Is Cost Segregation Worth It for Real Estate Investors

Mar 12, 2026When property owners ask whether cost segregation is worth it, they are usually asking a simpler question:

Will this meaningfully improve my financial position?

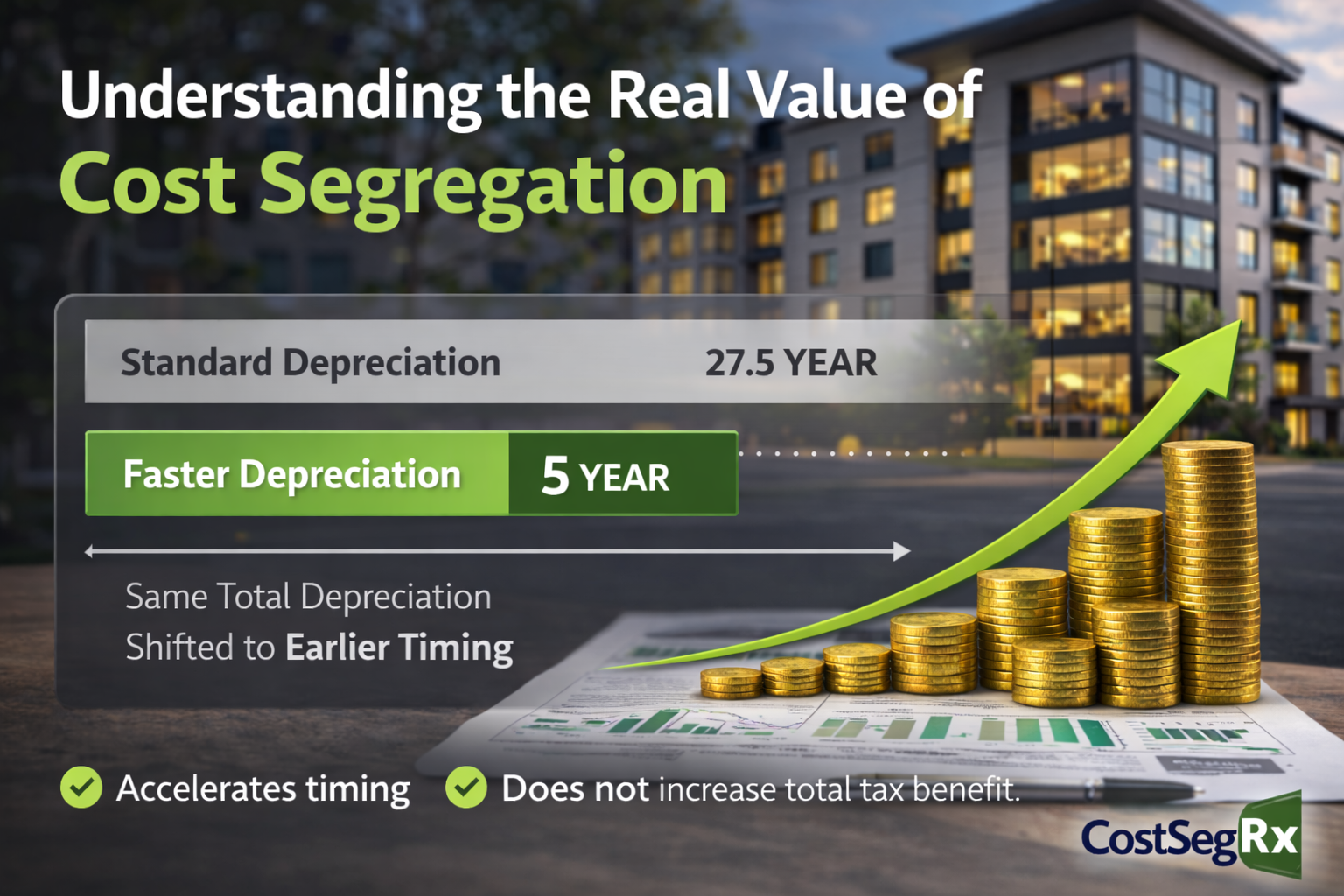

A cost segregation study does not increase the total depreciation available on a property. Instead, it accelerates when those deductions occur. Certain building components that would normally be depreciated over 27.5 years for residential property or 39 years for commercial property can often be reclassified into shorter recovery periods such as 5, 7, or 15 years.

For investors, that timing difference can significantly change early cash flow. If you are unfamiliar with how building components are separated into shorter recovery periods, you may want to read our explanation of 5-Year Property in Cost Segregation, which breaks down the types of assets commonly reclassified during a study.

Why Depreciation Timing Matters

Real estate investors often focus on total return, but timing of tax deductions can have just as much impact on portfolio growth.

Accelerating depreciation allows investors to claim a larger portion of deductions earlier in the ownership cycle. That reduction in taxable income can free up capital that might otherwise be tied up in taxes.

Many investors use that additional liquidity to:

- Reinvest in additional properties

- Fund renovations or property improvements

- Reduce leverage or operating debt

- Expand their portfolio more quickly

The property itself does not change. The strategy does.

In many cases, renovations can also create opportunities for reclassification, especially when improvements involve flooring, electrical systems, plumbing, or interior buildouts. You can learn more about how renovations interact with cost segregation in our articles on smart tax planning for residential property renovations and smart tax planning for commercial property renovations.

How Reclassification Works

Many owners assume that once a building is purchased, the entire structure must be depreciated over its standard recovery period.

However, a cost segregation study analyzes the property in detail and identifies components that qualify for shorter depreciation lives.

Examples may include:

- Flooring and specialty finishes

- Certain electrical systems that support equipment

- Dedicated plumbing or mechanical systems

- Land improvements such as parking areas or site lighting

- Equipment-related building components

These types of components often fall into the categories explained in our article on 15-Year Property in Cost Segregation, which covers land improvements and exterior site assets that may qualify for accelerated depreciation.

A Simple Example

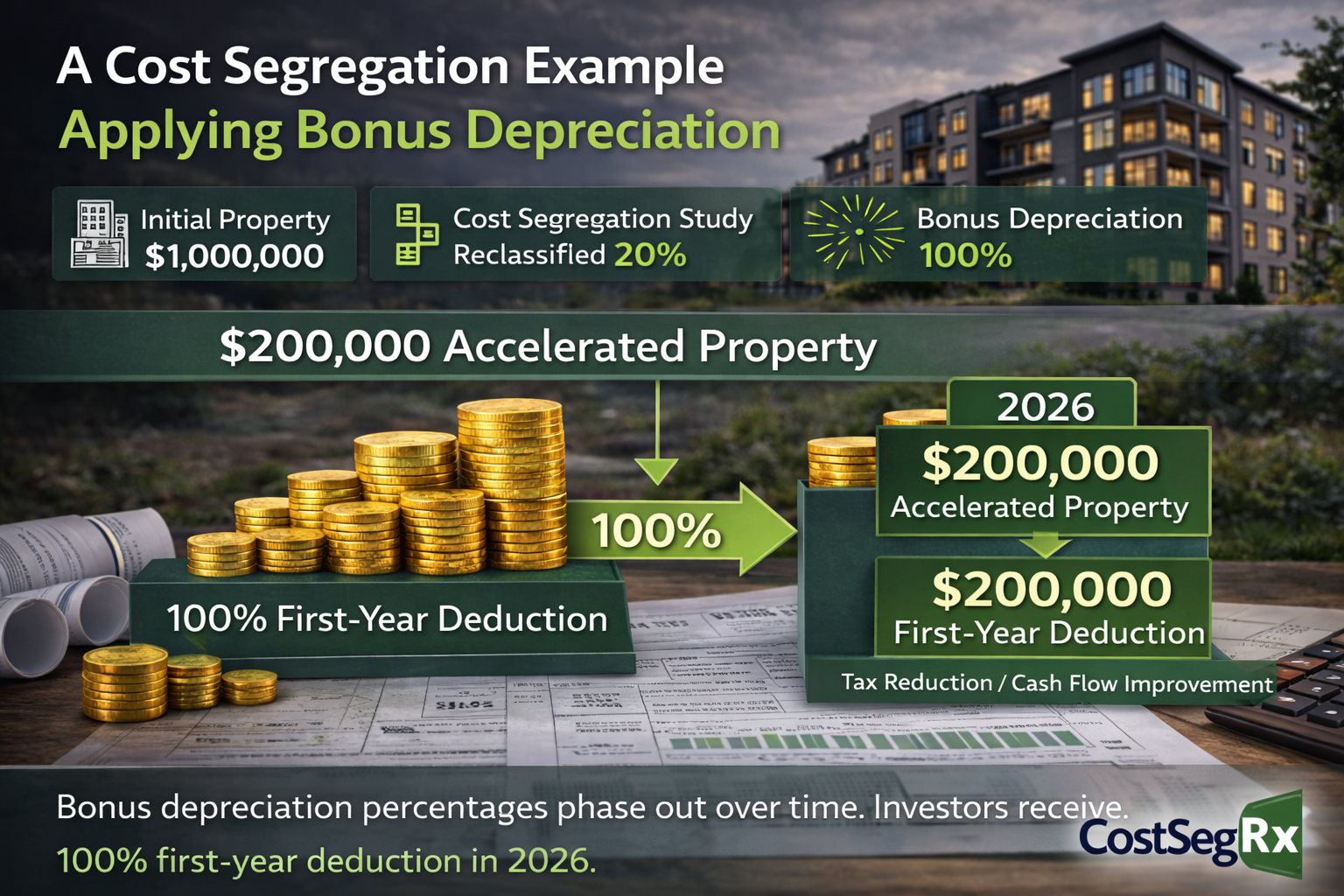

Consider a property owner who purchases a residential building with $1,000,000 of depreciable basis.

Under standard straight-line depreciation over 27.5 years, the owner may deduct roughly $36,000 per year.

If the owner is in a 35 percent tax bracket, that deduction may reduce annual tax liability by about $12,600.

Now assume a cost segregation study determines that 20 percent of the building’s components qualify for shorter recovery periods.

That means $200,000 of the property basis shifts into accelerated depreciation categories.

The total depreciation remains $1,000,000 over the life of the property. The total tax benefit does not change.

What changes is when those deductions occur.

A larger portion of depreciation may be taken earlier in the ownership period, which can significantly improve near-term cash flow.

Many of these accelerated deductions may also benefit from bonus depreciation, which you can explore further in our article on Bonus Depreciation and Cost Segregation.

A Strategy Used by Institutional Investors

Cost segregation is not a new or aggressive tax strategy. It has been recognized within the tax code for decades and is widely used by institutional real estate investors, private equity groups, and commercial developers.

In simple terms, cost segregation does not create new deductions. It changes the timing of existing ones.

When Cost Segregation May Provide the Most Value

Cost segregation tends to be most effective when:

- A property was recently purchased or constructed

- Significant renovations were completed

- The owner has strong taxable income

- Bonus depreciation is available

- The property will be held long enough to benefit from the timing shift

Every property is different, so the potential benefit should always be evaluated based on the property’s details and the owner’s tax situation.

It Is Often Not Too Late

Many property owners assume that if a building has already been depreciated for several years, they missed the opportunity.

In many cases that is not true.

A cost segregation study can often be performed retroactively. The adjustment is typically handled through IRS Form 3115, which allows previously missed depreciation to be captured without amending prior tax returns.

The Real Question

Ultimately, the value of cost segregation is not about creating additional deductions.

It is about improving the timing of depreciation so that investors can retain more capital earlier in the life of a property.

For many investors, that timing advantage can significantly improve cash flow and create opportunities for reinvestment and portfolio growth.

The question is not whether cost segregation works.

The question is whether it works for your property.

Key Takeaways

- Cost segregation accelerates depreciation timing, not total deductions

- The total tax benefit stays the same, but the timing changes

- Earlier deductions may improve near-term cash flow

- Many properties reclassify 15 to 25 percent of building components

- Institutional investors routinely use this strategy

- Retroactive studies may still be possible through Form 3115

Do you have a question about Cost Segregation?

Let us know how we can help

We hate SPAM. We will never sell your information, for any reason.