How One Tax Court Case Changed Cost Segregation for Investors

May 28, 2026Cost segregation did not become a powerful investor strategy by accident. One Tax Court case helped clarify why certain assets inside a building can be treated differently from the building itself for depreciation purposes. That case, Hospital Corporation of America v. Commissioner, is now one of the most important legal references behind modern cost segregation. For property investors, the lesson is simple: tax savings depend on proper asset classification, engineering support, and defensible documentation.

Key Takeaways

- See how HCA shaped modern cost segregation classification logic.

- Learn how assets move into shorter depreciation categories.

- Understand why classification can improve investor cash flow.

- Review which properties can benefit from HCA-based analysis.

- Use engineering support to strengthen depreciation planning decisions.

- Compare reclassification percentages on a practical investor example.

- Connect court-backed classification with IRS-aligned tax treatment.

The HCA Decision Behind Modern Cost Segregation

Hospital Corporation of America v. Commissioner helped shape the way cost segregation studies classify building-related assets for depreciation. The key issue was whether certain items connected to hospital facilities were structural components of the building or tangible personal property eligible for shorter recovery periods.

The IRS argued that many of the disputed items should be depreciated over the same recovery period as the building. The taxpayer argued that some assets were not simply part of the building structure. They served specific business functions and should be treated as tangible personal property.

The Tax Court agreed that older Investment Tax Credit classification rules could still help determine whether property qualified as §1245 property under ACRS and MACRS. That matters because §1245 property can often use shorter recovery periods, while §1250 building property generally depreciates over much longer periods. This is why modern cost segregation depends on classification logic, not just construction cost totals.

For investors, HCA did not create a blank check to accelerate everything. It confirmed that the right assets, supported by the right facts, can be separated from the building and depreciated faster.

How HCA Connects Assets to Depreciation Categories

A cost segregation study works by separating property costs into different tax recovery categories. Instead of treating an entire building as 27.5-year residential rental property or 39-year nonresidential real property, the study identifies assets that may qualify as shorter-life property.

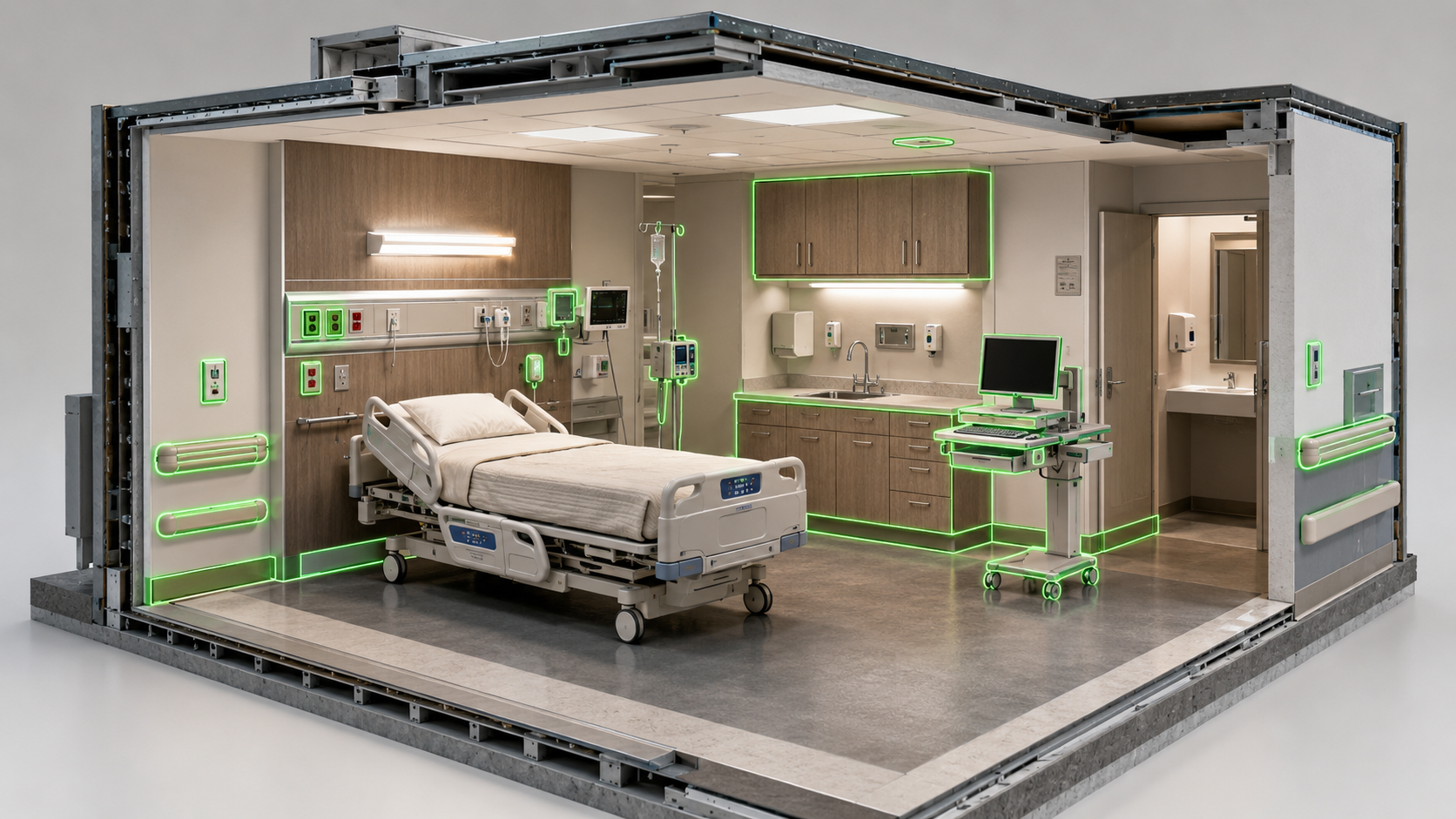

This is where HCA matters. The decision supports the idea that tangible personal property included in an acquisition or construction project should be treated according to its actual character. In practice, that means the study must identify what the asset is, how it is used, whether it relates to building operation, and whether it supports a specific business function.

Common categories include building property, land improvements, and tangible personal property. A strong study may identify 5-year property such as certain specialty finishes, dedicated systems, equipment support components, removable assets, and other property that is not inherently part of the building structure.

The engineering methodology matters because classification is fact-specific. A study should document the asset, connect it to the correct tax category, assign a reasonable cost, and reconcile those costs to the total project or purchase basis. That is why the IRS ATG emphasizes methodology, documentation, legal analysis, and cost reconciliation as markers of a quality study.

Why HCA Matters for Investor Cash Flow

The practical impact of HCA is faster depreciation where the facts support it. When costs are moved from long-life building property into shorter-life categories, investors can claim larger depreciation deductions earlier in the ownership period. That can reduce taxable income and improve after-tax cash flow.

This matters most when investors are making decisions about acquisitions, renovations, refinances, and hold periods. A property that looks average before tax planning may produce stronger cash-on-cash performance after depreciation is modeled correctly. The benefit is not just a larger deduction. It is better timing.

For example, an investor comparing two properties may use cost segregation projections to estimate early-year tax benefits. That analysis can influence pricing, reserve planning, debt strategy, and whether improvements should be completed before or after acquisition. When paired with cost segregation benefits, HCA-based classification gives investors a clearer view of how building components affect ROI.

Still, the case also reinforces caution. Accelerated depreciation is valuable only when the classification is supportable. Overstating short-life assets can create audit risk, repayment exposure, and unnecessary friction with tax advisors.

Where Investors See HCA Principles in Real Properties

HCA principles can show up across many investment property types. Multifamily properties may include qualifying personal property in unit interiors, amenities, specialty flooring, appliances, and certain dedicated systems. Commercial properties may include tenant-specific buildouts, specialty electrical, decorative finishes, equipment connections, and business-use assets.

Short-term rentals can also benefit when assets are properly identified and documented. Furniture, fixtures, equipment, and certain interior components may be analyzed separately from the building shell. Retail, restaurant, medical, light industrial, and office properties often have even more specialized assets that require detailed engineering review.

Renovation projects can be especially important. When investors upgrade interiors, replace finishes, add dedicated systems, or improve commercial spaces, the classification of those costs affects depreciation timing. For commercial properties, some improvements may also require analysis alongside Qualified Improvement Property rules.

The common thread is not the property type. It is whether the study can identify the asset, explain the classification, support the cost, and align the result with established tax treatment.

Using HCA as a Planning Tool, Not a Shortcut

Investors should treat HCA as a planning framework, not a loophole. The case supports cost segregation when the analysis is grounded in facts, engineering, and tax classification. It does not support broad assumptions or aggressive estimates without documentation.

The best time to apply this thinking is before major tax decisions are made. Acquisition planning, renovation planning, construction closeout, and year-end tax projections are all moments when classification can affect cash flow. A study performed at the right time can help investors understand which costs may qualify for shorter lives and how those deductions may interact with bonus depreciation.

Timing also matters because depreciation strategy changes depending on placed-in-service dates, available records, and investor goals. Reviewing when to perform a cost segregation study can help owners avoid waiting until documentation is harder to obtain.

The strongest studies usually include engineering review, property inspection support, cost detail, photographs, source documentation, and a clear legal rationale. That is the kind of approach that turns HCA from a historical case into a practical investor tool.

Financial Example: HCA Logic on a $1,000,000 Property

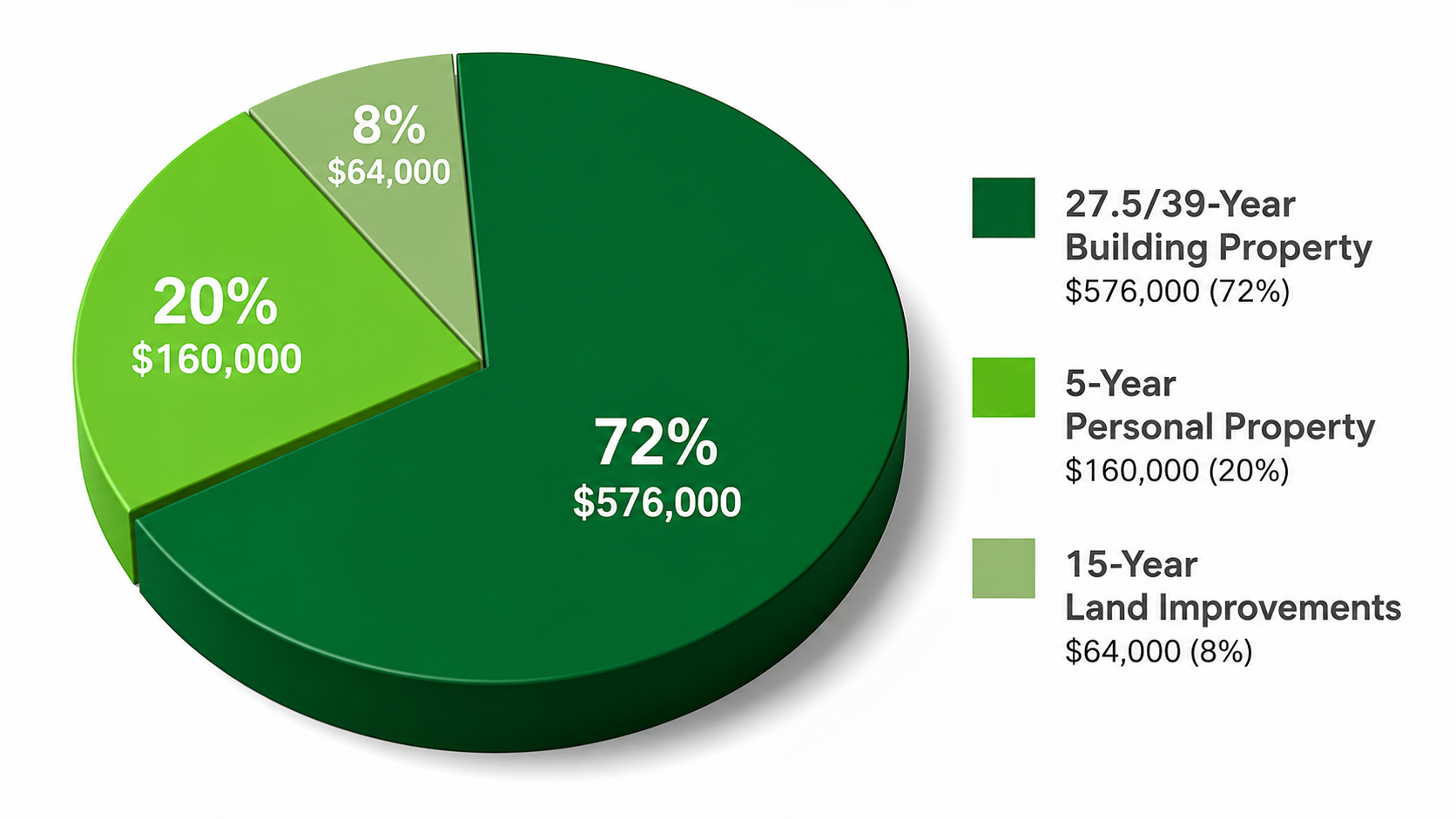

Consider an investor who purchases a small multifamily property for $1,000,000. After allocating value to land, assume the depreciable building basis is $800,000. Without cost segregation, that $800,000 would generally be depreciated over 27.5 years as residential rental property.

With a properly supported cost segregation study, a portion of that basis may be reclassified into shorter-life property. In many real estate studies, a typical reclassification range may fall around 17% to 28% of depreciable basis, depending on property type, condition, documentation, and asset mix. On an $800,000 depreciable basis, that could mean approximately $136,000 to $224,000 shifted into shorter recovery categories.

Some properties may support reclassification up to 32%, but only when the facts, engineering analysis, and documentation justify that result. A heavily improved short-term rental or specialty-use property may have more qualifying assets than a basic long-term rental. A simple apartment building with limited specialty components may fall lower.

The most important point is that 5-year property usually drives the stronger early-year result compared with 15-year land improvements. Both can matter, but 5-year assets generally create faster depreciation timing and stronger upfront cash flow impact. This is also why investors often evaluate bonus depreciation and cost segregation together when modeling after-tax returns.

Why Court-Backed Classification Still Depends on Quality

HCA changed the cost segregation landscape because it helped confirm that tangible personal property can be separated from building property under modern depreciation systems. That opened the door for investors to use engineering-based studies to identify shorter-life assets inside acquisitions and construction projects.

But the court case is only one part of the story. The IRS ATG still expects a study to classify assets correctly, explain the rationale, substantiate costs, and reconcile allocated costs to the total basis. That means the investor benefit depends on both legal support and technical execution.

A defensible cost segregation study uses an engineering method, follows IRS-aligned classification principles, and applies established tax treatment to real property facts. HCA gives investors the framework. A quality study turns that framework into measurable, supportable tax savings.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.