 19, 2025. That does not mean every cost segregation asset automatically qualifies. Each asset still has to meet the applicable requirements, including recovery period, acquisition, original use or used property rules, and placed-in-service rules.

This is where investors need to be careful. Cost segregation identifies and classifies assets. Bonus depreciation determines whether eligible short-life assets can be deducted even faster. The two strategies often work together, but they are not the same thing. For a broader planning view, investors can review bonus depreciation and cost segregation.

Where Investors Commonly Find Missed Depreciation

Cost segregation can apply across many investment property types. Common use cases include multifamily properties, short-term rentals, apartment buildings, office buildings, retail centers, medical offices, industrial properties, self-storage facilities, restaurants, and mixed-use properties. The right fit depends on the purchase price, improvement costs, property type, holding period, tax position, and investor goals.

Acquired properties are common candidates because the purchase price often gets allocated broadly. A study can help separate the depreciable building basis into appropriate asset classes after land is removed. Renovated properties can also be strong candidates because improvement costs may include a mix of structural building work, qualified improvement property, equipment, finishes, and specialty systems.

New construction can benefit as well, especially when cost records, drawings, and contractor detail are available. Better documentation can support more precise allocations. For developers and investors planning improvements early, the study can also help capture the tax impact of design and construction decisions before records become harder to reconstruct.

Short-term rental investors may also benefit when they have the right income profile and tax facts. Cost segregation can create larger depreciation deductions, but whether those losses offset other income depends on passive activity rules, material participation, and the investor’s specific tax situation. The depreciation strategy is powerful, but it needs to be coordinated with the investor’s CPA.

Timing the Study Before Tax Savings Slip Away

Timing matters. The best time to consider cost segregation is usually when a property is acquired, constructed, renovated, or placed in service. That is when documentation is freshest and tax planning decisions can be made before returns are filed. Waiting does not always eliminate the opportunity, but it can make the process more complex.

Investors who already own property may still be able to complete a lookback study and catch up missed depreciation through an accounting method change. This can be useful when a property was previously depreciated too slowly. However, it should be reviewed with a tax advisor because the treatment depends on the facts, prior filings, and current tax posture.

The strategy should also consider ownership plans. If an investor expects to sell quickly, accelerated depreciation may still help, but depreciation recapture and exit timing need to be modeled. If an investor plans to hold long term, the cash flow benefit may be especially valuable because early deductions can support years of portfolio operations.

A smart study is also conservative enough to be defensible. The IRS ATG emphasizes methodology, documentation, cost basis reconciliation, legal analysis, and clear identification of Section 1245 property. A study that overreaches can create audit risk. A study that is too vague may fail to capture the full opportunity. The right target is not the biggest number possible. It is the best-supported number.

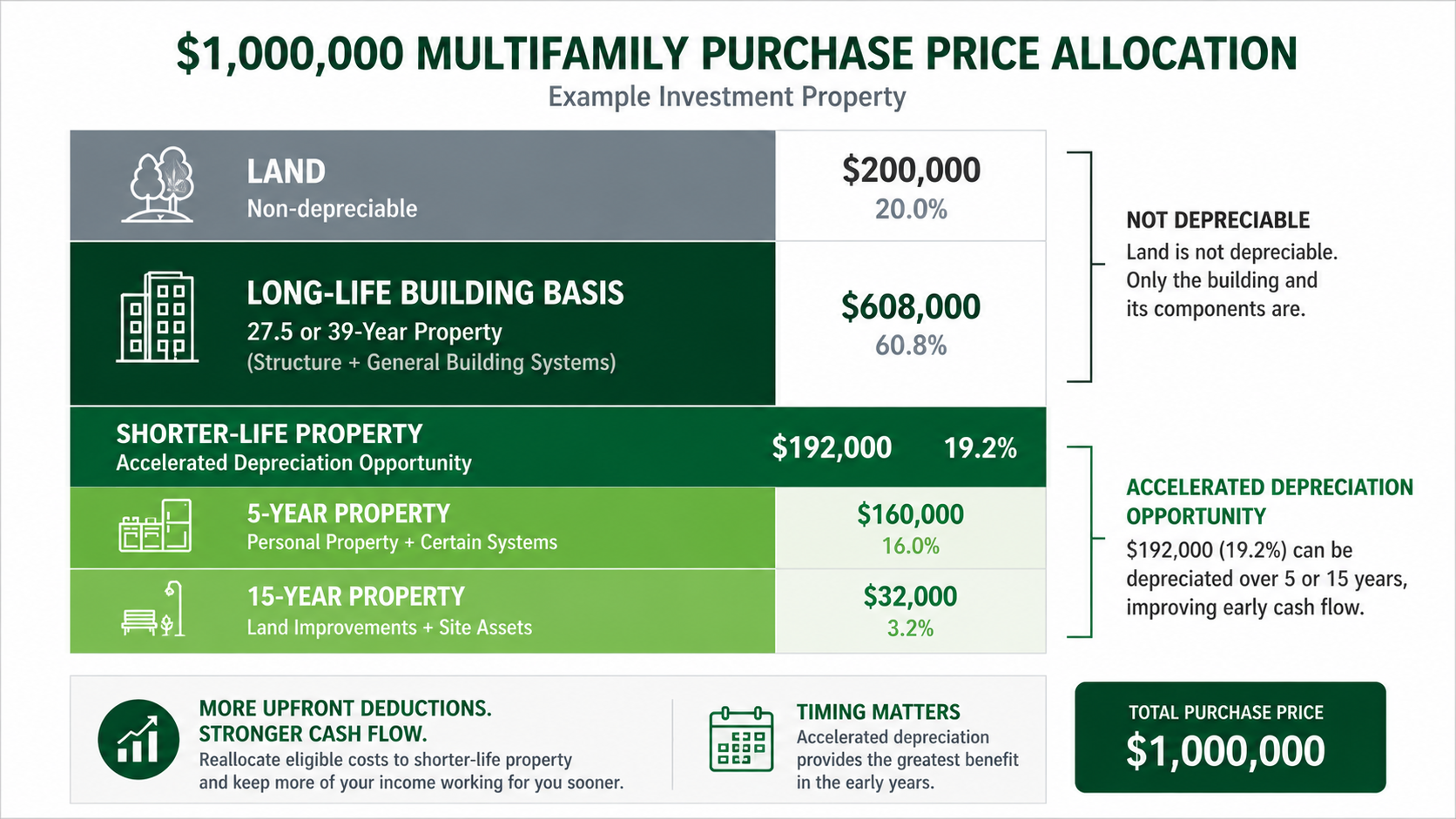

A $1,000,000 Rental Property Cash Flow Example

Assume an investor purchases a $1,000,000 multifamily property. After allocating $200,000 to land, the depreciable building basis is $800,000. Without cost segregation, most of that $800,000 may be depreciated over 27.5 years, creating roughly $29,091 of annual depreciation before considering other adjustments.

Now assume an engineering-based cost segregation study reclassifies 24% of the depreciable basis into shorter-life property. That equals $192,000 shifted out of the long-life building category. In many investor studies, reclassification commonly falls in the 17% to 28% range, depending on property type, documentation, and asset mix. Higher results, sometimes up to 32%, should only be used when the facts and engineering support are strong.

In this example, the reclassified amount might include a dominant share of 5-year property, with a smaller portion assigned to 15-year land improvements. That mix matters because 5-year property generally creates faster deductions than 15-year property. If qualified assets are eligible for 100% bonus depreciation under current rules, a large portion of that $192,000 may be deductible much earlier than it would be under straight-line building depreciation.

The result is not a permanent tax exemption. It is an acceleration of depreciation. But for investors, timing can be extremely valuable. If accelerated depreciation reduces taxable income today, the investor may have more cash available for reserves, renovations, debt reduction, or the next acquisition. That is the core reason cost segregation is often described as a cash flow strategy, not just a tax study.

Use the Tax Code Without Overpaying the IRS

Cost segregation helps investors stop treating every building dollar the same. When a property includes assets that can be classified into shorter recovery periods, an engineering-based study can move those deductions forward and improve after-tax cash flow. The strongest results come from proper asset classification, reliable documentation, and IRS-aligned methodology.

The strategy is well established, but it should be handled carefully. Investors need support for the property basis, the asset categories, the recovery periods, and the assumptions used in the study. That is what separates a defensible cost segregation study from a rough tax estimate.

If your investment property is being depreciated as one slow building, you may be paying more tax than necessary. With the right engineering review and tax planning, cost segregation can help you use depreciation more strategically, keep more cash working inside your portfolio, and align your tax treatment with the actual assets you own.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.