A Guide to Avoid Overestimating Short-Life Assets in Cost Segregation

May 04, 2026Cost segregation is designed to accelerate depreciation by identifying assets that qualify for shorter recovery periods. While this strategy can significantly improve early-year cash flow, it also introduces compliance risk when applied aggressively. One of the most common issues is the overestimation of short-life assets such as 5-year and 7-year property. This misclassification can lead to audit exposure, recapture risk, and financial restatements. Investors and advisors must understand where these risks originate and how to mitigate them through defensible methodologies.

Key Takeaways

- Overestimating short-life assets inflates accelerated depreciation beyond defensible limits

- Short-life assets typically include 5-year and 7-year property subject to strict classification rules

- Engineering-based methodologies reduce classification errors compared to rule-of-thumb approaches

- IRS guidance emphasizes documentation, legal analysis, and asset-level support

- Misclassification increases audit risk and potential depreciation recapture

- Overstated allocations can distort ROI projections and investor decision-making

- High-risk areas include electrical systems, plumbing, and specialty finishes

- Improper use of percentage-based allocations is a common red flag

- Defensible studies rely on detailed cost records, site inspections, and engineering analysis

- Strategic oversight ensures compliance while preserving tax efficiency

What Overestimating Short-Life Assets Means in Practice

Overestimating short-life assets occurs when a cost segregation study assigns an excessive portion of total project cost to assets classified as §1245 property. These assets benefit from accelerated depreciation schedules, often 5 or 7 years, compared to 27.5 or 39 years for §1250 property. The incentive is clear: higher allocations to short-life assets result in larger upfront deductions.

However, classification is not subjective. The IRS requires that assets meet specific criteria, including exclusion from structural components and alignment with tangible personal property definitions. The absence of bright-line rules makes this a fact-intensive determination, increasing the likelihood of misinterpretation.

For a deeper understanding of asset categorization, see cost segregation 5-year property and how these classifications are established.

How Misclassification Happens in Cost Segregation Studies

Errors typically originate from weak methodologies. Studies that rely on estimates, generalized percentages, or limited documentation are more likely to overstate short-life assets. The IRS Cost Segregation Audit Techniques Guide highlights that engineering-based approaches using actual cost records provide the highest level of accuracy.

Common sources of misclassification include:

- Assigning portions of building systems such as electrical or plumbing to short-life property without functional justification

- Using standardized allocation percentages instead of load-based or usage-based analysis

- Failing to distinguish between structural components and equipment-specific systems

- Applying residual or rule-of-thumb approaches without reconciliation to actual costs

For example, electrical distribution systems often support both building operations and equipment. Allocating a fixed percentage to short-life assets without supporting calculations is a frequent audit issue.

For further detail, see dedicated vs general purpose electrical outlets and how classification impacts recovery periods.

Why Overestimation Creates Financial and Audit Risk

The consequences of overestimating short-life assets extend beyond compliance. During an IRS examination, improperly classified assets may be reclassified into longer recovery periods. This results in depreciation recapture, increased taxable income, interest, potential penalties, and reduced credibility of the overall study.

Additionally, overstated depreciation can distort projected returns. Investors relying on inflated tax benefits may overestimate cash flow and make suboptimal acquisition or development decisions.

A defensible study is not only about maximizing deductions but ensuring sustainability under scrutiny. This is central to determining cost segregation ROI in real-world scenarios.

Where Overestimation Risks Commonly Occur

Certain asset categories consistently present higher risk due to their dual-purpose nature or complex classification rules.

Key examples include electrical systems with both general and equipment-specific loads, plumbing systems supporting both building infrastructure and process equipment, decorative finishes that may be incorrectly treated as removable personal property, and specialty lighting or millwork lacking clear functional separation.

These areas often require detailed engineering analysis and documentation to support classification decisions. The IRS emphasizes that allocations must be based on facts, not assumptions, particularly when distinguishing between §1245 and §1250 property.

Strategies to Prevent Overestimation and Strengthen Defensibility

Avoiding overestimation requires a disciplined approach grounded in methodology and documentation. The most reliable studies use detailed engineering analysis based on actual cost records, clear identification of each asset, measurable functional allocation data, reconciliation to total project cost, and legal analysis aligned with IRS guidance and case law.

Equally important is timing and preparation. Ensuring proper documentation early in the process improves accuracy and reduces reliance on estimates. For guidance on preparation, review documents needed for a cost segregation study.

A well-executed study balances acceleration with compliance, preserving both tax benefits and audit defensibility.

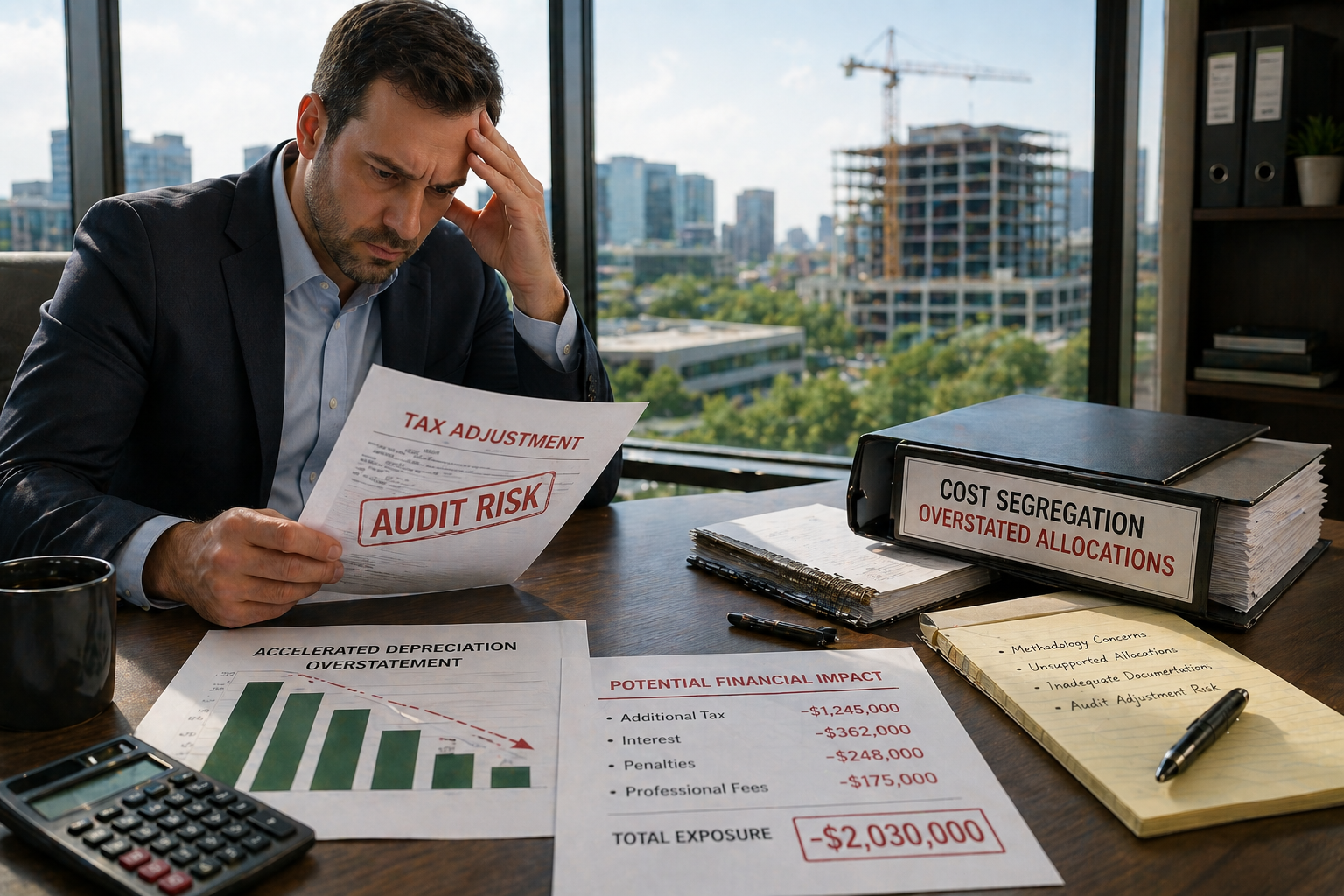

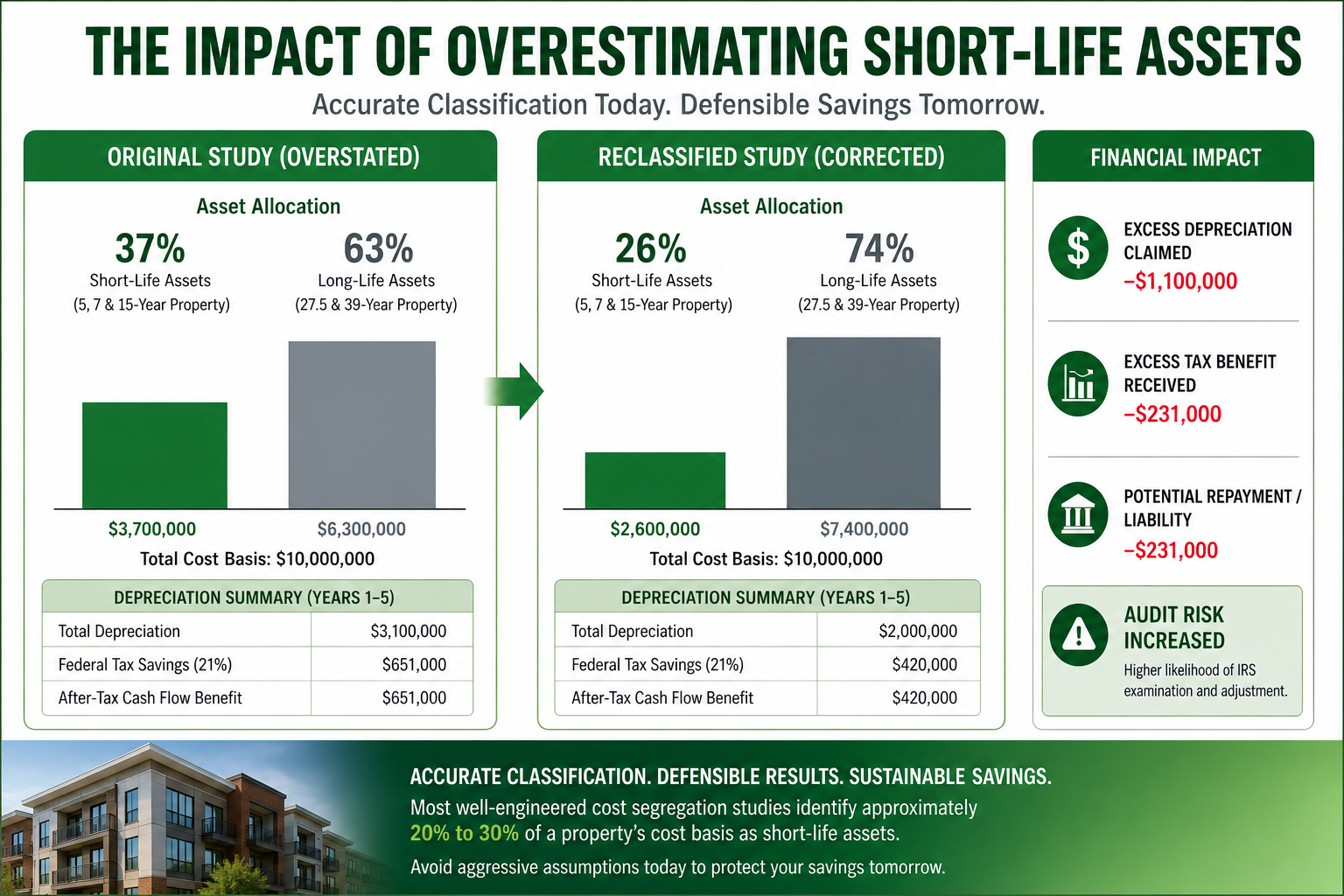

Real Impact: When Overestimation Triggers Reclassification

Consider a $10 million commercial property where a study allocates 37 percent of the cost basis to short-life assets. While this may appear reasonable at first glance, a closer review determines that a portion of those classifications lack sufficient engineering support and should be reclassified to longer recovery periods.

This adjustment reduces allowable depreciation, lowering early-year tax savings and creating a correction that may include repayment, interest, and reduced future deductions. What initially appeared to be a strong tax position becomes a weakened one under scrutiny.

This scenario highlights a critical risk in cost segregation: the issue is not always obvious overreach, but subtle over-allocation that fails to hold up when tested. Even small deviations from defensible ranges can compound into meaningful financial exposure over time.

Building Defensible Acceleration Without Crossing the Line

Cost segregation remains one of the most powerful tax strategies in real estate. However, its effectiveness depends on precision. Overestimating short-life assets undermines both compliance and investor outcomes.

The objective is not maximum acceleration at any cost, but optimized acceleration supported by engineering, documentation, and legal grounding. Investors who prioritize defensibility position themselves for consistent, sustainable tax advantages while minimizing exposure to audit risk.

Do you have a question about Cost Segregation?

Let us know how we can help

We hate SPAM. We will never sell your information, for any reason.