Cost Segregation for a 1031 Exchange Commercial Strip Mall

Jun 25, 2026Many investors complete a 1031 exchange into a commercial strip mall because they want to preserve equity and continue growing their portfolio without triggering immediate gain recognition. After closing, one of the most common questions is what a cost segregation report actually looks like and how it handles exchange property. The answer is more detailed than many investors expect. A quality report combines engineering analysis, asset classification, construction documentation, and tax law to allocate costs into the proper depreciation classes.

Many investors assume a cost segregation study prepared for a 1031 exchange looks exactly like a study performed on a standard acquisition. In reality, exchange properties often involve multiple basis layers that must be analyzed separately. A replacement strip mall may include carryover basis from the relinquished property, excess basis created by additional cash or financing, and post-acquisition improvements. A quality cost segregation report identifies these basis components, determines which assets qualify for accelerated depreciation, and documents how each portion is treated for tax purposes.

Schedule a CostSegRx Strategy Call.

Key Takeaways

- Understand what a cost segregation report contains and documents

- See how exchange property assets are classified correctly

- Learn why depreciation timing impacts investor cash flow

- Review common strip mall scenarios benefiting from studies

- Explore planning considerations after completing a 1031 exchange

- See how carryover basis and excess basis affect depreciation

- Understand what defines a defensible engineering-based study

What Does a Cost Segregation Report Look Like for a 1031 Exchange Strip Mall?

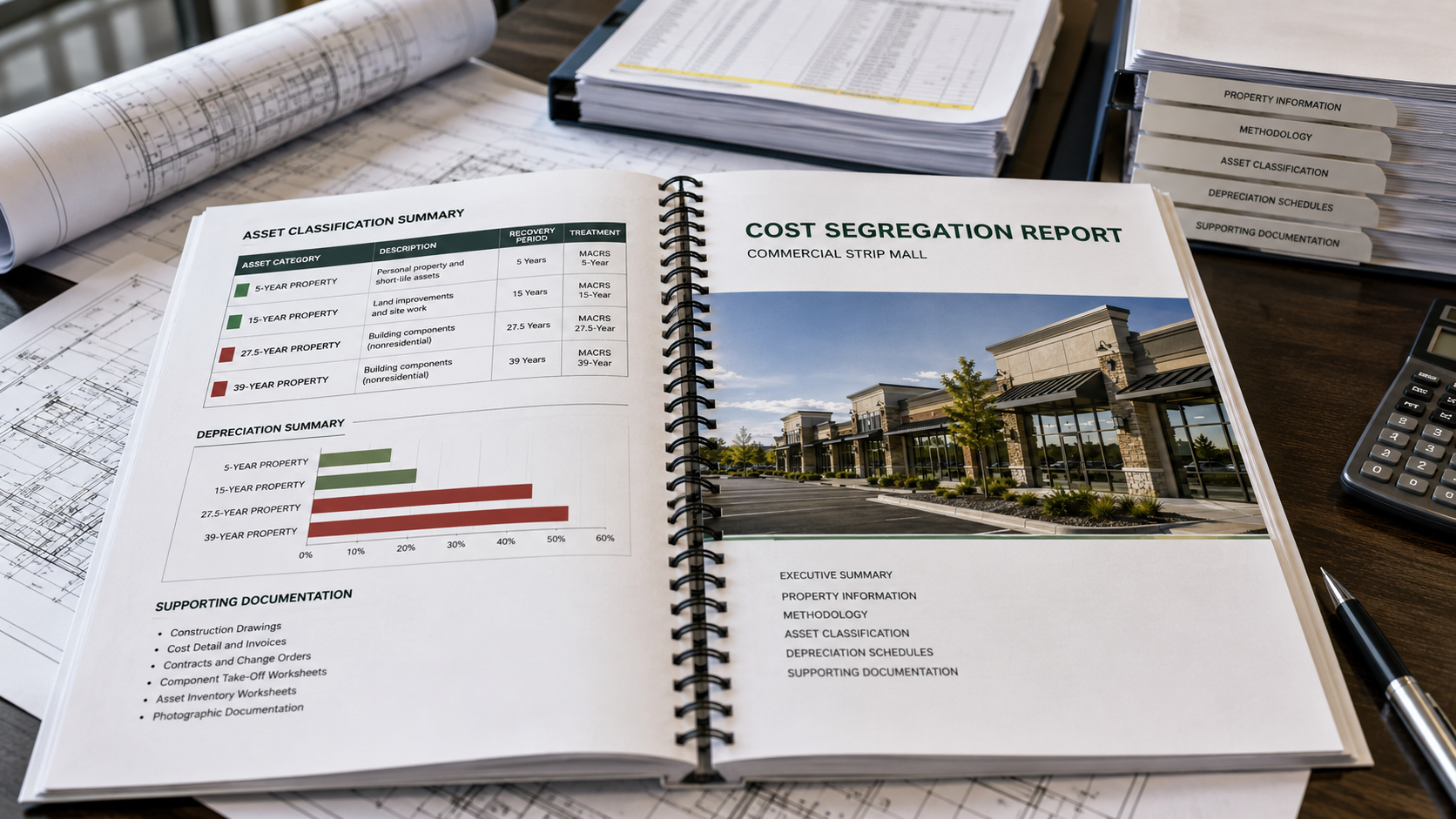

A professional cost segregation report is much more than a depreciation schedule. The IRS Cost Segregation Audit Technique Guide explains that quality studies should include engineering analysis, asset listings, supporting documentation, cost reconciliation, methodology explanations, and legal support for asset classifications.

For a commercial strip mall acquired through a 1031 exchange, the report typically includes an executive summary, property description, site inspection findings, construction and acquisition documentation, engineering asset analysis, detailed asset schedules, depreciation classifications, cost allocation schedules, supporting tax authority, and reconciliation to total project cost.

Many investors are surprised by the level of detail involved. A quality study generally resembles an engineering report combined with a tax analysis. Investors interested in understanding what makes a defensible study often benefit from reviewing a discussion of a quality cost segregation study.

How Assets Are Classified Inside the Report

The core purpose of the report is determining which assets qualify as §1245 property, which qualify as land improvements, and which remain part of the building structure. The IRS ATG discusses the distinction between §1245 property and §1250 property as one of the most important components of cost segregation analysis.

5-Year Property

For a typical commercial strip mall, 5-year property may include decorative specialty lighting, tenant-specific finishes, certain dedicated electrical systems, specialty millwork, specific equipment-support systems, and removable floor coverings. The analysis follows established engineering methodology and tax authority rather than estimates or percentages. Investors can learn more about proper classification of 5-year property and how engineering support affects defensibility.

15-Year Land Improvements

15-year land improvements often include parking lots, sidewalks, curbing, landscaping, site drainage, and exterior site improvements. These assets are frequently significant in strip mall properties because retail centers often have extensive site infrastructure. Additional discussion of 15-year land improvements can help investors understand their impact on depreciation acceleration.

QIP 15-Year Property

If qualifying interior improvements were completed after acquisition, portions may qualify as Qualified Improvement Property depending on the facts and timing of the renovation.

39-Year Nonresidential Real Property

Assets remaining in the building structure generally stay in the 39-year nonresidential real property category. Examples often include structural walls, roof systems, foundations, general building electrical systems, standard plumbing systems, and structural framing.

Why This Matters After a 1031 Exchange

Many investors assume a 1031 exchange alone creates tax savings. In reality, the exchange primarily defers gain recognition. The depreciation strategy occurs afterward.

Because replacement properties may contain carryover basis, excess basis, and future improvement basis, understanding how those components are analyzed within a cost segregation study is often just as important as completing the exchange itself.

A cost segregation study may allow portions of the exchange basis and additional capital investment to be allocated into faster recovery categories. This can significantly increase depreciation deductions during the early ownership years.

For investors focused on maximizing after-tax cash flow, understanding cost segregation benefits is often an important next step after completing an exchange transaction.

Common Strip Mall Applications

Commercial strip malls frequently contain asset categories that make cost segregation particularly valuable. Examples include neighborhood retail centers, grocery-anchored centers, mixed retail developments, multi-tenant shopping centers, renovated retail properties, and value-add retail acquisitions.

These properties often contain significant parking areas, landscaping, tenant improvements, and specialized retail finishes that create opportunities for proper asset reclassification.

Strategy Considerations for 1031 Exchange Investors

Timing matters.

Many investors complete the exchange transaction and then wait several years before evaluating cost segregation. While studies can often be performed later through accounting method change procedures, planning earlier may improve cash flow visibility and tax forecasting.

Property records, closing statements, improvement histories, site inspections, and engineering analysis all contribute to a stronger report. Investors should avoid studies that rely on unsupported percentages or broad assumptions. The IRS ATG specifically discusses detailed engineering approaches and quality study standards as preferred methodologies.

Investors evaluating study timing may benefit from understanding when to perform a cost segregation study.

Financial Example: Cost Segregation After a 1031 Exchange

Consider an investor who sells a relinquished strip mall and completes a properly structured 1031 exchange into a replacement strip mall purchased for $8,000,000.

Unlike a standard acquisition, the replacement property's depreciable basis may include multiple components that require separate analysis within the cost segregation study.

In this example, the replacement property's basis includes carryover basis from the relinquished property as well as excess basis created by the investor's additional capital and financing. A quality engineering-based study evaluates the replacement property and determines which assets qualify as 5-year property, 15-year land improvements, and 39-year nonresidential real property.

Assume the engineering analysis identifies the following allocation of the $6,400,000 depreciable basis:

| Classification | Allocation % | Amount |

|---|---|---|

| 5-Year Property | 22% | $1,408,000 |

| 15-Year Land Improvements | 8% | $512,000 |

| 39-Year Nonresidential Real Property | 70% | $4,480,000 |

In this example, 30% of the depreciable basis is allocated to accelerated depreciation categories.

Actual percentages vary based on property design, tenant improvements, site improvements, construction details, available records, and engineering findings. Most strip mall studies generally fall within a range of approximately 17% to 28% reclassification, although higher percentages may be supportable when property characteristics and documentation justify the classification.

One important difference between a standard acquisition study and a 1031 exchange study is that the report may contain separate schedules showing how depreciation is calculated for carryover basis, excess basis, and later improvements. This additional level of analysis is one reason detailed engineering documentation is especially important for exchange properties.

What Investors Should Expect From a Defensible Report

A quality cost segregation report for a 1031 exchange strip mall should clearly explain how each asset was identified, measured, and classified. The strongest reports use detailed engineering methodology, reconcile allocated costs to total project costs, document supporting evidence, and align classifications with established tax authority and IRS guidance. The goal is not simply to accelerate depreciation. The goal is to accurately classify assets based on their actual function and characteristics.

Unlike a traditional acquisition study, a 1031 exchange cost segregation report may include separate schedules for carryover basis, excess basis, and subsequent improvements. This additional complexity makes accurate engineering analysis, asset classification, and documentation especially important. When properly prepared, a cost segregation study provides investors with a structured, supportable framework for maximizing depreciation while maintaining compliance with established tax treatment.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.