1031 Exchange Explained. How Real Estate Investors Defer Taxes and Build Wealth

Mar 27, 2026A 1031 exchange allows real estate investors to defer capital gains taxes when selling and reinvesting into like-kind property. Under IRC §1031, the gain is not eliminated. It is deferred and carried into the replacement property. When combined with cost segregation and depreciation strategies, a 1031 exchange becomes a powerful tool for long-term tax planning and portfolio growth.

- What Is a 1031 Exchange

- How a 1031 Exchange Works

- Key IRS Rules and Deadlines

- Tax Benefits and Strategy

- Combining 1031 Exchange with Cost Segregation

What Is a 1031 Exchange

A 1031 exchange is a tax-deferral strategy that allows investors to sell investment or business real estate and reinvest the proceeds into another qualifying property without immediately recognizing capital gains tax. The term “like-kind” is broad and generally includes most real property held for investment or business use.

The deferred gain reduces current tax liability and allows more capital to remain invested. Over time, this can significantly increase purchasing power and portfolio scale.

How a 1031 Exchange Works

The process involves selling a relinquished property and acquiring a replacement property through a qualified intermediary. The investor never takes direct receipt of the proceeds. Instead, funds are held and transferred to complete the exchange.

The replacement property must be of equal or greater value to fully defer taxes. Any cash or debt reduction received is considered “boot” and may be taxable.

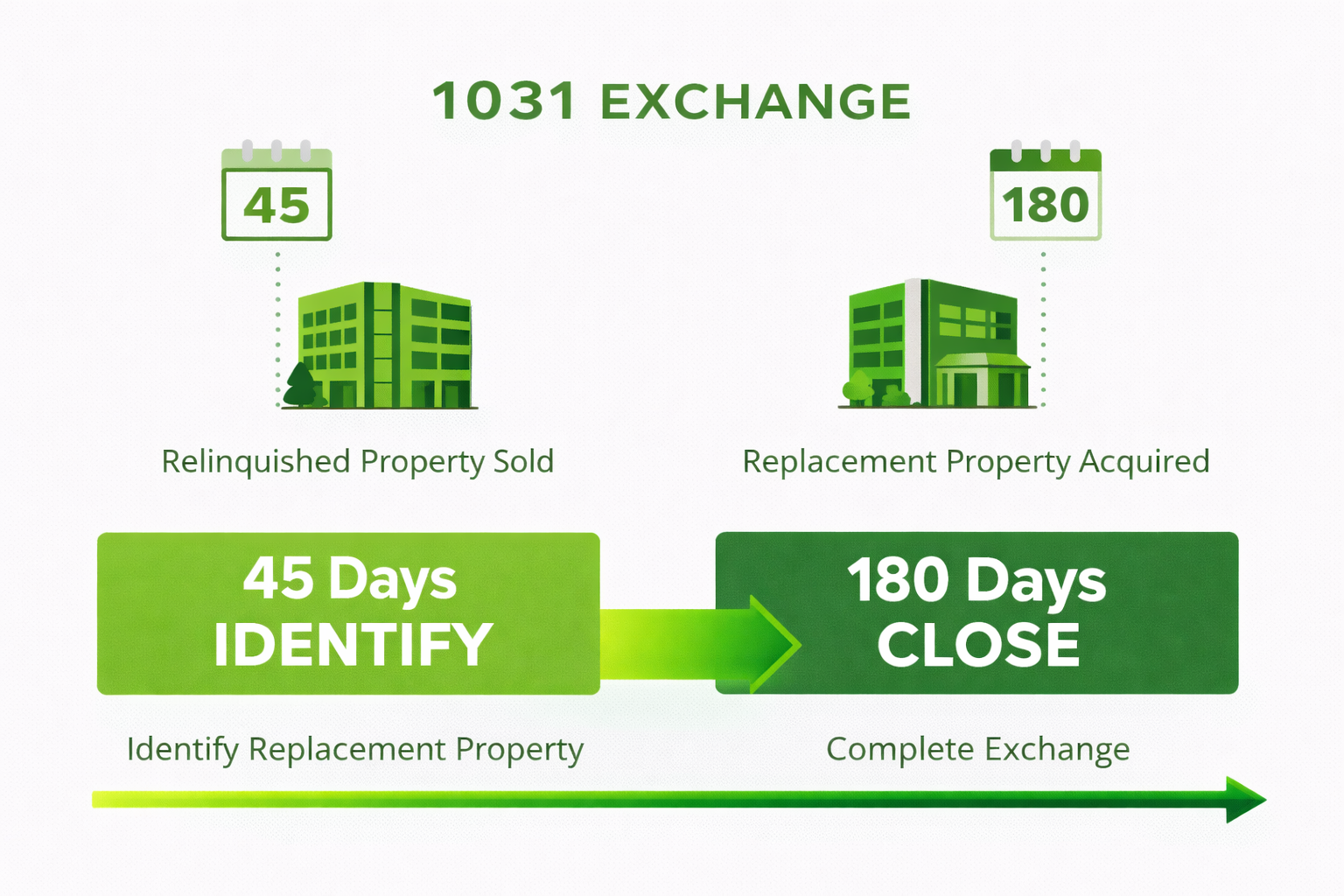

Key IRS Rules and Deadlines

1031 exchanges are governed by strict timing and structural requirements. Missing deadlines can disqualify the exchange and trigger full tax recognition.

Key rules include:

- 45-day identification period to select replacement property

- 180-day completion window to close on the new asset

- Use of a qualified intermediary is required

- Property must be held for investment or business use

Tax Benefits and Strategy

The primary benefit of a 1031 exchange is tax deferral. Investors defer capital gains tax, depreciation recapture, and in some cases state taxes. This allows more equity to be reinvested into larger or higher-performing assets.

Over multiple exchanges, investors can continue to defer gains indefinitely. When paired with estate planning, deferred gains may be eliminated through a step-up in basis.

Strategically, investors use 1031 exchanges to consolidate properties, diversify into new markets, or transition into assets with stronger cash flow.

Combining 1031 Exchange with Cost Segregation

A 1031 exchange defers taxes. Cost segregation accelerates deductions. Together, they create a powerful tax strategy.

After acquiring a replacement property, investors often perform a cost segregation study to reclassify assets into shorter recovery periods such as 5-year property and 15-year property. This increases early-year depreciation and improves cash flow.

Bonus depreciation may further enhance these benefits. Many investors evaluate bonus depreciation strategy immediately after completing an exchange to maximize first-year deductions.

Timing also matters. Understanding when to perform a cost segregation study ensures the deductions align with tax planning goals.

When executed correctly, this combined strategy allows investors to defer gains on the sale while generating new deductions on the acquisition. This creates both short-term tax savings and long-term wealth accumulation.

1031 exchanges remain one of the most effective tools in commercial real estate tax planning. When paired with depreciation strategies, they provide a structured path to scale portfolios, increase cash flow, and manage tax liability over time.

Do you have a question about Cost Segregation?

Let us know how we can help

Your information is secure. We only use your details to answer your direct inquiry.